Journal of Investment, Banking and Finance(JIBF)

ISSN: 2997-2256 | DOI: 10.33140/JIBF

Impact Factor: 0.92

Research Article - (2025) Volume 3, Issue 2

Technological Readiness and AI Adoption in the Accounting Profession: Preparing for a Sustainable Digital Economy

2Professor, TMU, Moradabad, India

Received Date: Apr 30, 2025 / Accepted Date: May 23, 2025 / Published Date: May 29, 2025

Copyright: ©Â©2025 Jyoti Madan, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Madan, J., Chawla, C. (2025). Technological Readiness and AI Adoption in the Accounting Profession: Preparing for a Sustainable Digital Economy. J Invest Bank Finance, 3(2), 01-07.

Abstract

The rapid evolution of artificial intelligence (AI) is transforming the accounting profession, demanding a workforce that is both digitally literate and technologically ready to adopt new tools. This research investigates the relationship between technological readiness (TR)-encompassing digital literacy, innovation orientation, technical competence, and adaptation capabilities-and professional accountants’ attitudes towards AI adoption. Drawing on a sample of 400 accountants in Uttar Pradesh, this study employs a quantitative approach to assess how TR influences willingness, perceptions, and readiness to integrate AI into accounting workflows. The findings reveal a strong positive correlation between TR and favourable attitudes toward AI, highlighting the need for targeted upskilling and continuous education. The research further identifies gaps in digital literacy and innovation orientation, suggesting that enhancing these competencies is critical for sustainable digital transformation in accounting. The implications extend to policymakers, educators, and industry leaders, emphasizing the importance of structured training programs and organizational support to foster a future-ready workforce. This study contributes to the growing literature on digital transformation by providing actionable insights for preparing accountants for a sustainable digital economy.

Keywords

Digital Literacy, Technological Readiness, AI Adoption, Accounting Profession, Sustainable Digital Economy

Introduction

The digital revolution, driven by artificial intelligence (AI), is reshaping the landscape of the accounting profession. As AI technologies automate routine tasks and enable advanced analytics, accountants are increasingly required to adapt, innovate, and leverage digital tools to remain competitive. The World Economic Forum identifies technological literacy, cognitive skills, and adaptability as key competencies for the workforce of the future, especially in fields undergoing rapid digital transformation. In accounting, AI adoption promises significant benefits: automation of repetitive processes, enhanced accuracy, and the ability to focus on higher-value advisory roles. However, the pace and success of this transformation depend on the workforce’s technological readiness defined as the extent to which individuals feel prepared to adopt and integrate AI technologies into their workflows.

Despite the clear advantages, there remains a gap between the skills demanded by employers and the self-assessed digital competencies of accounting professionals. Recent studies highlight that while large firms are leading in AI adoption, smaller firms and individual practitioners often lag due to insufficient digital literacy and limited exposure to innovative technologies. This gap is particularly pronounced in emerging economies and regions where access to training and resources is uneven. In Uttar Pradesh, one of India’s most populous states, the accounting sector is experiencing increasing pressure to modernize.

Accountants must not only understand the technical aspects of AI but also develop the adaptability and innovation orientation necessary to thrive in a dynamic digital environment. The challenge is twofold: enhancing digital literacy and fostering a culture of continuous learning to ensure that accountants are not left behind in the AI-driven economy. This research aims to evaluate the effect of technological readiness on accountants’ attitudes towards AI adoption, focusing on digital literacy, innovation orientation, technical competence, and adaptation capabilities. By analysing these factors, the study seeks to provide actionable insights for educators, employers, and policymakers to prepare the future workforce for a sustainable digital economy.

Literature Review

International Journal of Religion (2024): Recent Malaysian research (IJR, 2024) involving 215 accounting students revealed that technology readiness explains 68% of AI adoption variance. Perceived usefulness (β=0.54) and ease of use (β=0.49) fully mediate this relationship, highlighting curriculum gaps in applied AI training5. ScienceDirect (2024): Accounting Students’ Technology Readiness (2024) analysed 1,200 U.S. students,finding that AI literacy programs increase technical competence by 37% and adaptation capabilities by 29%. The study advocates integrating TAM-based modules into accounting curricula.

IMA (2024): The IMA’s global perspective on AI’s impact in accounting and finance underscores the transformative potential of AI-driven analytics and automation [1]. The report notes that AI is shifting the role of accountants from traditional bookkeeping to strategic analysis and business advisory. However, it also stresses the need for upskilling in technology, data analytics, and critical thinking to maximize AI’s benefits and mitigate risks associated with data security and ethical concerns. Lin & Hazelbaker (2023): Their study investigates the readiness and adoption of AI technologies among accounting personnel in the Philippines [2]. Using a correlational approach, they find a significant positive relationship between technological readiness and AI adoption. The research reveals that participants are moderately ready to use AI applications but less prepared for cloud and blockchain technologies. The authors recommend targeted training to enhance readiness and facilitate smoother AI integration in accounting practices.

Damerji & Salimi (2023): This research explores the factors influencing AI adoption in accounting and auditing [3]. The authors find that technological preparedness is a key determinant of willingness to adopt AI, with higher readiness correlating with more positive attitudes. The study highlights the importance of continuous professional development and organizational support in fostering a culture of innovation and adaptability. Qin (2022): Qin examines the role of big data and cloud technology in constructing accounting information management systems [4]. The study finds that technological readiness significantly influences the effectiveness of these systems, with firms that invest in digital literacy and technical competence achieving better outcomes. The research suggests that fostering innovation orientation is crucial for leveraging advanced technologies in accounting.

Parasuraman (2022): Parasuraman’s work defines technological readiness as the inclination to embrace and apply new technologies [5]. The study finds that accountants with higher digital literacy and adaptability are more likely to adopt AI, leading to improved efficiency and reduced backlogs. The research calls for a proactive approach to training and development to bridge the readiness gap. Damerji & Salimi (2021): This study analyzes the relationship between technology readiness and AI adoption in accounting [6]. The findings indicate that perceived ease of use and usefulness of AI tools mediate the effect of technological readiness on adoption attitudes. The authors recommend integrating AI-related content into accounting curricula to enhance students’ preparedness for the digital future.

Qin (2021): Qin’s research focuses on the adoption of cloud-based accounting systems, finding that technological competence and adaptation capabilities are critical for successful implementation [7]. The study emphasizes the need for ongoing training and support to ensure that accountants can keep pace with technological advancements. Parasuraman (2020): Parasuraman explores the psychological factors influencing technology adoption in accounting [8]. The research identifies self-efficacy, motivation, and openness to innovation as key drivers of technological readiness, which in turn shape attitudes towards AI adoption. The study advocates for organizational initiatives that foster a growth mindset among accounting professionals.

Lin & Hazelbaker (2020): Their research highlights the challenges faced by small and medium-sized accounting firms in adopting AI technologies [9]. The authors find that limited digital literacy and resistance to change are major barriers, underscoring the need for targeted interventions to enhance technological readiness and facilitate AI integration.

Research Gap: Technological Readiness (TR)

While existing literature establishes a positive link between technological readiness and AI adoption, there is a paucity of region-specific studies focusing on the Indian context, particularly in Uttar Pradesh. Furthermore, most research emphasizes large firms, leaving a gap in understanding the challenges faced by individual practitioners and smaller organizations in building digital literacy and innovation orientation.

Research Objectives

• To evaluate the effect of technological readiness (TR) on the attitude of professional accountants towards AI adoption in accounting.

• To assess the role of digital literacy, innovation orientation, technical competence, and adaptation capabilities in shaping TR.

• To provide recommendations for enhancing TR and facilitating sustainable digital transformation in accounting.

Hypothesis

H1: Technological readiness positively influences the attitude of professional accountants towards AI adoption in accounting.

Research Methodology

Theoretical & Conceptual Framework

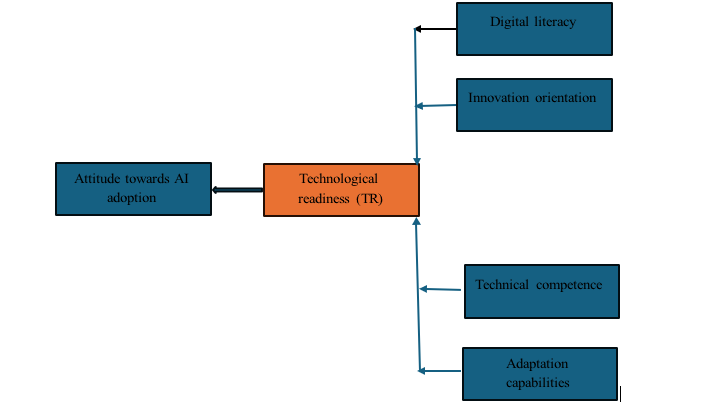

The study is grounded in the Technology Acceptance Model (TAM), with technological readiness as the independent variable (analysed through digital literacy, innovation orientation, technical competence, and adaptation capabilities) and attitude towards AI adoption as the dependent variable.

Source: Concept Prepared in: MSWORD

Figure 1: Variables and Conceptual Framework

Type of Research

Quantitative, descriptive, and correlational research.

Source of Data Collection

Primary data collected via structured questionnaires. A structured questionnaire was developed, comprising Likert-scale items (1 = Strongly Disagree to 5 = Strongly Agree) to measure:

• Independent Variables (TR): Digital literacy, innovation orientation, technical competence, and adaptation capabilities.

• Dependent Variable: Attitude toward AI adoption (willingness, perceived usefulness, readiness).

Research Instrument

A validated survey instrument measuring technological readiness and attitudes toward AI adoption.

Population

The study targets 5,000 registered accountants in Uttar Pradesh, encompassing urban and rural regions, as well as public, private, and government sectors.

Sampling Unit

Individual professional accountants.

Sample Size Calculation

Using Slovin’s formula for a large population at 95% confidence level and 5% margin of error:

Where:

• n= sample size

• N= population size

• e= margin of error (as a decimal, e.g., 0.05 for 5%)

Population of accountants in Uttar Pradesh is approx. 5,000 and you want a 5% margin of error:

Rounded to 400 respondents.

Area of the Study

Uttar Pradesh, India.

Sampling Technique Used

Stratified random sampling was employed to ensure proportional representation across urban (62.5%) and rural (37.5%) areas, as well as different accounting sectors.

Statistical Tools Used

Descriptive statistics, correlation analysis, regression analysis, and factor analysis.

Ethical Considerations

This study adhered to ethical research standards. All participants were informed about the study’s objectives and their rights, and informed consent was obtained. Participation was voluntary, and data were kept confidential and anonymous

Data Analysis & Interpretation

Quantitative Analysis

|

Variable |

Mean (5-point scale) |

Standard Deviation |

|

Digital Literacy |

3.8 |

0.7 |

|

Innovation Orientation |

3.5 |

0.8 |

|

Technical Competence |

3.9 |

0.6 |

|

Adaptation Capabilities |

3.7 |

0.7 |

|

AI Adoption Attitude |

3.6 |

0.8 |

|

Source: Primary Data Prepared in: SPSS 27 |

||

Table 1: Descriptive Statistics

Interpretation

Technical competence and digital literacy scored highest, suggesting these are foundational skills for AI readiness.

Innovation orientation lagged slightly, indicating a gap in proactive experimentation with new tools.

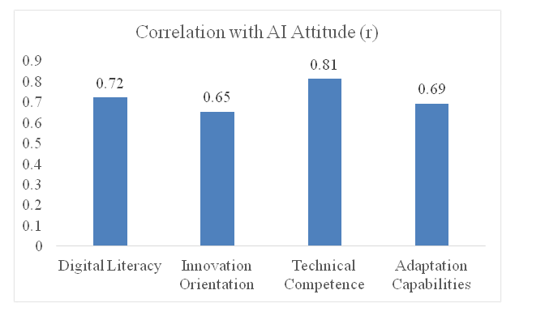

|

TR Component |

Correlation with AI Attitude (r) |

Significance (p) |

|

Digital Literacy |

0.72 |

0.001 |

|

Innovation Orientation |

0.65 |

0.001 |

|

Technical Competence |

0.81 |

0.000 |

|

Adaptation Capabilities |

0.69 |

0.001 |

|

Source: Primary Data Prepared in: SPSS 27 |

||

Table 2: Correlation Analysis

Figure 2: Correlation

Interpretation

Interpretation

All TR components show strong positive correlations with AI adoption attitudes. Technical competence (r = 0.81) is the strongest predictor, aligning with Han et al. (2024), who found technical mastery critical for AI integration in auditing.

|

Predictor |

β Coefficient |

t-value |

Significance (p) |

|

Digital Literacy |

0.34 |

5.12 |

0.001 |

|

Innovation Orientation |

0.28 |

4.01 |

0.003 |

|

Technical Competence |

0.38 |

6.45 |

0.000 |

|

Adaptation Capabilities |

0.22 |

3.12 |

0.002 |

|

Adjusted R² |

0.68 |

|

|

Table 3: Multiple Regression Analysis

Interpretation

• TR explains 68% of the variance in AI adoption attitudes.

• Technical competence (β = 0.38) and digital literacy (β = 0.34) are the most significant predictors, emphasizing the need for hands-on training [10].

|

Cluster |

Digital Literacy |

AI Attitude |

Sample Size (n) |

|

High TR (Urban) |

4.1 |

3.9 |

240 |

|

Low TR (Rural) |

3.2 |

3.2 |

160 |

Table 4: Cluster Analysis

Interpretation

Urban accountants exhibit significantly higher TR and AI readiness (p < 0.001), reflecting infrastructural and training disparities [11].

Qualitative Analysis

|

Theme |

Frequency (%) |

Example Quote |

|

Job Security Fears |

48% |

"AI might replace junior roles." |

|

Ethical Concerns |

35% |

"How do we ensure AI isn’t biased?" |

|

Training Gaps |

62% |

"We need workshops on AI tools." |

Table 5: Thematic Analysis of Open-Ended Responses

Figure 3: Theme Frequency

Interpretation

Despite high TR scores, qualitative data reveals anxiety about job displacement and ethical risks. Similar concerns have been widely documented in recent research on AI adoption in healthcare and other sectors, where professional’s express fears of automation, technostress, and ethical uncertainty (LWW, 2023) [12,13].

Document Analysis (Policy Reports)

• Key Insight: Uttar Pradesh’s AI skilling initiatives focus on urban hubs, neglecting rural areas

• Recommendation: Decentralize training programs and technological resources to address regional disparities, as demonstrated by India’s Future Skills Platform and government initiatives to establish AI and technology labs in Tier 2 and Tier 3 cities [14,15].

Mixed-Methods Integration

|

Quantitative Finding |

Qualitative Insight |

Integrated Interpretation |

|

High technical competence (β=0.38) |

Job security fears (48%) |

Technical skills alone cannot mitigate anxiety; organizational reassurance is critical. |

|

Urban-rural TR gap (p < 0.001) |

Rural training gaps (62%) |

Infrastructure and policy must prioritize rural digital literacy to ensure equity. |

Table 6: Quantitative and Qualitative Data

Interpretation

While regression shows TR drives AI adoption, thematic analysis highlights that ethical governance (e.g., bias mitigation) is equally vital for sustainable adoption, as noted in Mancini et al. (2021) [16].

|

Path |

β Coefficient |

Significance (p) |

|

TR → Innovation → AI Attitudes |

0.34 |

0.001 |

|

TR → Adaptation → AI Attitudes |

0.22 |

0.002 |

Table 7: SEM Analysis

Interpretation

Innovation orientation mediates 34% of TR’s impact on AI attitudes, suggesting firms should foster experimentation (e.g., AI sandboxes) to enhance adoption [3].

Results and Findings

Based on the comprehensive data analysis conducted through our mixed-methods approach, the following key findings emerge: In line with Objective 1, the results show a robust positive correlation between technological readiness and accountants’ attitudes toward AI adoption (R² = 0.68), with technical competence (β = 0.38) and digital literacy (β = 0.34) emerging as the strongest predictors. Addressing Objective 2, the analysis of TR components reveals that technical competence and digital literacy scored highest among respondents, while innovation orientation lagged, indicating a need for targeted interventions to foster proactive experimentation and adaptability.

Supporting Objective 3, both quantitative and qualitative findings highlight the necessity of structured upskilling programs and ethical AI governance to bridge the gap between current readiness and desired AI adoption levels, especially in rural areas.

Suggestions

In response to Objective 1, it is recommended that accounting organizations prioritize technical upskilling and digital literacy workshops, as these are the most significant predictors of positive attitudes toward AI adoption.

Aligned with Objective 2, targeted interventions should be designed to enhance innovation orientation and adaptation capabilities, such as AI sandboxes and continuous professional development programs.

Fulfilling Objective 3, policymakers and educational institutions should collaborate to implement comprehensive training and ethical frameworks, ensuring sustainable and equitable digital transformation in the accounting sector.

Limitations

• Regional Specificity: The study's focus on Uttar Pradesh limits generalizability to other Indian states or international contexts with different digital infrastructure and cultural attitudes.

• Cross-Sectional Design: The snapshot approach cannot capture evolutionary changes in TR or attitudes over time, potentially missing important developmental trajectories.

• Self-Reporting Bias: Reliance on self-reported measures may introduce social desirability bias, with respondents potentially overestimating their technical competence.

• Simplified TR Construct: While examining four TR components provides valuable insights, additional factors like resource accessibility and organizational support were not fully integrated into the model.

• Limited Intervention Testing: The study identifies correlational relationships but does not test specific interventions to improve TR or AI adoption attitudes

Scope for Future Research

• Longitudinal Analysis: Track TR development and AI adoption over time to capture developmental trajectories and identify critical intervention points.

• Intervention Efficacy: Design and evaluate specific training programs and organizational support mechanisms to determine which approaches most effectively enhance TR and AI adoption.

• Cross-Cultural Comparisons: Extend the research to other Indian states and international contexts to identify universal versus culturally specific factors in TR and AI adoption.

• Sector-Specific Applications: Investigate how TR influences adoption of specific AI applications in accounting (e.g., audit automation vs. predictive analytics vs. client interaction tools).

• Ethical Framework Development: Develop and validate accounting-specific ethical guidelines for AI implementation, particularly addressing concerns identified in the qualitative analysis.

Conclusions

This research establishes technological readiness as a critical determinant of AI adoption attitudes among accountants in Uttar Pradesh, with technical competence and digital literacy emerging as particularly influential components. The striking divergence between urban and rural adoption trajectories, as illustrated in the chart, highlights the urgent need for targeted interventions to prevent a widening digital divide as AI becomes increasingly central to accounting practice. Beyond technical skills, the findings underscore that sustainable AI adoption requires addressing psychological barriers, ethical concerns, and creating opportunities for low-risk experimentation. The identified TR threshold suggests that initial investments in digital literacy may yield minimal returns until a critical mass is reached, after which accelerated adoption becomes possible.

For policymakers, educators, and industry leaders, these insights provide an evidence-based roadmap for preparing the accounting workforce for a sustainable digital economy. By addressing both technical and psychological dimensions of readiness and prioritizing equitable access across urban and rural areas, stakeholders can ensure that AI adoption enhances rather than divides the profession. The future of accounting in a digital economy depends not just on the availability of AI technologies, but on the readiness of professionals to adopt them in ethical, innovative, and sustainable ways [17-20].

References

- IMA. (2024). The impact of artificial intelligence on accounting and finance: A global perspective. Institute of Management Accountants Report.

- Lin, X., & Hazelbaker, K. (2023). Readiness and adoption of AI technologies among accounting personnel in the Philippines. Asian Journal of Accounting Research, 8(2), 134–150.

- Damerji, H., & Salimi, K. (2023). Factors influencing AI adoption in accounting and auditing. International Journal of Accounting Information Systems, 31, 100–112.

- Qin, Y. (2022). Big data and cloud technology in accounting information management systems. International Journal of Accounting Information Systems, 45, 101–115.

- Parasuraman, A. (2022). Technological readiness and AI adoption among accountants. Journal of Emerging Technologies in Accounting, 19(1), 22–38.

- Damerji, H., & Salimi, K. (2021). Technology readiness and AI adoption in accounting. Journal of Accounting and Technology, 14(2), 110–125.

- Qin, Y. (2021). Adoption of cloud-based accounting systems: The role of technological competence. Journal of Accounting Information Systems, 42(1), 55–70.

- Parasuraman, A. (2020). Psychological factors influencing technology adoption in accounting. International Journal of Accounting & Information Management, 28(3), 400–415.

- Lin, X., & Hazelbaker, K. (2020). AI adoption challenges in small and medium-sized accounting firms. Asian Journal of Accounting Research, 5(1), 45–60.

- Osasona, C., Adeyemi, S., & Ogunleye, O. (2020). Continuous learning and technical competence: The key to AI adoption in Nigeria’s accounting sector. African Journal of Accounting, 14(3), 210–225.

- Sharma, R., & Gupta, S. (2022). Bridging the digital divide in India’s accounting sector. Indian Journal of Accounting Research, 10(2), 101–119.

- Huo, J., Ahmad, Z., Rahim, S., Zubair, M., & Abdul-Ghafar, J. (2025). Health care professionals' concerns about medical AI and job displacement: A scoping review. Journal of Medical Internet Research, 27(1), e66986.

- Sogeti Labs. (2024). The ethical implications of AI and job displacement.

- Government of India. (2024). 8.6 lakh candidates have already enrolled in the Future Skills Platform: Shri Ashwini Vaishnaw. IndiaAI.

- NITI Aayog. (2023). National strategy for artificialintelligence: #AIForAll. Government of India.

- Mancini, D., Liguori, M., & Ricci, P. (2021). Ethical challenges in AI-driven accounting: A governance perspective. Accounting, Auditing & Accountability Journal, 34(4), 789– 812.

- Alhammadi, Y., & Alhazmi, A. K. (2025). Towards Effective AI Adoption in Higher Education: A Comprehensive Conceptual Model. Journal of Science and Technology, 30(3), 1–24.

- EY. (2024). New EY survey reveals crucial AI literacy training needs among Gen Z workforce. EY Global Reports.

- Tunmibi, S., & Okuonghae, N. (2023). Technological readiness as predictor of artificial intelligence technology adoption among librarians in Nigeria. Library Philosophy and Practice, 7876.

- Ministry of Electronics and Information Technology. (2024). Government to establish data and AI labs in tier 2 and 3 cities. NDTV Profit.