Journal of ENT Surgery Research(JESR)

Research Article - (2026) Volume 4, Issue 1

Evaluating Risk Management Practices and Banking System Stability: A Comparative Study of Spain Pre and Post-COVID-19 (2017–2023)

Received Date: Mar 27, 2026 / Accepted Date: Apr 17, 2026 / Published Date: Apr 29, 2026

Copyright: ©2026 Pakhlavon Orifjonov. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Orifjonov, P. (2026). Evaluating Risk Management Practices and Banking System Stability: A Comparative Study of Spain Pre and Post-COVID-19 (2017

Abstract

This paper examines the role of banks in managing risk through diversification and information-based mechanisms, as well as the effectiveness of regulatory capital buffers in strengthening financial stability. It then evaluates the resilience of the Spanish banking sector across two periods: before the COVID-19 crisis (2017–2019) and after the initial recovery phase (2021–2023). Focusing on capital adequacy, liquidity positions, and profitability, the study relies on official publications of the Banco de España and the IMF to identify trends and structural changes in Spain’s banking environment. The findings indicate that regulatory reforms, strong capital positions, and liquidity support measures contributed significantly to the sector’s post-pandemic resilience.

Introduction

Banks play a fundamental role in the financial system by acting as intermediaries between savers and borrowers. Through deposit collection, lending activities, and financial services, banks support economic growth, facilitate investment, and ensure the efficient allocation of financial resources. However, the banking sector is exposed to various risks, including credit risk, liquidity risk, market risk, and operational risk. Effective risk management is therefore essential for ensuring the stability and sustainability of financial institutions. One of the key challenges in banking arises from asymmetric information, where borrowers possess more information about their financial situation than lenders. This imbalance of information can lead to problems such as adverse selection and moral hazard, which increase the probability of loan defaults and financial instability. To address these issues, banks implement several mechanisms such as credit scoring systems, collateral requirements, borrower monitoring, and third-party guarantees in order to reduce uncertainty and improve lending decisions. In addition to internal risk management strategies, regulatory authorities play an important role in ensuring the stability of the banking system. After the global financial crisis of 2007–2009, the Basel III regulatory framework introduced additional capital requirements and macroprudential tools aimed at strengthening banks’ resilience during periods of financial stress. Among these tools are the capital conservation buffer (CCoB) and the countercyclical capital buffer (CCyB), which require banks to hold additional capital during economic expansions so that they can absorb losses during economic downturns. This paper combines theoretical discussion and empirical analysis. First, it critically evaluates the role of banks in risk diversification and their approaches to addressing asymmetric information. Second, it assesses the role of Basel III capital buffers in mitigating systemic risk. Finally, the paper analyzes the resilience of the Spanish banking system before and after the COVID-19 crisis by comparing capital adequacy, liquidity positions, and profitability indicators using data from official financial stability reports.

The Role of Banks in Risk Diversification and Asymmetric Information

Banks are relevant to economic development through the financial services they provide. Their intermediation role can be said to be incentive for economic growth. Banks are essential for risk diversification as they manage and allocate risk across diverse assets, clients, and financial instruments, which reduces the effects of failures in certain sectors. Their strategies for diversification can reduce various types of risks, including credit, market, operational and liquidity risks. “In addition to other risks that banks face, credit risk is a major factor affecting their profitability, as a substantial portion of their revenue is derived from interest on loans. But interest rate risk is directly associated with credit risk, which means that a high or growing interest rate increases the likelihood of a loan default [1].” Credit risk is a risk of loss resulting from an obligor’s inability to meet its obligations. Increasing non-performing loans in the credit portfolio reduces banks’ ability to achieve their objectives. Non-performing loans are defined as loan values that have not been serviced for three months or more [2]. Continuing, one of the main risks in banking has become liquidity risk, since it caused failure of many banks in the recent past. Liquidity risk not only affects the performance of a bank but also its reputation. Comptroller of the Currency (2001) noted that liquidity risk has become a serious concern and challenge for the modern era banks [3].

A bank having good asset quality, strong earnings and sufficient capital may fail if it is not maintaining adequate liquidity These are the main reasons why banks diversify their assets. Banks face challenges in asymmetric information, leading to adverse selection and moral hazard. Strategies mitigate this, improving risk management and financial stability. Credit scoring systems are one of the main ways banks figure out if a borrower is creditworthy. These systems look at users’ past and present financial situations to get a better idea of how likely they are to be able to pay back loans. According to Nikitenko (2013), using advanced credit scoring models and making financial disclosures required are very important for reducing information gaps. This lets banks make better lending choices. Banks also reduce risk by requiring collateral. Lenders secure borrowers’ repayment motivation by securing loans with actual assets. Collateral protects lenders and encourages borrowers to repay loans, according to a study [4]. This method reduces adverse selection and aligns parties’ interests. Third-party guarantees secure loans by holding the guarantor responsible for the debt, including interest, if the borrower defaults. When initial borrowers cannot repay the loan and interest, guarantors should cover the amount. This makes loans more appealing to lenders [5]. Finally, borrowers must be monitored financially to reduce moral hazard. Assessing borrowers’ finances regularly helps banks identify dangers. According to the Federal Deposit Insurance Corporation, constant monitoring allows banks to respond promptly to changing borrower situations, maintaining loan portfolio stability and eliminating unforeseen risks.

The capital conservation buffer (CCoB) and the countercyclical capital buffer (CCyB) are important parts of the Basel III regulatory scheme. They are meant to make banks more stable and lower systemic risk. Both buffers help keep the economy stable in different ways, especially when the economy is under a lot of stress. Banks are required to keep more capital on hand than the minimum capital standards, which are set at 2.5% of risk-weighted assets. This is called the CCoB. With this cushion, the government wants to make sure that banks can handle losses when the economy is down. The Bank for International Settlements says that the CCoB is very important for making sure that individual financial institutions are safe, which helps keep the whole financial system stable. When a bank’s capital goes below this buffer, it can’t give out capital in the form of dividends or bonuses. This forces banks to rebuild their capital reserves. The purpose of this system is to protect against possible losses and keep banks running even when things get tough. The CCoB is especially important during economic downturns, when banks are quicker to incur losses. By mandating banks to maintain more capital during successful times, the CCoB generates a buffer that can be used during times of crisis. This proactive approach not only protects individual banks, but also strengthens the overall resilience of the financial sector to systemic shocks.

The Countercyclical Capital Buffer (CCyB) is a significant regulatory system that aims to reduce systemic risks linked with rapid loan growth and financial imbalance. It enables macroprudential authorities to change banks’ capital requirements based on current economic conditions, influencing lending behaviour and promoting financial stability. During borrowing raises, authorities might raise the CCyB requirement, forcing banks to keep additional capital. This proactive policy tries to reduce lending practices that cause asset bubbles and financial crises. During economic downturns, banks might limit or release the CCyB to maintain lending and economic activity. Flexibility is needed to avoid credit supply limits that worsen recessions. According to Faria-e-Castro (2019), introducing the CCyB could have helped to protect the US economy from the effects of the 2007-09 financial crisis by ensuring banks maintained adequate capital buffers during periods of fast credit expansion. According to the analysis, increased capital requirements under favourable economic situations can prevent future financial crises or at least mitigate their impact during recessions. Katerina Lagaria’s work on capital buffers (2021) suggests that the CCoB and the CCyB are both capital buffers designed to absorb losses in times of stress, introduced by the Basel III Capital Accord. They focus on the downturn phase, when they are released to strengthen the banking sector against losses when the financial cycle turns to allow credit institutions to offer credit to the actual economy. The Basel III framework requires banks to maintain additional capital during economic upswings and provide a cushion during downturns to improve bank stability and reduce systemic risk.

Resilience of the Spanish Banking System Before and After COVID-19

Pre-Covid-19 Capital Adequacy: The capital adequacy framework, including Common Equity Tier 1 (CET1) and Capital Adequacy Ratio (CAR), is crucial for bank stability. Spanish banks demonstrated strong capital positions, exceeding the minimum requirement of 4.5%, and maintained CAR levels above 8%, indicating a robust capital base capable of withstanding financial shocks during the pre-COVID period based on Banco de España Annual Report 2017 (see Chart 1). Chart 1

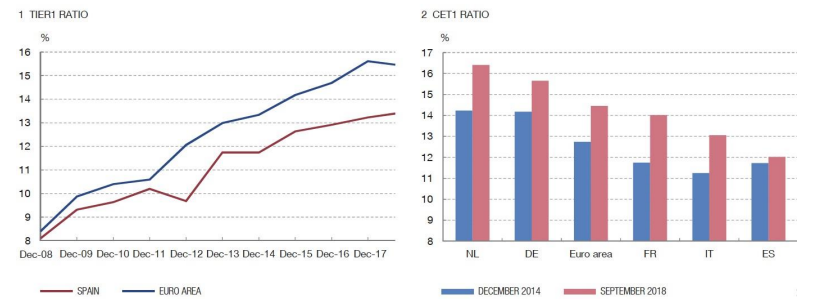

According to Annual Report of Central Bank of Spain (2018), the common equity Tier 1 (CET1) capital ratio declined by 43 basis points over the past year to 12.2%, primarily due to the elimination of temporary adjustments in capital deductions mandated by European regulations during the implementation of the Basel III Accord (go to Chart 2). Chart 2.

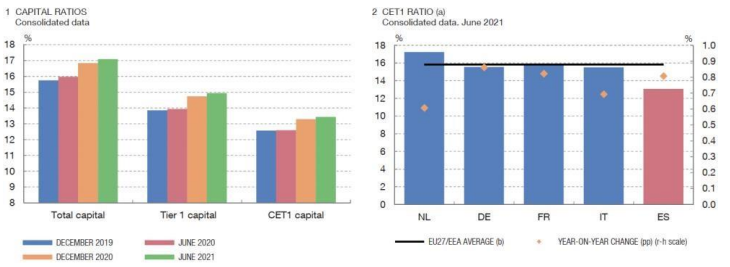

Regarding solvency, the Common Equity Tier 1 (CET1) capital ratio for deposit institutions was 12.6% at the end of 2019, reflecting an increase of 35 basis points (bp) throughout the year, mostly attributable to reserve buildup. In 2019, the average profit ratio of primary Spanish institutions exceeded the EU average; yet, these institutions ranked last regarding the CET1 ratio (Chart 3). Chart 3.

Post-Covid-19 Capital Adequacy: According to Financial Stability Report of Bank of Spain (2021), the CET1 ratio increased by 83 basis points from June 2020 to June 2021, reaching 13.4%, due to an increase in capital and a reduction in RWAs. The change (69 bp) happened mostly in 2020 H2 and was mostly because of the steps the government took to lessen the effects of the health crisis. The common equity tier 1 (CET1) ratio saw an important spike from June 2020 to December 2020, attributed to a 3.6% increase and a reduction in risk-weighted assets (RWAs), mostly as a result of pandemic mitigation strategies. The growth stabilized between December 2020 and June 2021, mirroring the Tier 1 and total capital ratios (see Chart 4).

Bank of Spain looks at the CET1 ratio and CAR to see if they have changed since COVID-19 in their 2022 Financial Stability Review. The CET1 ratio stayed the same, which shows that Spanish banks kept their ratios above 12% after the pandemic, though they were a little lower than the EU standard. This stability shows that banks are putting a lot of effort into keeping a strong capital buffer in case the economy changes.

Pre-Covid-19 Liquidity Positions: By the end of 2019, almost all of Basel III’s first phase criteria will be in force. The NSFR requirement went into effect this year with a minimum level of 100%, whereas the LCR requirement was 80% in 2017 and is 90% in 2018. Regarding liquidity, Spanish banks had an LCR ratio of almost 150%, likewise obviously over the required minimum and in line with the European average. Chart 2.35

Chart 2.35 presents the findings from this analysis, demonstrating that the liquidity situation of Spanish banks is strong, since all banking groups surpass the minimum LCR standards established for 2018 (100%) in both scenarios. The liquidity situation of the less significant institutions is particularly noteworthy, maintaining a ratio of roughly 380% even in favorable scenarios [6].

Post-Covid-19 Liquidity Positions: However, to address liquidity requirements during the pandemic, the Spanish government implemented public guarantee facilities, which substantially increased bank lending. Approximately 60% of the liquidity requirements of Spanish nonfinancial corporations were satisfied through bank loans, with a portion of these loans being state-backed, which accounted for 30% of the firms’ liquidity requirements. The research shows that liquidity assistance measures like TLTRO-IIIs and governmental guarantees have helped banks maintain liquidity and lend post-pandemic. Banks have retained funding sources and maintained a consistent liquidity coverage ratio (LCR) due to assistance, ensuring financial stability in the face of economic uncertainty. In June 2023, SIs had a Liquidity Coverage Ratio (LCR) of 182 percent, above the mandatory minimum. Spanish SIs with significant worldwide presence have lower LCR levels (153 percent in June 2023), comparable to European peers, but still exceeding minimal criteria. Spanish LSIs often have a conservative liquidity profile and stable retail deposits, making them resilient to changes in wholesale market financing conditions. Spanish LSIs have low loan-to-deposit ratios and large liquid asset volumes, making them eligible for monetary operations with the ECB. Overall, their liquidity position (in terms of LCR and NSFR) exceeds regulatory requirements [7].

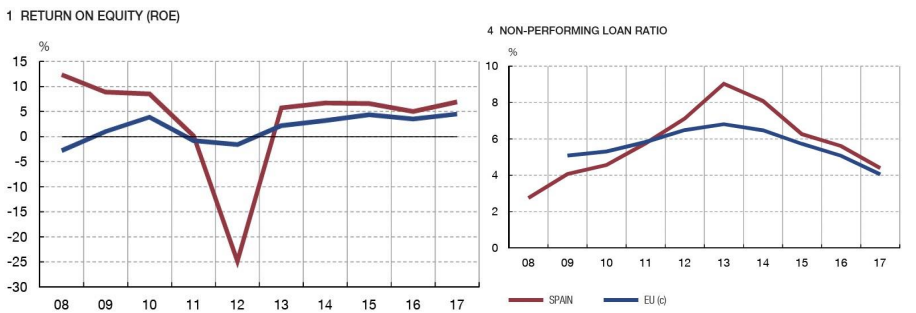

Pre-Covid-19 Profitability: In 2017, the Return on Equity (ROE) for Spanish deposit institutions was 7%, while domestic businesses had a ROE of 5.9%. This data removes the impact of Banco Popular Español’s considerable losses after its resolution by the Single Resolution Board in June of that year. As reported by Annual Report of the Bank of Spain (2017), Spanish credit institutions have lower capital levels and more non-performing loans than their European peers. Despite their recent poor performance, they nevertheless offer a favorable rate of return and efficiency. Spain’s efficiency ratio has fallen in recent years, and rates of return remain historically low (Chart. 6).

In Spain, the NPL ratio has a strong countercyclical trend. During the 2008 global financial crisis, bank credit’s NPL ratio attained a high of 14% in late 2013. In the past five years, it has dropped and currently stands at 4.8% as of end-2019. The NPL ratio is predicted to grow in 2020 [8].

Post-Covid-19 Profitability: The Banco de España reported that the return on equity (ROE) for Spanish banks averaged between 8% to 10% in the years preceding the pandemic. This time was characterized by endeavors to recover from the Eurozone crisis, with banks prioritizing operational efficiencies and cost savings [9]. Spain’s Significant Institutions (SIs) have seen a strong rebound in profitability post-COVID-19, with Return on Equity (ROE) at 12.1% and Return on Assets (ROA) at 0.76%. This growth is attributed to increased net interest income, primarily due to faster interest rate pass-through on loans [10-13]. However, this trend may face reversals due to rising funding costs and economic slowdowns. Monetary policy normalization has led to realized losses in 40% of sovereign debt portfolios held at fair value by SIs. Despite this, credit quality remains resilient, with the nonperforming loans (NPL) ratio decreasing to 3.4% by mid-2023. Sector-specific challenges persist, with high NPLs in hospitality, restaurants, leisure, and construction/ real estate [13-15].

Recommendation

The Bank of Spain should focus on increasing capital adequacy and improving liquidity situations to make Spain’s banking system more stable. Encouraging banks to keep their CET1 ratios well above the legal minimums will protect the economy from shocks and keep things stable even when bad things happen. It is important to strengthen both liquidity coverage ratios (LCR) and net stable funding ratios (NSFR), especially for institutions that deal with a lot of foreign business. With these steps and regular stress tests that look at liquidity in different situations, Spanish banks will be able to keep their liquidity levels high. This will help with both financial stability and keeping operations running smoothly when the market is volatile.

Conclusion

In conclusion, banks play a critical role in managing financial risks and supporting economic stability through effective financial intermediation and diversification strategies. By allocating resources across different sectors and borrowers, banks reduce the impact of potential losses and improve the resilience of the financial system [16]. At the same time, mechanisms such as credit scoring, collateral requirements, monitoring, and guarantees help reduce problems associated with asymmetric information. The introduction of regulatory measures under the Basel III framework has further strengthened the stability of the banking sector. The capital conservation buffer and the countercyclical capital buffer ensure that banks maintain sufficient capital during periods of economic growth and are better prepared to absorb losses during financial downturns. These measures contribute significantly to reducing systemic risk and improving overall financial stability. The comparative analysis of the Spanish banking system shows that banks maintained strong capital adequacy and liquidity positions both before and after the COVID-19 crisis. Government support measures, regulatory flexibility, and improved risk management practices helped banks withstand the economic shock caused by the pandemic [17]. Although profitability fluctuated during this period, the sector demonstrated a relatively strong recovery in the post-pandemic period. Overall, maintaining adequate capital buffers, strong liquidity management, and continuous regulatory supervision remains essential for ensuring the long-term stability and resilience of banking systems in the face of future economic challenges.

References

- Ayeni, O. et al. (2012). Combined Advancement and Single-Lobed Nasolabial Transposition Flaps for a Nasal Sidewall Defect. Dermatologic Surgery, 38 (8), 1386–1389.

- Ahmad, N.H.B. and Ariff, M. (2008). Multi-Country Study of Bank Credit Risk Determinants. International Journal of Banking and Finance, 5 (1).

- Arif, A. (2012). Liquidity Risk and Performance of Banking System. 4 May.

- Nikitenko, A. (2013). Asymmetric information and bank lending: The role of formal and informal institutions (a survey of laboratory research).

- Huang, J. et al. (2021). Risk control mechanisms of third-party guarantee when financing newsvendor. RAIRO - Operations Research, 55 (4), 2337–2358.

- Bank of Spain. (2019). Financial Stability Report. Spring 2019.Banco de España.

- Fund., M. (2024). Spain: Financial Sector Assessment Program-Technical Note on Systemic Risk Analysis. IMF Staff Country Reports, 2024 (259).

- Bank of Spain. (2019). Financial Stability Report. Spring 2019.Banco de España

- Central Bank of Spain. (2022). Annual Report 2021. Banco de España.

- Louis. (2019). Countercyclical Capital Buffers and Financial Crises. Stlouisfed.org.

- Lagaria, K. (2021). Capital Conservation Buffer and Countercyclical Capital Buffer. papers.ssrn.com.

- Bank of Spain. (2017). Financial Stability Report. November 2017. Banco de España.

- Central Bank of Spain. (2023). Financial Stability Report. Autumn 2023. Banco de España.

- Central Bank of Spain. (2024b). Annual Report 2023. Banco de España.

- Central Bank of Spain. (2023a). Annual Report 2022. Banco de España.

- Central Bank of Spain. (2019). Annual Report 2018. Banco de España.

- Central Bank of Spain. (2020). Annual Report 2019. Banco de España.