Current Trends in Business Management(CTBM)

ISSN: 2995-4010 | DOI: 10.33140/CTBM

Research Article - (2026) Volume 4, Issue 1

An Examination of the Timing of Financial Incentives and Audit Committee Strength on the Likelihood to Whistleblow

Received Date: Jan 20, 2026 / Accepted Date: Feb 23, 2026 / Published Date: Mar 04, 2026

Copyright: ©2026 Afia A OPPONG. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: OPPONG, A. A. (2026). An Examination of the Timing of Financial Incentives and Audit Committee Strength on the Likelihood to Whistleblow. Curr Trends Business Mgmt, 4(1), 01-10.

Abstract

The US regulatory environment has various whistleblower programs that allow external fraud reporting, with financial rewards for whistleblowers. However, the period between the initial tip and the reward continues to increase. The Sarbanes–Oxley Act generated an increased focus on audit committees’ roles as monitors of internal whistleblowing processes to encourage internal reporting. This study examines the relationship between the timing of financial incentives (long vs. short), audit committee strength (strong vs. weak), and the likelihood of whistleblowing. A sample of 95 financial professionals indicated a likelihood of whistleblowing regarding potential financial statement fraud. The results indicate that internal whistleblowing is more likely when the audit committee is strong; the respondents associated a strong audit committee with increased protection from retaliation and trust compared to scenarios involving a weak audit committee. This study has implications for firms, regulators, and stakeholders in structuring new and existing whistleblower programs.

Keywords

Whistleblower Incentives, Financial Rewards, Audit Committee Strength, the Timing of Financial Incentives, Whistleblowing Intent, Financial Statement Fraud and Internal vs. External Whistleblowing

Introduction

Whistleblowing is a mechanism that is used to deter fraud. Accordingly, this is an important topic in the accounting literature. Tips are by far the most common initial detection method, exhibiting a 43 percent prevalence rate (Association of Certified Fraud Examiners [1]. According to the ACFE, organizations lose approximately 5% of their annual revenue due to fraud, totaling over $4.7 trillion. Research on whistleblowing channels indicates that whistleblowing can be internal or external and that both channels have important but different implications for firms, regulators, and stakeholders [2]. Specifically, external whistleblowing leads to reputational damage, a negative 2.8 percent market-adjusted five-day stock price reaction, and negative future operating and stock returns following whistleblowing announcements [3]. Internal whistleblowing is preferable for corporations and firms because it allows management to correct misconduct on time and minimize costs [2,4].

To increase reported fraud and provide avenues for reporting, the US government has developed various external programs to report fraud: The Securities and Exchange Commission (SEC), Internal Revenue Service (IRS), and False Claims Act (FCA) federal whistleblower programs provide avenues for external whistleblowing. These programs offer financial incentives for tips that lead to enforcement actions and provide protection against retaliation. Thus, these programs provide a great incentive for individuals who would otherwise not report fraud because of a fear of retaliation. As prior research has noted, fear of retaliation is one of the primary reasons individuals fail to report fraud [5-7]. A survey of US workers showed that the rate of perceived retaliation was 49% percent [8].

Federal whistleblower programs have seen tremendous increases in payouts to whistleblowers over the past decade, signaling a shift in the whistleblower landscape vis-à-vis external whistleblowing. As federal programs expand, the period from the initial tip to the reward for external whistleblowing is growing, and the number of tips is increasing. According to the current trends, it can take several years for whistleblowers to receive rewards. Meanwhile, the timing of the reward can affect external whistleblower intent. Thus, whistleblowing comes with various costs and benefits for the whistleblower [9]. Prior research indicates that perceived personal costs of reporting (PCR) include the risks of counter-reporting, retaliation, and job loss. Further, research shows that the higher the PCR, the lower the reporting intention [10-12]. The timing of the reward can increase the perceived PCR and affect reporting intention. If such a timing becomes an economic cost rather than a reward, it may sway potential whistleblowers from external to internal whistleblowing. Accordingly, research shows that financial incentives can cause whistleblowers to reframe their reporting decisions as an economic rather than an ethical choice [13].

The timing of the reward can affect the potential external whistleblowing. Prior research shows that external whistleblowing comes with costs, such as job loss, reputation, and fear of retaliation. Thus, most whistleblowers weigh their financial, legal, and economic costs and benefits. There are several instances in which lives and careers have been damaged by whistleblowing (Ramirez et al., 2016). If the timing of the reward is known for potential whistleblowers, the added cost of time may lead to increased perceived costs of reporting and sway potential whistleblowers because waiting for a reward may make external whistleblowing less appealing. Prior research shows that whistleblowers perceive a high personal cost of reporting, which leads to decreased reporting [10,12]. Building on the research on the effects of financial incentives on whistleblowing intent, this study addresses the timing of financial rewards and their impact on whistleblowing intention. This information will be beneficial to regulators and governmental agencies, as they work to fine-tune the legislation for whistleblower programs. Audit committees and corporations can also use this information to design or strengthen their internal whistleblower programs by educating employees on external programs and the added costs of external whistleblowing. Research has shown that a high-quality audit committee sets the tone of its internal control environment and functions as an internal recipient of whistleblowing complaints [14]. Therefore, AC actions can affect the likelihood of external or internal whistleblowing. Researchers have noted that an organizational environment that supports whistleblowing facilitates internal whistleblowing [15]. This study examines the timing of financial incentives and audit committee strength in relation to the likelihood of whistleblowing. It also extends the literature on the importance of corporate governance oversight in relation to whistleblower intentions.

To examine the effect of timing of financial incentives (long vs. short) and audit committee strength (strong vs. weak) on the likelihood of whistleblowing, I conducted a 2 × 2 experiment with 95 financial professionals and MBA students as participants. The study participants were industry accounting and finance professionals (accounting, finance, and auditing), who were required to make judgments about fraud. Financial professionals were used as they would understand the case presented, and MBA students have been used as a proxy for financial professionals in prior studies.

The results of this study indicate that knowledge of the timing of financial incentives affects whistleblowers’ decisions to act and leads to internal whistleblowing. The results extend the literature on audit committees’ role in whistleblowing and introduce the timing of financial incentives into whistleblowing literature.The remainder of this paper is organized as follows. Section II presents the hypotheses. Section III provides an overview of the study’s design and methodology. Section IV discusses the results of this study. Finally, Section V discusses the implications and limitations of the study.

Literature Review and Hypotheses

Whistleblowing is defined as the disclosure of illegal, immoral, or illegitimate practices by organizational members (current or former) under their employers' control of persons or organizations, which may affect action [16,17].

Determinants of Whistleblowing

The decision to engage in whistleblowing is complex and has been extensively studied. Whistleblowing motivations are driven, in part, by the evaluation of the costs and benefits associated with the decision, which could include fear of retaliation, financial loss, loss of reputation, difficulty finding employment, and harassment [17-19].

Previous studies have shown a positive relationship between alpha and beta personality traits and whistleblowing, whereas others have shown that women have higher reporting intentions than men [20,21]. This gender difference in reporting intention adds to the complexity of whistleblowing. Additionally, older accountants who have taken ethics classes are more likely to report fraud externally [22]. Further, whistleblowers with a strong sense of moral reasoning and moral obligation to report have stronger reporting intentions [23].

Reporting intentions are lower when the wrongdoer is likable and has a good reputation, whereas auditors are more likely to engage in whistleblowing when the wrongdoer is a coworker than a supervisor [4,24]. Moreover, when the reporting channel is anonymous, reporting intentions are greater for the misappropriation of assets than fraudulent financial reporting [25,26]. However, auditors prefer to report fraud through non-anonymous channels rather than anonymous ones [24]. Auditing and professional firms prefer auditors and professionals to report wrongdoing internally to reduce the negative impacts of reporting. However, outsiders, such as short sellers, politicians, and journalists, prefer to report externally [27]. The characteristics of the organization comprise the last determinant of whistleblowing. Potential whistleblowers must weigh their organization’s characteristics (e.g., how it handles internal whistleblowing, whether it provides incentives, the regulatory environment, and the repercussions of blowing the whistle). Additionally, prior research shows that retaliation leads to higher external reporting of fraud [28].

Fraud Triangle and Whistleblowing

To further probe the whistleblower decision process used a conceptual framework similar to the fraud triangle known as the whistleblower triangle to shed light on whistleblowing motivations [27]. The whistleblower triangle comprises pressure/incentives, opportunities, and rationalization. Pressure and incentives, including moral standards of ethical behavior, media, financial pressures and incentives, professional goals, and reputation goals, can affect the decision to engage in whistleblowing. Meanwhile, financial incentives result in stronger intentions to report fraud externally [27].

However, the opportunity to whistleblow depends on the organization's commitments and procedures for whistleblowing. The lack of commitment and procedures may increase the likelihood of external whistleblowing compared with internal whistleblowing. After a potential whistleblower decides to report fraud, they must weigh the costs and benefits of their decision, including whether the internal or external channel is costlier. Prior research has shown that monetary incentives increase the perceived benefits of whistleblowing and lead to increased reporting intention [29,17].

In the United States, to encourage fraud reporting and the calculation of perceived benefits, the regulatory environment also helps to support potential whistleblowers with protection and financial incentives. Federal whistleblower programs provide avenues for external reporting, and the enactment of the Sarbanes–Oxley Act of 2002 has increased the role of corporations’ audit committees in the oversight of internally reported fraud.

Financial Incentives, Discounting, and Query Theory

Individuals are more likely to report internally than externally [7,26]. External financial incentives and their effects on whistleblowing have been extensively studied. Prior research on financial bounties and reporting intentions shows that the availability of financial rewards affects participants’ reporting intentions [17,22,29]. Found that financial rewards led to higher reporting of questionable acts and participants’ increased willingness to reveal their identity [29]. Found that financial incentives increase the intention to whistleblow to an external authority and that perceptions of fraud seriousness are positively affected by reporting intentions [22]. Found that financial incentives can lead whistleblowers to reframe reporting decisions as economic rather than ethical [13].

This finding suggests that financial rewards motivate external whistleblowing. The provision of internal financial incentives motivates fraud reporting [13]. Such extrinsic motivators can also act as disincentives in certain contexts, hijacking intrinsic motivation [13]. Nevertheless, the timing of the effect of external financial incentives on whistleblower intention remains largely unexamined. The SEC and IRS programs can take several years to complete from the moment a tip is provided, until a reward is offered. Thus, this study modeled the timing of financial incentives as either short- or long-term and their effect on whistleblowing intent. Prior research has shown that whistleblowers face various adverse effects such as job loss, fear of retaliation, financial loss, difficulty finding employment, and harassment [18,19,]. Waiting for a reward for several years can exacerbate these effects. Proposed a model to report questionable behavior [12]. Their model includes three attributes: perceived seriousness of the act, personal responsibility, and PCR. These findings indicate a negative relationship between perceived PCR and reporting intentions. The timing of financial incentives provided by external whistleblower programs has increased tremendously. As SEC and IRS whistleblower programs have increased payouts in recent years, the time taken for payouts has also increased to over ten years in the IRS program (Internal Revenue Service, n.d.).

The decision between short- and long-term rewards has been extensively studied and modeled in economics and psychology literature. Accounting for why individuals may choose a short-term reward over a long-term reward, the economic and psychology literature has focused on intertemporal choice to explain why greater value is placed on short-term rewards than on long-term rewards [30]. Economics researchers frequently use a process called “temporal discounting” to explain the choice for the short term over the long term [30]. Temporal discounting involves a decrease in the subjective value of a reward as the delay in its receipt increases [31]. Further, when people choose between long and short terms, they frequently weigh the immediate consequences of their decisions more heavily than the delayed consequences [31]. In summary, the concept of temporal discounting addresses why people prefer to be given money now, rather than later. In subjectively valuing timed rewards, future payments are described as being “discounted [32].”

In economic theory, the discounted utility theory model has been used to explain why individuals choose a short-term reward over the long term [30]. In this model, the time preference rate is assumed to be constant, causing the future value to devalue over the current value [30]. Various other models have been used to explain the discounting effect, such as hyperbolic and quasi-hyperbolic models, which do not assume a constant rate of diminishing utility, but a higher discounting rate for events closer in time [30]. These economic theory models suggest that individuals choose short-term rewards over long-term rewards because of the discount effect [30].

Query theory emphasizes the role of memory retrieval in decision making regarding time preference to explain the cognitive process that underlies decision making regarding time preferences [30]. This theory posits that decision makers query their memories of information relevant to a decision. However, owing to output interference, retrieval is less successful for later queries than for earlier queries, thus influencing the decision preference for the current versus future timing. These theories imply a preference for short-term timings.

Moreover, this study conducted research on financial incentive timing as a PCR. The timing of financial incentives is a critical factor in determining whether potential whistleblowers engage in internal or external whistleblowing. If the reward takes several years to be provided, it may affect the whistleblowers’ motivation and judgment. Considering the timing of financial incentives as a perceived PCR, the timing of financial incentives in the long-versus short-term may affect reporting intentions. Also examine auditors’ intentions to report fraud when PCR is perceived [10]. They found a negative relationship between perceived cost of reporting and reporting intentions. They found that low and high PCR levels might lead to fraudulent reporting. Thus, according to, short-term incentive timing has a lower PCR than does long-term incentive timing [10,12].

Therefore, I test the following hypothesis:

H1: Short-term timing of financial incentives is associated with increased whistleblowing.

Audit Committees and Whistleblowing

Organizational commitment and other factors can promote whistleblowing and deter fraud. An audit committee oversees whistleblowing cases and the procedures it implements for reporting and investigating reported fraud can serve as a catalyst for whether individuals engage in internal or external whistleblowing. The primary organizational factor analyzed in this study was the audit committee.

Audit committee characteristics such as independence, expertise, composition, frequent meetings, and size have been empirically researched over the years to establish criteria for distinguishing between strong and weak audit committees [33,34].

Research has shown that the audit committee functions as a gatekeeper, ensuring that reported fraud is investigated and whistleblowers are not retaliated against [35]. Research has noted that an organizational environment that supports whistleblowing facilitates internal whistleblowing [15]. Prior research has established that fear of retaliation is one of the primary reasons why individuals fail to report fraud, and that reporting intentions are lower when there is a threat of retaliation [5-7,22]. By overseeing the financial reporting process, a strong audit committee is more likely to investigate fraud and reduce retaliation risk [2]. Find that a high-quality audit committee is associated with a lower probability of external whistleblowing and a lower likelihood of retaliation. Additionally, research has established that internal whistleblowing is more likely when the threat of retaliation is low [18,36].

Additionally, following the enactment of the Dodd–Frank Act, the SEC implemented rules that enabled the audit committee to take legal action against employers who retaliated against whistleblowers (US SEC, 2020). A strong audit committee ensures that the management does not retaliate against potential whistleblowers, leading to decreased retaliation. Prior research has also shown that a strong audit committee will ensures that internally reported misconduct is investigated and resolved [28]. Moreover, a high-quality audit committee is associated with the implementation of a stronger whistleblowing system, which leads to increased internal whistleblowing [28]. Further, prior research has shown that internal whistleblowing is encouraged when employees perceive that management will investigate and correct wrongdoing and support an atmosphere that encourages disclosure [15].

A key characteristic of a strong audit committee is regular communication with management and internal and external auditors, which fosters information sharing and helps ensure that issues and reports of fraud are addressed in a timely manner [37]. Prior research has established that a higher-quality audit committee is likely to make better decisions when investigating fraud because it is not susceptible to management influences compared with a lower-quality audit committee, which leads to a lower likelihood of external whistleblowing [28]. A strong audit committee makes the right decisions regarding fraud investigation, leading to increased organizational support for whistleblowing. Prior research on organizational support and whistleblowing has also shown that high organizational support leads to internal whistleblowing [11,38]. Based on the research cited above, I propose the following hypothesis:

H2: Relative to external whistleblowing, internal whistleblowing is more likely to occur when the audit committee is strong.

H3: Relative to external whistleblowing, internal whistleblowing is more likely when the

Method

Participants

There were 199 responses to the survey via an anonymous link and 185 participants consented to participate in the study. Of these, 95, who fully completed the study, passed the comprehension checks and were included in the study.

Participants were obtained primarily through the following avenues: (1) past and present finance colleagues of the author; (2) LinkedIn, an Internet platform for professionals to solicit participants; (3) networking of colleagues; (4) MBA students; and (5) financial professionals through the Qualtrics Research Panel.

Table 1 presents the demographic characteristics. The participants were predominantly female (61 percent); college graduates with a bachelor’s degree or higher represented 85 percent of the sample, and 88 percent had more than five years of professional experience. Of the participants, 45 percent had professional certifications such as CPA, CMA, CGMA, CFA, or CIA, whereas 31 percent had a CPA license.

|

Gender |

Male |

(n) 32 |

% 34 |

|

|

Female |

58 |

61 |

|

|

Other |

5 |

5 |

|

Professional Experience (Years) |

< 5 |

11 |

11 |

|

|

5–15 |

41 |

43 |

|

|

16–25 |

31 |

33 |

|

|

> 25 |

11 |

12 |

|

|

Not Disclosed |

1 |

1 |

|

Professional Certification |

CPA |

29 |

31 |

|

|

Other (CMA, CGMA, CFA, CIA, CFE) None |

21

52 |

22

53 |

|

Highest Educational Degree Earned |

< Associate’s Degree |

13 |

14 |

|

|

Bachelor’s Degree |

36 |

38 |

|

Type of Current Organization |

Advanced Degree (some master’s, master’s, or doctoral) Private for |

46

41 |

48

44 |

|

|

Public Company |

18 |

19 |

|

|

Not-For-Profit Company Governmental |

8

8 |

9

9 |

|

|

Public Accounting |

8 |

9 |

|

|

Other (please specify) |

6 |

6 |

|

|

Prefer not to disclose |

5 |

5 |

Table 1: Participants’ Demographic Characteristics

Design and Instrument

This study examined whistleblower intent using a 2 × 2 factorial between-subjects design with respect to the timing of financial incentives (long vs. short term) and audit committee strength (strong vs. weak). The participants were randomly assigned to four experimental tasks.

Participants received a vignette with a realistic case of a company in the manufacturing sector. Background information on the company, industry, and key performance history is provided. In addition, the case included a management compensation structure and whistleblower issues.The case materials for the whistleblower incident were developed after a review of various whistleblower studies and were adapted from [39]. The case study involves a publicly traded company with a steady performance history. The case vignette provided a brief description of the structure of the management team, the financial reporting team, and the review process for financial statements. The whistleblower incident involved financial-statement fraud related to expenses.

Development of the Primary Independent Variable: Timing of Financial Incentive (TIMING)

In this study, the added cost of whistleblowing was emphasized because of the timing of the financial incentives. As the effect of the timing of external financial incentives on whistleblower intentions remains largely unexamined, the variable was adapted using a combination of prior studies on whistleblower financial and the SEC’s whistleblower reports to Congress [23,25,29,36].

Since TIMING is a new variable not tested in the accounting literature, the study participants were asked the following question: “In the case you just analyzed, please indicate the timing of receiving the financial reward (incentive). The endpoints are labeled ‘1 = short’ and ‘7 = long’.” As expected, the analysis of the effect size for each manipulation indicated that the timing of the reward was distinct between the vignettes.

Second Independent Variable: Audit Committee Strength (AC STRENGTH)

The vignette for the independent variable audit committee strength was adapted from a previous study [40]. Additionally, prior research analyzed the characteristics of a strong audit committee, such as expertise, composition, size, independence, integrity, and objectivity, which formed the basis of the strong vs. weak audit committee strength in this study [33]. To adequately assess the manipulation of the strength of the audit committee, participants were asked, “In the case you just analyzed, please indicate the strength of the audit committee. The endpoints are labeled ‘1 = weak’ and ‘7 = strong’.” As expected, the analysis of the effect size for each manipulation indicated that the strength of the audit differed between the vignettes.

Dependent Variable: Likely to Report Internally or Externally (LIKELY_BOTH)

The dependent variable was the likelihood of participants reporting fraud through whistleblower channels established by the company’s audit committee or externally through the SEC’s tips, complaints, and referral hotlines. The question had endpoints labeled “1 = Likely to report internally to the company’s audit committee,” with a mid-point of “4 = Labeled neither report internally or externally” and “7 = Likely to report externally to the SEC” (LIKELY_BOTH).

Results

Comprehension Checks

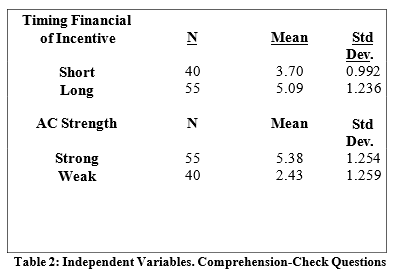

Participants were asked two comprehension-check questions to assess their comprehension of the case, and the independent variables (AC STRENGTH and TIMING) were adequately captured. On the basis of the comprehension check questions, 24 participants were excluded from the survey. Most of the short-term timing and AC strength –weak condition participants failed the comprehension checks. Therefore, it is difficult to assess why more respondents failed the comprehension checks in the short-term condition. However, based on the analysis of question 14 of the survey, which asked participants to describe the impact of the timing on their decision to whistleblow, participants in the short-term condition felt that the reward should be more immediate, and the timing was still lengthy in the short-term treatment condition. After deleting all participants who failed the comprehension checks, a one-way ANOVA was performed for the comprehension check questions relating to TIMING and AC STRENGTH. For TIMING, the difference in means was in the expected direction and significant (F (2, 93) =34.350, p =.000). The difference in means was in the expected direction for the second independent variable, AC STRENGTH, and was significant (F (1, 93) =128.302, p=000). Table 2 presents the means of the independent variables. The difference in the means for both questions indicates successful experimental manipulation [40]. For TIMING, the mean for the short-term condition was 3.70, whereas the mean for the long-term condition was 5.09. For AC STRENGTH, the mean for AC - STRENGTH – STRONG WAS 5. 38, and for AC - STRENGTH – WEAK condition, the mean was 2.43.

Descriptive Results

Univariate Results

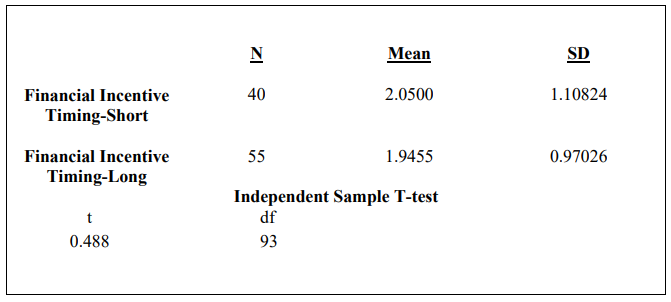

The first hypothesis predicted that short-term financial incentives would be associated with increased whistleblowing, both internally and externally. To test H1, a new variable was computed based on a scale of four to determine whether H1 was supported. First, the original dependent variable was reentered and recoded to approximately zero to create a new variable. Subsequently, an absolute value for the new number is computed to create a new variable for testing H1, which transforms the original results for comparison. Finally, an independent-sample t-test was performed to test this hypothesis. Table 3 presents the results. The mean value of the transformed variable for TIMING-SHORT was 2.050, and that for TIMING-LONG, was 1.9455; however, the model was not significant (t < 1.00), indicating that H1 was not supported. Table 3 shows the results of the t-tests for H1.

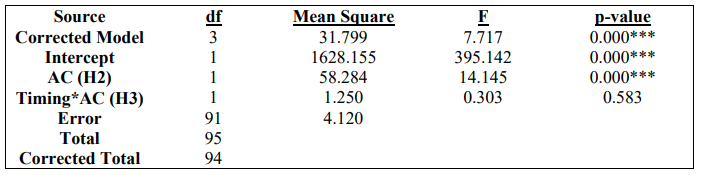

H2 posits that relative to external whistleblowing, internal whistleblowing is more likely when the audit committee is strong. The results in Table 4 indicate that when AC STRENGTH is strong, it is associated with increased internal whistleblowing with a mean value of 3.51, supporting H3. Furthermore, the F (1, 91) value was 14.145 and the p-value was .000, indicating statistical significance at the .01 level, thus supporting hypothesis H2. H3 posited that internal whistleblowing is more likely than external whistleblowing when the external financial incentive timing is long term and the AC is strong. However, the analysis of variance model did not show practical or statistical significance for the interaction of the two independent variables, TIMING and AC STRENGTH (TIMING*AC STRENGTH). Therefore, H3 was not supported, as shown in Table 4. The F-value for the TIMING × AC STRENGTH interaction was 0.583.

Table 3: Independent variable descriptive statistics—How likely are you to report fraud internally to AC or externally to the SEC (Recoded using LIKELY_BOTH – Minus 4 Midpoint)

*** Significant at the 0.01 level (2-tailed)

Table 4: Dependent Variable (Likely_Both)

Supplemental Results

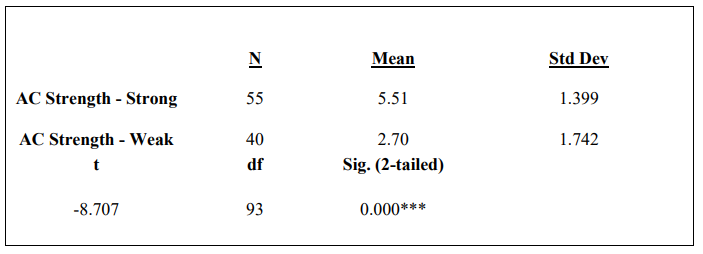

In this study, participants were asked two questions related to threats of trust and retaliation. The questions were scored on a seven-point scale. The mean value for a strong AC was 5.51, while the weak AC had a mean value of 2.70. This finding supports prior research that shows that organizational trust can mediate wrongdoing reporting. Table 5 shows the mean values for AC STRENGTH–STRONG and WEAK and the associated results.

When participants were asked “Please indicate whether the audit committee will protect the reporters of fraud from retaliation?”

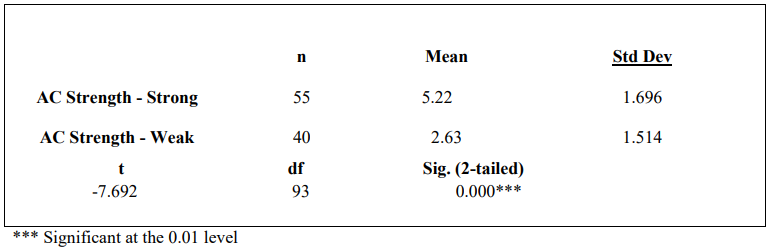

The endpoints were measured as “1 = will not protect against retaliation” and “7 = will protect against retaliation.” The independent-samples t-test results showed significance at p < 0.01 level, as shown in Table 5. The main effect of AC strength was significant (p < 0.01). Table 6 shows that participants indicated that a strong AC would likely protect against retaliation, supporting prior research on retaliation threats and a strong AC. The mean value for strong AC was 5.22 on a seven-point scale, while that for weak AC was 2.63. the Financial Likelihood.

Table 5: Trust in the Audit Committee

Table 6: Belief in Whether the Audit Committee Will Protect the Reporters of Fraud from Retaliation

Discussion and Conclusion

When faced with an act of wrongdoing, individuals may choose to report it, either internally or externally. This study examined two factors that potential whistleblowers must contend with: the timing of financial incentives and the internal corporate mechanism of the corporation, that is, the audit committee. The findings indicate that a strong audit committee is associated with the likelihood of internal whistleblowing, and provide further evidence that a strong audit committee is associated with more trust and a lower likelihood of retaliation. The findings provide further empirical evidence and support prior literature showing that an organizational environment that supports whistleblowing facilitates internal whistleblowing [15]. These findings support prior literature revealing that the audit committee can function as a gatekeeper to ensure that reported fraud is investigated and whistleblowers are not retaliated against [35]. This study also supports prior research showing that when the threat of retaliation is low, it leads to more internal whistleblowing [18,36].

Similar to other experimental studies, this study had various limitations due to its design and survey research, which were limited to external validity, sample size, sample representation, and the potential for demand effects. This study considered only the economic costs and benefits of whistleblowing, and not the effects of social, legal, and psychological costs on reward timing. Finally, whistleblower behavior is complex; thus, modeling the economic aspects (financial incentives) of decision making may have been a limitation.

This study extends the literature on audit committees’ role in whistleblowing by introducing the timing of financial incentives. Future research can explore the effect of an immediate reward on reporting intentions, and whether expectations related to receiving a reward from a governmental agency may affect whistleblowing intentions. Finally, future research could examine the effects of psychological and social factors, and the timing of financial incentives on the impact of internal and external whistleblowing.

Funding: This research received no specific grant from any funding agency.

Conflict of Interest: The authors declare no conflict of interest.

Data Availability Statement: Data available upon reasonable request.

AI Usage Statement: Generative AI tools were used to convert references from the Chicago 16th format to the APA 7th Edition.

References

- Association of Certified Fraud Examiners. (2024). Report to the nations: 2024 global study on occupational fraud and abuse.

- Lee, G., & Xiao, X. (2018). Whistleblowing on accountingy-related misconduct: A synthesis of the literature. Journal of Accounting Literature, 41(1), 22-46.

- Bowen, R. M., Call, A. C., & Rajgopal, S. (2010). Whistleblowing: Target firm characteristics and economic consequences. The Accounting Review, 85(4), 1239-1271.

- Taylor, E. Z., & Curtis, M. B. (2013). Whistleblowing in audit firms: Organizational response and power distance. Behavioral Research in Accounting, 25(2), 21-43.

- Lauck, J. R., Perreault, S. J., Rakestraw, J. R., & Wainberg,J. S. (2020). Strategic audit inquiry: The impact of timing and the promotion of statutory protections on client fraud disclosures. Accounting Horizons, 34(3), 153-167.

- Near, J. P., & Miceli, M. P. (1986). Retaliation against whistle blowers: Predictors and effects. Journal of applied psychology, 71(1), 137.

- Hooks, K. L., Kaplan, S. E., & Schultz Jr, J. J. (1994). Enhancing communication to assist in fraud prevention and detection. Auditing: A Journal of Practice & Theory, 13(2).

- Ethics Resource Center. (2024). ECI’s global business ethics survey.

- Miceli, M. P., Near, J. P., & Dworkin, T. M. (2008). Whistleblowing in organizations. Psychology Press.

- Kaplan, S. E., & Whitecotton, S. M. (2001). An examination of auditors' reporting intentions when another auditor is offered client employment. Auditing: A Journal of Practice & Theory, 20(1), 45-63.

- Latan, H., Ringle, C. M., & Jabbour, C. J. C. (2018). Whistleblowing intentions among public accountants in Indonesia: Testing for the moderation effects. Journal of business ethics, 152(2), 573-588.

- Schultz, J. J., Johnson, D. A., Morris, D., & Dyrnes, S. (1993). An investigation of the reporting of questionable acts in an international setting. Journal of Accounting research, 31, 75-103.

- Berger, L., Perreault, S., & Wainberg, J. (2017). Hijacking the moral imperative: How financial incentives can discourage whistleblower reporting. Auditing: A Journal of Practice & Theory, 36(3), 1-14.

- Turley, S., & Zaman, M. (2007).Audit committee effectiveness: informal processes and behavioural effects. Accounting, Auditing & Accountability Journal, 20(5), 765-788.

- Miceli, M. P., & Near, J. P. (1984). The relationships among beliefs, organizational position, and whistle-blowing status: A discriminant analysis. Academy of Management journal, 27(4), 687-705.

- Near, J. P., & Miceli, M. P. (1985). Organizational dissidence: The case of whistle-blowing. Journal of business ethics, 4(1), 1-16.

- Xu, Y., & Ziegenfuss, D. E. (2008). Reward systems, moral reasoning, and internal auditors’reporting wrongdoing. Journal of Business and Psychology, 22(4), 323-331.

- Young, R. F. (2017). Blowing the whistle: Individual persuasion under perceived threat of retaliation. Behavioral Research in Accounting, 29(2), 97-111.

- Wainberg, J., & Perreault, S. (2016). Whistleblowing in audit firms: Do explicit protections from retaliation activate implicit threats of reprisal? Behavioral Research in Accounting, 28(1), 83–93.

- Brink, A. G., Cereola, S. J., & Menk, K. B. (2015). The effects of personality traits, ethical position, and the materiality of fraudulent reporting on entry-level employee whistleblowing decisions. Journal of Forensic & Investigative Accounting, 7(1), 180-211.

- Brown, J. O., Hays, J., & Stuebs Jr, M. T. (2016). Modeling accountant whistleblowing intentions: Applying the theory of planned behavior and the fraud triangle. Accounting and the Public Interest, 16(1), 28-56.

- Andon, P., Free, C., Jidin, R., Monroe, G. S., & Turner, M. J. (2018). The impact of financial incentives and perceptions of seriousness on whistleblowing intention. Journal of business ethics, 151(1), 165-178.

- Stikeleather, B. R. (2016). When do employers benefit from offering workers a financial reward for reporting internal misconduct?. Accounting, Organizations and Society, 52, 1-14.

- Robertson, J. C., Stefaniak, C. M., & Curtis, M. B. (2011). Does wrongdoer reputation matter? Impact of auditor-wrongdoer performance and likeability reputations on fellow auditors' intention to take action and choice of reporting outlet. Behavioral Research in Accounting, 23(2), 207-234.

- Brink, A. G., Lowe, D. J., & Victoravich, L. M. (2013). The effect of evidence strength and internal rewards on intentions to report fraud in the Dodd-Frank regulatory environment. Auditing: A Journal of Practice & Theory, 32(3), 87-104.

- Kaplan, S., Pany, K., Samuels, J., & Zhang, J. (2009). An examination of the association between gender and reporting intentions for fraudulent financial reporting. Journal of Business Ethics, 87(1), 15-30.

- Smaili, N., & Arroyo, P. (2019). Categorization of whistleblowers using the whistleblowing triangle. Journal of Business Ethics, 157(1), 95-117.

- Lee, G., & Fargher, N. L. (2018). The role of the audit committee in their oversight of whistle-blowing. Auditing: A Journal of Practice & Theory, 37(1), 167-189.

- Pope, K. R., & Lee, C. C. (2013). Could the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010 be helpful in reforming corporate America? An investigation on financial bounties and whistle-blowing behaviors in the private sector. Journal of business ethics, 112(4), 597-607.

- Irving, K. (2009). Overcoming shortâ?termism: Mental time travel, delayed gratification and how not to discount the future. Australian Accounting Review, 19(4), 278-294.

- Green, L., Myerson, J., Oliveira, L., & Chang, S. E. (2013). Delay discounting of monetary rewards over a wide range of amounts. Journal of the experimental analysis of behavior, 100(3), 269-281.

- Doyle, J. R. (2013). Survey of time preference, delay discounting models. Judgment and Decision making, 8(2), 116-135.

- Seetharaman, A., Wang, X., & Zhang, S. (2014). An empirical analysis of the effects of accounting expertise in audit committees on non-GAAP earnings exclusions. Accounting Horizons, 28(1), 17-37.

- Wilbanks, R. M., Hermanson, D. R., & Sharma, V. D. (2017). Audit committee oversight of fraud risk: The role of social ties, professional ties, and governance characteristics. Accounting Horizons, 31(3), 21-38.

- Cohen, J., Gaynor, L. M., Krishnamoorthy, G., & Wright, A.M. (2007). Auditor communications with the audit committee and the board of directors: Policy recommendations and opportunities for future research. Accounting Horizons, 21(2), 165-187.

- Guthrie, C. P., & Taylor, E. Z. (2017). Whistleblowing on fraud for pay: Can I trust you?. Journal of Forensic Accounting Research, 2(1), A1-A19.

- Cohen, J., Krishnamoorthy, G., & Wright, A. (2010). Corporate governance in the postâ?Sarbanesâ?Oxley era: Auditors’ experiences. Contemporary Accounting Research, 27(3), 751-786.

- Alleyne, P., Hudaib, M., & Haniffa, R. (2018). The moderating role of perceived organisational support in breaking the silence of public accountants. Journal of Business Ethics, 147(3), 509-527.

- Brink, A. G., Lowe, D. J., & Victoravich, L. M. (2017). The public company whistleblowing environment: Perceptions of a wrongful act and monetary attitude. Accounting and the Public Interest, 17(1), 1-30.

- Brown-Liburd, H. L., & Wright, A. M. (2011). The effect of past client relationship and strength of the audit committee on auditor negotiations. Auditing: A Journal of Practice & Theory, 30(4), 51-69.

- U.S. Securities and Exchange Commission. (2018). Annual report to Congress: Whistleblower program.

- Department of the Treasury, Internal Revenue Service. (2019). Whistleblower program: Fiscal year 2019 annual report to Congress.

- Felo, A. J., Krishnamurthy, S., & Solieri, S. A. (2003). Audit committee characteristics and the perceived quality of financial reporting: an empirical analysis. Available at SSRN 401240.

- Internal Revenue Service. (n.d.). Whistleblower program:Fiscal year 2019 annual report to Congress.

- KPMG. (n.d.). Fraud and whistleblowing.

- Near, J. P., & Miceli, M. P. (1995). Effective-whistle blowing. Academy of management review, 20(3), 679-708.

- Ramirez, M. K. (2007). Blowing the whistle on whistleblower protection: A tale of reform versus power. U. Cin. L. Rev., 76, 183.

- Seifert, D. L., Stammerjohan, W. W., & Martin, R. B. (2014). Trust, organizational justice, and whistleblowing: A research note. Behavioral Research in Accounting, 26(1), 157-168.

- Seifert, D. L., Sweeney, J. T., Joireman, J., & Thornton,J. M. (2010). The influence of organizational justice on accountant whistleblowing. Accounting, Organizations and Society, 35(7), 707-717.

- The CPA Journal. (1998, December).

- U.S. Securities and Exchange Commission. (2020).Whistleblower retaliation.