Journal of Democracy Research(JDR)

ISSN: 3070-4006 | DOI: 10.33140/JDR

Research Article - (2026) Volume 2, Issue 1

The Role of Green Finance in Vietnam’s Integrated Economic Development Model

Received Date: Feb 02, 2026 / Accepted Date: Mar 06, 2026 / Published Date: Mar 16, 2026

Copyright: ©2026 Huynh Thanh Dien. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Dien, H. T. (2026). The Role of Green Finance in Vietnam

Abstract

The study analyzes the role of Climate Finance (CF) and Environmental, Social, and Governance (ESG) in Vietnam’s integrated growth model for the period 2025–2030. Building on the theories of endogenous growth, new institutional economics, and global value chains, the paper develops a three-layer analytical framework: the international context; three intermediate pillars (climate finance, institutional–data coordination, and geo-economic positioning); and direct factors (ESG, technology, and human resources). The analysis shows that Vietnam has opportunities to mobilize international resources (JETP, green credit, GSS bonds, carbon market), but absorption capacity remains limited due to fragmented institutions, lack of transparent data, and weak technological and human resource capabilities. Accordingly, the study proposes viewing climate finance and ESG not as external pressures but as endogenous drivers to enhance total factor productivity (TFP), increase domestic value added (DVA), and expand access to international markets. Policy implications emphasize institutional reform for coordination, the development of MRV systems and carbon markets, the expansion of green finance channels, and improvements in workforce quality.

Keywords

Climate Finance, ESG, Integrated Growth, JETP, Carbon Market, Vietnam, Economy, Research Methodology ICAP

Introduction

Over the past two decades, Vietnam has regarded international economic integration as a strategic lever to foster growth, with the goal of becoming a high-income industrialized nation by the mid-21st century. By 2025, Vietnam had signed 17 free trade agreements (FTAs), including several next-generation FTAs such as the CPTPP and EVFTA, while also strengthening comprehensive strategic partnerships with major economies. These steps have opened opportunities to expand export markets, attract foreign investment, and participate more deeply in global value chains. Alongside these opportunities, integration also presents stringent challenges in terms of sustainable development. International mechanisms such as the European Union’s Carbon Border Adjustment Mechanism (CBAM) and emission-related Monitoring, Reporting, and Verification (MRV) systems have become mandatory conditions for market access. This constitutes a significant barrier for many domestic firms that rely on low-cost advantages and remain unprepared for the green transition.

At the same time, higher environmental standards create new spaces for development. On the one hand, they serve as prerequisites for attracting high-quality green FDI; on the other, they compel domestic firms to adopt low-carbon technologies, strengthen ESG (Environmental, Social, Governance) practices, and integrate more deeply into higher value-added segments of global supply chains. Thus, international integration represents both pressure and a historic opportunity for Vietnam to restructure its growth model toward green–digital integration. However, the financing challenge for the green transition remains urgent and difficult. The costs of investing in low-carbon technologies, renewable energy infrastructure, MRV systems, and ESG compliance exceed the capacities of most small and medium-sized enterprises.

Although Vietnam has accessed certain international resources, most notably the Just Energy Transition Partnership (JETP) with a commitment of USD 15.5 billion through 2030, the country’s absorptive capacity for green capital remains limited due to fragmented policies and a lack of transparent coordination mechanisms. This study aims to clarify the role of Climate Finance (CF) and ESG (Environmental, Social, Governance) in Vietnam’s green transition, while analyzing the practical challenges of mobilizing and absorbing international resources such as JETP, green finance, and the carbon market.

On this basis, the paper proposes an integrated growth model in which climate finance and ESG are not merely external compliance requirements but endogenous drivers of sustainable development. The study is expected to provide both a theoretical framework and policy implications to help Vietnam build effective coordination institutions, transparent MRV (Monitoring, Reporting, Verification) systems, and a domestic carbon market, thereby leveraging international integration as a strategic pathway to become a regional hub for green–digital production.

Thereotical Foundations and Analytical Framework

Theoretical Foundations

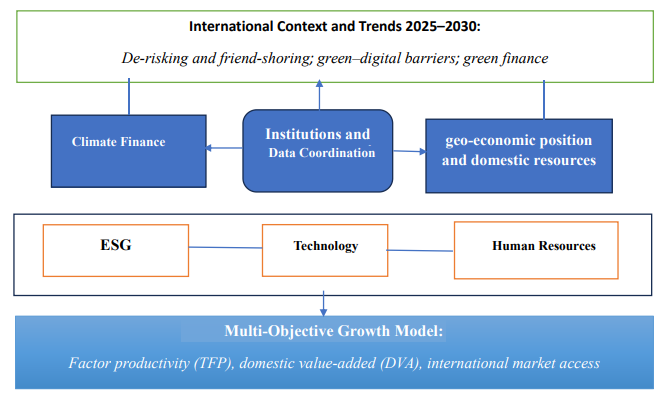

This study draws on a combination of modern economic and management theories to construct an analytical framework for Vietnam’s integrated growth model in the era of green–digital integration. The international context and trends for 2025–2030 provide the starting point, including de-risking and friend-shoring, the emergence of green–digital trade barriers, and the global reallocation of capital flows into green finance. These dynamics present both opportunities and challenges for Vietnam: the chance to attract green FDI, but also barriers for domestic firms that are not yet prepared for ESG compliance or MRV systems. From a theoretical perspective, endogenous growth theory underscores the role of knowledge, technology, and human capital in enhancing total factor productivity (TFP) [1].

This provides the foundation for emphasizing technology and human resources as two endogenous pillars of growth within the framework. New institutional economics highlights that institutions and coordination mechanisms determine the efficiency of resource allocation [2]. Therefore, institutional quality and interoperable data must be placed at the center to ensure that climate finance and domestic resources are allocated transparently, based on outcomes rather than inputs.

Global value chain theory demonstrates that, to capture more value, a country must upgrade into higher value-added segments [3]. For Vietnam, this is tied to ESG compliance and participation in carbon markets, which can raise domestic value added (DVA) and secure more sustainable international market access. Furthermore, research on the green economy and ESG affirms that ESG is not merely a reporting standard but also a strategic framework for attracting green finance and shaping corporate innovation [4,5].

This is why ESG is considered one of the three key intermediary factors in the framework, alongside technology and human resources. Carbon markets and MRV mechanisms show that emissions are increasingly priced as a trade cost, establishing a direct link between climate finance and market access, while incentivizing investment in low-carbon technologies. Finally, the concept of the integrated growth model, discussed in recent deliberations at the “Vietnam Economic Outlook 2025–2030” conference, has concretized the connections among climate finance, institutions, geo-economic positioning, ESG, technology, and human resources, with the aim of simultaneously enhancing three indicators: TFP, DVA, and international market access [6,7].

Analytical Framework of the Study

The analytical framework is grounded in the theories of endogenous growth, new institutional economics, global value chains, as well as contemporary research on the green economy, ESG, and carbon markets. In the international context of 2025–2030, de-risking, the rise of green–digital barriers such as CBAM and MRV, and the global reallocation of capital flows toward green finance create both opportunities and pressures for Vietnam [1-3].

Against this backdrop, three intermediate pillars are identified: (i) climate finance, including sources such as JETP, green ODA, green bonds, and green FDI; (ii) institutions and interoperable data, to ensure transparency, reduce transaction costs, and strengthen absorptive capacity; (iii) geo-economic positioning and domestic resources, which form the foundation for Vietnam’s role in global green value chains. Building on these pillars, three direct factors are activated: ESG as a compliance framework and competitive strategy; technology as the driver of TFP through low-carbon innovation and digitalization; and human resources as the condition for improved governance and technological absorption.

The convergence of these factors results in an integrated, multi-objective growth model, aimed at simultaneously improving TFP, increasing DVA, and strengthening international market access. This analytical framework directly supports the study’s objective of transforming climate finance and ESG from external compliance pressures into endogenous drivers, thereby providing the foundation for sustainable growth and deeper integration of Vietnam in the coming period.

Figure 1: Analytical Framework of the Role of Green Finance in Vietnam’s Integrated Economic Development Model (Source: Author’s proposal).

Research Methodology ICAP

The study employs a qualitative analysis combined with secondary data sources. The data include: (i) foundational theories; (ii) international reports on the green economy, ESG, and carbon markets; (iii) Vietnamese policies and legal documents; and (iv) statistical data from the State Bank of Vietnam, the Ministry of Natural Resources and Environment. Content analysis is applied to systematize, compare, and develop a three-layer analytical framework: the international context; three intermediate pillars (climate finance, institutions–data, geo-economic positioning); and direct factors (ESG, technology, human resources). In addition, some descriptive statistics are used to illustrate practical realities. The limitation of this method lies in the lack of quantitative data for verification; therefore, the findings are primarily directional and serve as policy suggestions.

Green Finance in Vietnams Integrated Economic Development Model

International Context and Implications for Vietnam

During the 2025–2030 period, the international economic and political landscape is undergoing profound changes that directly affect the development models of emerging economies, including Vietnam. Three prominent trends can be identified. First, the restructuring of global supply chains, with an emphasis on de-risking and friend-shoring. Multinational corporations are increasingly cautious in allocating value chains, aiming to reduce geopolitical risks and enhance supply stability. This trend creates opportunities for Vietnam to become an alternative destination, thanks to its strategic geographic position, abundant labor force, and extensive FTA network (17 agreements signed). However, these opportunities can only be fully realized if Vietnamese enterprises comply with new standards on environment, labor, and governance.

Second, the rise of green–digital trade barriers in international commerce. The European Union has launched the Carbon Border Adjustment Mechanism (CBAM), requiring exporters to measure, report, and verify (MRV) their carbon emissions. Major markets such as the United States, Japan, and Canada also enforce stringent Environmental, Social, and Governance (ESG) standards across supply chains. As a result, Vietnam’s low-cost advantage is diminishing, while competitiveness increasingly depends on firms’ ability to comply with green standards. For key export sectors such as steel, cement, textiles, and seafood, this poses significant pressure but also an opportunity to restructure toward clean technologies and transparent data.

According to Figure 1, exports of CBAM-covered products from non-EU countries increased significantly between 2019 and 2023. Vietnam, with products such as steel, aluminum, and cement, falls into categories heavily affected. This indicates that CBAM has already become a real barrier, compelling firms to prepare for ESG compliance and data transparency.

Figure 2: Export Data of CBAM-Affected Products to the EU, 20123 vs. 2019 (Source: Policy Brief “Learning from CBAM’s transitional phase,” CER, 2024)

Third, the global reallocation of capital flows toward green sectors. Reports by UNCTAD (2024) and ICAP (2024) show that the share of green foreign direct investment (FDI) and climate finance in total global investment is rising significantly. International financial institutions also prioritize funding renewable energy projects, low-carbon infrastructure, and green technologies. This creates opportunities for Vietnam to access new resources, clearly reflected in the Just Energy Transition Partnership (JETP), which commits USD 15.5 billion in support by 2030. However, the absorptive capacity for these resources depends on the degree of institutional coordination, the development of a national MRV system, and the ESG management capacity of enterprises.

Overall, the current international context exerts pressure while also offering historic opportunities for Vietnam. Green–digital barriers may reduce market access if firms cannot comply, but they simultaneously provide incentives for technological upgrading, greater domestic value added (DVA), and competitiveness rooted in sustainable development. Therefore, this study argues that linking climate finance and ESG with an integrated growth model is the pathway for Vietnam to transform the pressures of international integration into endogenous drivers for long-term development.

Three Intermediate Pillars in the Green Transition

To seize opportunities and overcome challenges from the international context, Vietnam needs to build on three intermediate pillars: climate finance, institutional and interoperable data, and geo-economic positioning with domestic resources. These are the foundations that ensure the green transition is implemented in a coherent and effective manner.

First, climate finance. This is the key resource enabling Vietnam to fulfill its emission reduction commitments and develop renewable energy. In practice, Vietnam has become one of the priority recipients of international support, exemplified by the JETP with a total commitment of USD 15.5 billion through 2030. In addition, the domestic banking system has launched green credit packages, accounting for about 5% of total outstanding loans, while some major corporations have issued green bonds to finance clean energy projects. However, most small and medium-sized enterprises (SMEs)—which account for over 90% of all firms—still cannot access these funds due to limited capacity to meet ESG standards and data transparency requirements. This shows that while climate finance presents major opportunities, Vietnam must improve its capacity to absorb and allocate these resources to transform them into endogenous drivers.

Furthermore, empirical data reveal that climate finance in Vietnam has started to take shape but remains limited in scale. The share of green credit in total outstanding loans rose from 0.73% in 2015 to 4.5% in 2023, and stood at about 4.3% by March 2025, equivalent to roughly VND 704 trillion in green credit. In the capital market, the cumulative issuance of green, social, and sustainable (GSS) bonds in 2016–2024 reached about VND 33.5 trillion, with VND 6.9 trillion in 2024 alone—only 1.5% of total corporate bond issuance. Meanwhile, ESG readiness among Vietnamese firms remains low: according to PwC (2022), only about 16% of firms consider social indicators a priority, while ESG reporting frameworks and data transparency remain underdeveloped. These figures are illustrated in the figure below, which presents an overview of Vietnam’s scale and readiness in building the three intermediate pillars— climate finance, the green capital market, and ESG—serving as prerequisites for leveraging international climate finance.

Figure 3: Share of Green Credit in Total Outstanding Loans, 2015–2024. Source: State Bank of Vietnam (2025)

Second, institutions and interoperable data. According to North (1991), institutions are the key factor determining the efficiency of resource allocation. In the case of Vietnam, fragmented management among ministries (Natural Resources and Environment, Industry and Trade, Finance, Planning and Investment) has created “bottlenecks” in implementing climate and energy policies. At present, the legal framework for the carbon market is still in its drafting stage, the MRV system remains fragmented, and there is no unified coordination mechanism. Huỳnh Thanh Äiá»n (2025) emphasizes the need to place coordinating institutions and interoperable data standards at the center, treating them as the foundation for allocating capital based on outcomes (TFP, DVA, market access) rather than inputs. Thus, institutional reform and the establishment of a transparent data system are the “leverage points” for Vietnam to strengthen its capacity to absorb and utilize climate finance.

Third, geo-economic positioning and domestic resources. Vietnam enjoys several strategic advantages: a central location in the Asia–Pacific region, a gateway to ASEAN and major economies, a wide network of FTAs, and a young and cost-competitive workforce. These constitute an important foundation for deeper integration into global green value chains. However, significant constraints remain: weak energy infrastructure, an electricity grid not yet capable of integrating large-scale renewable sources, high logistics costs and poor connectivity, and limited domestic research and development (R&D) capacity, leading to dependence on imported technology. Therefore, leveraging geo-economic advantages must be linked with upgrading domestic capabilities, particularly in energy, logistics, and technology.

Direct Factors Influencing the Green Transition

Vietnam’s green transition is directly influenced by three key factors: ESG, technology, and human resources. These are the specific channels through which climate finance and institutional coordination are transformed into endogenous drivers of growth.

First, ESG. Many Vietnamese enterprises have begun to recognize the importance of ESG, yet the gap between commitment and practice remains significant. The Vietnam ESG Readiness 2022 report indicates that nearly 80% of enterprises have made or are planning ESG commitments, but most face challenges due to limited knowledge, insufficient data, and a lack of clear regulatory guidance [8]. A quantitative study by on 169 enterprises further shows that ESG reporting readiness is positively associated with factors such as accounting proficiency, information technology systems, and the proportion of women in management [9]. This indicates that ESG is not merely an external requirement but is closely tied to internal governance capacity and corporate culture.

Second, technology. According to endogenous growth theory, technological innovation is the direct driver of improvements in total factor productivity (TFP). In Vietnam, the share of R&D expenditure in GDP remains low, at only about 0.43% in 2021 (World Bank, 2022), compared with over 2% in many advanced economies [1]. However, some large firms have made stronger efforts. For instance, CADIVI under the GELEX Group has committed around 2% of its revenue to R&D for developing green products in the electrical equipment sector. Such examples show an increasing trend of investment in green technology at the corporate level, although the economy as a whole still lacks breakthroughs.

Third, human resources. Human capital determines the capacity to absorb and implement ESG as well as low-carbon technologies. While Vietnam’s labor force is abundant, skills related to ESG, data governance, and innovation remain limited. PwC (2022) emphasizes that insufficient training and weak strategic leadership capacity are two major barriers hindering enterprises in implementing ESG. Therefore, enhancing green skills, digital skills, and governance capacity should be considered strategic priorities to fully leverage climate finance and opportunities from green integration.

|

Factor |

Impact on TFP |

Impact on DVA |

Impact on International Markets |

|

ESG |

Improves governance, enhances data transparency, encourages investment in innovation |

Promotes supply chain transparency, increases localization ratio |

Meets ESG/CBAM standards, maintains access to EU–US markets |

|

Technology |

Low-carbon innovation, automation, and digitalization of production |

Enables participation in higher-value segments (R&D, design) |

Meets high-tech requirements in exports |

|

Human resources |

Enhances management skills and technology absorption capacity |

Improves labor quality, raises domestic value added |

Meets demand for high-quality labor from international partners |

Table 1: Impacts of ESG, Technology, and Human Resources on TFP – DVA – International Markets

In summary, ESG, technology, and human resources represent both pressures and opportunities for the green transition. ESG shapes the international “rules of the game” and opens pathways to green finance; technology determines productivity and emission reduction capacity; while human resources are the condition for operating and absorbing innovation. The combination of these three factors will determine the extent of Vietnam’s success in building an integrated, multi-objective growth model aimed at enhancing TFP, increasing DVA, and expanding international market access.

<img src="https://www.opastpublishers.com/scholarly-images/10448-69d0d7afe277f-the-role-of-green-finance-in-vietnams-integrated-economic-de.png" width="500" height="300">

Figure 4: Impacts of ESG, Technology, and Human Resources on TFP – DVA – Market Access (Source: Author’s synthesis.)

Prospects of a Multi-Objective Integrated Growth Model

Synthesizing analyses of the international context, the three intermediate pillars, and the direct factors shows that Vietnam now stands at a historic opportunity to build a multi-objective integrated growth model. The core of this model is to treat climate finance and ESG not merely as external compliance requirements, but as endogenous drivers of development.

First, enhancing total factor productivity (TFP). Combining climate finance with technological innovation and improved ESG governance creates a momentum for productivity growth. Capital from JETP, green credit, and green bonds, if allocated based on outcomes (MRV, ESG) rather than inputs will encourage firms to invest in low-carbon technologies and transparent governance. Productivity improvements will thus derive not only from capital accumulation, but also from innovation quality and organizational efficiency.

Second, increasing domestic value added (DVA). ESG and the carbon market compel firms to make supply chains more transparent, thereby promoting localization in higher-value segments such as design, R&D, and logistics. If well-leveraged, Vietnam could reduce reliance on low-cost assembly and raise the DVA share in exports from the current 40% to 55–60% by 2030, on par with regional peers such as Thailand and China. This would mark a shift from an “assembly economy” to a “green value economy”.

Third, expanding international market access. By complying with CBAM, ESG, and MRV standards, Vietnamese enterprises will not only maintain market share in traditional destinations such as the EU, US, and Japan, but also move into higher-value segments. Participation in international carbon markets will additionally enable firms to generate revenue from carbon credit trading, thus enhancing global competitiveness.

However, these prospects can only be realized if Vietnam addresses several prerequisites: (i) building a unified coordinating institution to avoid fragmented management; (ii) establishing an interoperable MRV system aligned with international standards; (iii) creating mechanisms to support SMEs’ participation in green finance and carbon markets; and (iv) developing a workforce with ESG and green technology competencies.

If these conditions are met, the multi-objective integrated growth model will allow Vietnam to simultaneously achieve its net-zero commitment by 2050 and its ambition to become a high-income industrialized nation by mid-21st century. In other words, Vietnam can transform “green barriers” into a strategic springboard, making international integration a key driver of sustainable development.

|

Pillar / Factor |

Impact on TFP |

Impact on DVA |

Impact on Market Access |

|

Climate finance |

Promotes green technology innovation, improves productivity |

Encourages localization of green production |

Expands exports through green capital and JETP |

|

Institutions & data |

Reduces transaction costs, ensures efficient capital allocation |

Facilitates domestic firms’ participation in value chains |

Meets international MRV/CBAM standards |

|

Geo-economic position |

Strengthens infrastructure, supports supply chains |

Enhances logistics and market advantages |

Increases FDI attractiveness & regional connectivity |

|

ESG |

Encourages improved governance & transparency |

Boosts compliance with value chain standards |

Meets EU, US, Japan standards; accesses higher-value segments |

|

Technology |

Drives low-carbon innovation, digitalizes production |

Enables participation in higher-value segments (GVC) |

Meets technological requirements in exports |

|

Human resources |

Enhances skills, data governance, and technology absorption |

Expands creativity and quality management capacity |

Meets demand for high-quality labor from international partners |

|

Source: Author’s synthesis |

|||

Table 2. Matrix of Impacts of Pillars/Factors on Outcomes

The “Pillar–Factor–Outcome Impact Matrix” highlights the close linkages between intermediate pillars (climate finance, institutions–data, geo-economic position) and direct factors (ESG, technology, human resources) with the three core objectives: TFP, DVA, and international market access. What stands out is the integrated and synergistic effect: climate finance drives technological innovation, transparent institutions ensure effective capital allocation, while ESG, technology, and human resources directly enhance value and sustain exports. The table thus demonstrates that only by synchronizing all these elements can Vietnam build a multi-objective integrated growth model, transforming green–digital pressures into endogenous drivers of development

Conclusion and Policy Implications

Conclusion

This study demonstrates that in the context of green–digital integration, Climate Finance (CF) and Environmental, Social, and Governance (ESG) are not merely external compliance pressures, but can become endogenous drivers of Vietnam’s sustainable development. Through theoretical and empirical analysis, the study highlights three critical layers of the green transition: (i) the international context shaped by de-risking, CBAM, MRV, and green capital flows; (ii) three intermediate pillars—climate finance, institutions and interoperable data, and geo-economic positioning; and (iii) three direct factors—ESG, technology, and human resources. The convergence of these elements opens the prospect of building a multi-objective integrated growth model aimed at enhancing Total Factor Productivity (TFP), increasing Domestic Value Added (DVA), and expanding international market access. However, to realize this prospect, Vietnam must address core constraints such as institutional fragmentation, lack of data transparency, limited capacity to absorb climate finance,low R&D investment, and insufficient human resource quality to meet ESG and green technology requirements.

Policy Implications

Based on these findings, the study proposes five groups of policy implications for the 2025–2030 period: First, establish a national coordination mechanism for ESG and climate finance. An inter-ministerial body under the Government should be created with the authority to integrate energy, environmental, trade, and financial policies. This agency would oversee JETP implementation, monitor ESG compliance, and allocate climate finance based on outcomes such as TFP, DVA, and market access.

Second, develop an internationally standardized MRV data system. Vietnam needs a national database on emissions and supply chains to ensure transparency and interoperability with global mechanisms such as CBAM. This would help exporters meet foreign requirements while laying the groundwork for a domestic carbon market.

Third, design and operate a national carbon market. Vietnam should finalize the legal framework for carbon credit trading, ensuring clear property rights and offsetting mechanisms. A pilot carbon exchange could be launched in 2025–2026, with the aim of linking to international mechanisms under the Paris Agreement (Article 6) by 2028–2030. This would provide a vital economic tool to reduce emissions and mobilize additional finance for businesses.

Fourth, promote technological innovation and green human resource development. R&D spending should rise to at least 1% of GDP by 2030, focusing on renewable energy, clean production, and supply chain digitalization. In parallel, vocational and higher education curricula must integrate green skills, ESG, and data governance to build a high-quality workforce capable of managing the green transition.

Finally, expand domestic green finance channels. Beyond international capital, Vietnam should develop green bond markets, ESG investment funds, and green credit mechanisms to boost local firms’ participation. Special support packages should also be introduced for SMEs to lower compliance costs and strengthen their capacity to absorb climate finance.

These policy implications aim to transform international integration into a strategic lever for Vietnam’s transition from a low-cost growth model to an integrated, green, and digital growth model, simultaneously achieving three objectives: enhancing productivity (TFP), increasing domestic value added (DVA), and strengthening international market access. This is the pathway for Vietnam to escape the middle-income trap and realize its ambition of becoming a high-income industrialized country by mid-21st century

Limitations and Future Research Directions

This study has several limitations. First, the data rely primarily on secondary sources, which may not fully reflect the realities of climate finance absorption and ESG implementation in Vietnam. Second, the analysis is limited to theoretical frameworks and policy suggestions without quantitative validation. Third, the research scope focuses on the macro level and does not delve into sectoral or firm-level differences.

Future research should be expanded in three directions: (i) conduct quantitative surveys to test the impacts of climate finance and ESG on TFP, DVA, and market access; (ii) perform sectoral analyses to identify varying levels of readiness for the green transition; (iii) investigate mechanisms for linking Vietnam’s carbon market with international markets, while also examining issues of social equity in the green transition.

References

- Romer, P. M. (1990). Endogenous technologicalchange. Journal of political Economy, 98(5, Part 2), S71-S102.

- Douglass, C. (1991). Douglass C. North. The Journal of Economic Perspectives, 5(1), 97-112.

- Gereffi, G., & Fernandez-Stark, K. (2011). Global value chain analysis: a primer. Center on Globalization, Governance & Competitiveness (CGGC), Duke University, North Carolina, USA, 33.

- Trade, U. N. (2024). World Investment Report 2024: Investment Facilitation and Digital Government. United Nations.

- Biedenkopf, K., Chen, Z., De Clara, S., Doda, B., Eden, A., Hall, M., ... & Wildgrube, T. (2024). Emissions Trading Worldwide: Status Report 2024.

- Otto, S. (2025). The external impact of EU climate policy: political responses to the EU’s carbon border adjustment mechanism. International Environmental Agreements: Politics, Law and Economics, 1-18.

- Äiá»n, H. T. (2025). The Role of Green Finance in Vietnam's Integrated Economic Development Model. Available at SSRN 5768142.

- PwC Vietnam. (2022). Vietnam ESG Readiness Report 2022. PwC Vietnam.

- Nguyen, D. T. P., Nguyen, L. T. H., Nguyen, A. T. M., & Phan, L. L. T. (2024). Factors affecting the readiness for ESG reporting in Vietnamese enterprises. Problems and Perspectives in Management, 22(3), 263.