International Journal of Criminology and Criminal Law(IJCCL)

ISSN: 2996-3397 | DOI: 10.33140/IJCCL

Review Article - (2026) Volume 4, Issue 2

The Role of AI in Enhancing ESG Performance and Firm Resilience: Evidence from Vietnam’s Export-Oriented Enterprises

Received Date: Apr 01, 2026 / Accepted Date: May 01, 2026 / Published Date: May 06, 2026

Copyright: ©2026 Huynh Thanh Dien. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Dien, H. T. (2026). The Role of AI in Enhancing ESG Performance and Firm Resilience: Evidence from Vietnam

Abstract

The paper examines how artificial intelligence (AI) adoption shapes firms’ resilience (RES) through risk management (RM), data transparency (DT), and environmental, social, and governance (ESG) performance in an emerging-market context. Using a stratified sample of 300 export-oriented firms across textiles/footwear, electronics/components, seafood/ agriculture, wood/furniture, and other sectors, we estimate a structural model and conduct multi-group comparisons by ownership (FDI vs. domestic) and industry. Results indicate that AI does not directly enhance RES; instead, AI improves RM and DT, which strengthen ESG and, in turn, bolster RES. ESG exhibits the strongest total effect on RES. Heterogeneity analyses reveal pronounced gaps in AI and ESG between FDI and domestic firms and between electronics and traditional sectors, while RES tends to converge. Robustness checks address common method bias, measurement invariance, and endogeneity concerns. The findings highlight that aligning digital technologies with governance and risk capabilities is pivotal for sustainable resilience in emerging markets.

Keywords

Artificial Intelligence, ESG Practices, Organizational Resilience, Risk Management, Data Transparency, Vietnam, Emerg¬ing Markets.

Introduction

Globalization and digital transformation intensify firms' exposure to economic crises, climate risks, supply chain disruptions, and trade policy shifts. In this context, firm resilience (RES), defined as the capacity to sustain operations, adapt, and recover from shocks –has become increasingly vital [1]. Recent studies confirm that RES is a vital determinant of long-term sustainability and competitiveness, particularly in emerging economies [2].

At the same time, Environmental–Social–Governance (ESG) practices have become central to modern corporate governance. ESG enhances long-term performance by strengthening reputation, building stakeholder trust, and improving access to capital, especially during periods of crisis; [3,4]. Artificial Intelligence (AI) is increasingly recognized as a transformative capability in this regard. AI enables big-data analytics, risk detection, demand forecasting, and supply chain optimization, while also supporting the collection and standardization of ESG information to improve reporting quality [5,6]. Emerging evidence suggests that AI adoption strengthens ESG practices and, indirectly, contributes to resilience [7]. However, the mechanisms through which AI supports RES—particularly through risk management (RM) and data transparency (DT)—remain underexplored in emerging markets.

Vietnam provides a relevant context for addressing this gap. As an export-oriented economy, the country depends heavily on industries such as textiles, electronics, seafood, and wood processing, all of which face increasingly stringent ESG requirements in international markets. Understanding how AI adoption interacts with ESG practices to strengthen resilience is therefore both theoretically significant and practically urgent.

The research focuses on the relationships among AI adoption, ESG, and RES in Vietnam, highlighting the mediating roles of RM and DT. It also examines differences between foreign direct investment (FDI) and domestic firms, offering insights for both policymakers and managers.

Theoretical Framework and Analytical Model

AI Adoption and Corporate Governance

Artificial Intelligence (AI) has increasingly been recognized as a foundational tool in modern corporate governance. AI has been widely applied in areas ranging from data analytics, market demand forecasting, and supply chain management to supporting strategic decision-making. Recent studies show that AI offers specific benefits: enabling firms to identify and mitigate risks, automate processes, and improve the accuracy of ESG reporting, while simultaneously optimizing resource use to reduce costs and emissions [5,6].These findings suggest that AI does not directly generate firm resilience (RES), but serves as a fundamental capability that helps firms operate more transparently, efficiently, and sustainably.

From a sustainable governance perspective, an increasing body of empirical evidence highlights the positive relationship between AI and ESG performance. Zhang (2024) found that the level of AI adoption significantly influenced the ESG scores of Chinese firms, particularly in governance and information transparency. Similarly, emphasized the role of AI in automating ESG reporting and supporting audits of non-financial data, thereby enhancing the reliability of ESG disclosure [7].

In relation to RES, AI is regarded as a critical tool that enables firms to identify risks early and respond promptly through real-time data analytics. In supply chain management, demonstrated that AI adoption enhances RES by improving transparency, forecasting disruptions, and strengthening recovery capacity [8]. These findings align with the view that AI enhances firms' ability to process information and make effective decisions in volatile environments. However, AI should not be considered a direct driver of RES; rather, it functions as a complementary capability. AI can enhance ESG practices and resilience only when embedded in risk management systems and data transparency mechanisms .The present study contributes [9].

Beyond international evidence, studies in Vietnam and Southeast Asia also highlight the strong link between digital capabilities, ESG, and sustainable competitiveness. Nguyen & Mai (2024) showed that factors such as information technology infrastructure, management processes, and accounting capacity significantly affect the readiness of manufacturing firms in Vietnam to adopt ESG reporting [10]. A broader research review further affirms that technological capacity is a prerequisite for ESG adoption in Asian firms (Hermawan, Wijaya, & Rianawati, 2025). These findings reinforce the assumption that AI, as a manifestation of advanced technological capability, can help firms overcome information barriers to implement ESG more effectively.

ESG and Its Role in Firm Resilience (RES)

ESG is increasingly recognized as a managerial standard that reinforces organizational robustness. Firms prioritizing ESG exhibit greater capital-allocation efficiency and reduced vulnerability to shocks; ESG also strengthens resilience through more effective risk management and enhanced investor/customer trust [4,11].

ESG is tightly linked to supply-chain strength: firms with stronger ESG tend to maintain more resilient supply chains and long-term growth. AI catalyzes these outcomes by improving information governance and transparency (Li, Chen, & Wang, 2024) [7]. In export-dependent Vietnam, which faces ESG requirements from the EU, the US, and Japan, credible ESG has become a necessary condition for competitiveness and long-term resilience.

The Mediating Role of Risk Management and Data Transparency

AI influences RES through two mediators: risk management (RM) and data transparency (DT). First, RM: AI enables firms to forecast market fluctuations, assess climate impacts, and design crisis-response scenarios, reducing losses and safeguarding continuity [12,13]. Second, DT: AI supports ESG data collection, processing, and standardization (e.g., GRI, ISSB), improving the transparency and reliability of disclosure and strengthening stakeholder trust [6,5]. Together, RM and DT are the bridge through which AI translates into ESG capabilities and, via ESG, into resilience [14,15].

Firm Resilience (RES)

RES denotes a firm's capacity to adapt, sustain operations, and recover swiftly after crises. Determinants include supply flexibility, input diversification, contingency planning, digital transformation, and green innovation; [2,5]. In ASEAN, stronger financial foundations and governance practices supported performance during dual crises, while higher ESG scores correlated with lower earnings volatility [16,17]. In Vietnam, softer factors such as cost flexibility, market diversification, and social networks also play an important role alongside technology and ESG.

Conceptual Framework and Research Hypotheses

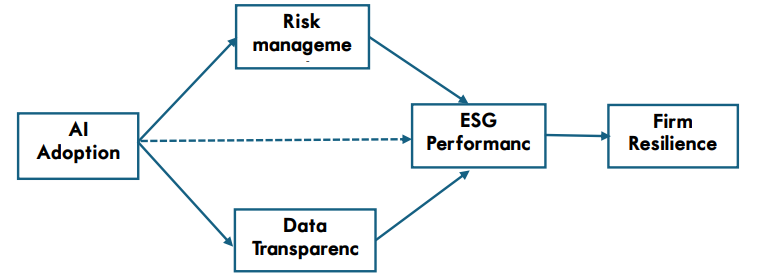

In the context of global volatility, digital technology adoption and ESG practices are increasingly regarded as critical pillars for enhancing firm resilience (RES). Artificial Intelligence (AI) has emerged as a foundational tool that not only supports risk management and strengthens data transparency but also contributes to improving ESG performance and organizational resilience. Building on the theoretical synthesis and prior empirical studies, this paper proposes a conceptual framework that illustrates the relationships among AI adoption, risk management, data transparency, ESG, and RES (Figure 1).

Figure 1: Conceptual framework of the relationships among AI, risk management, data transparency, ESG, and RES

Source: Compiled and proposed by the author based on prior studies

AI enables firms to forecast market fluctuations, detect anomalies, and develop crisis response scenarios, thereby improving the effectiveness of risk management. Demonstrated that digital transformation and data technologies enhance the risk management capacity of small and medium-sized enterprises, particularly under conditions of uncertainty [18]. Hence, the following hypothesis is proposed. H1: AI adoption positively influences risk management.

AI supports the processing, standardization, and disclosure of ESG data, improving the reliability and transparency of reporting. Chen, Evans, and Zhang (2024) showed that the degree of digital technology adoption, including AI, is closely associated with the quality of firms' ESG disclosure. This leads to the hypothesis. H2: AI adoption positively influences data transparency.

An effective risk management system helps firms minimize losses, allocate resources efficiently, and better meet ESG requirements. Found that during the financial crisis, companies with stronger risk management maintained higher ESG performance [3]. Therefore. H3: Risk management positively influences ESG performance.

Transparency in ESG disclosure reduces information asymmetry, enhances investor trust, and strengthens market reputation. Found that using AI to enhance ESG disclosure helps firms reinforce organizational legitimacy and stakeholder relations. Thus, the hypothesis is [6]. H4: Data transparency positively influences ESG performance.

AI not only improves risk management and data transparency but also directly enhances ESG performance by automating reporting and optimizing resource utilization. Both Chen et al. (2024) and provided evidence that AI adoption positively affects ESG quality. Therefore [6]. H5: AI adoption positively influences ESG performance.

Firms with higher ESG performance typically demonstrate stronger capital allocation and sustainable governance, which enhance their resilience against shocks. Wang et al. (2023) showed that ESG optimizes capital efficiency and strengthens firm resilience, while also provided evidence that ESG promotes resilience and business performance [19]. Accordingly. H6: ESG performance positively influences firm resilience.

Combining H5 and H6, it can be inferred that AI indirectly contributes to firm resilience by enhancing ESG performance. Confirmed that AI-driven ESG improvements have spillover effects on sustainable development and organizational resilience [7]. Therefore. H7: AI adoption indirectly influences firm resilience through ESG.

Research Methodology

We employ a quantitative research design, using a structured questionnaire administered to 300 export-oriented firms spanning textiles/footwear, electronics/components, seafood/agriculture, wood/furniture, and other industries. The sample was stratified by ownership type (FDI vs. domestic) and firm size, enabling robust comparative analysis. A total of 300 observations meets the recommended threshold for structural equation modeling (SEM); suggest a minimum of 200 cases to ensure reliable estimation in complex SEM models [20]. The present study therefore provides sufficient statistical power for hypothesis testing.

Measurement scales were adapted from validated instruments in prior research (Kim & Park, 2022; Liu et al., 2023; Zhang & Li, 2024) and contextualized for Vietnam (see Table 1). Reliability was examined using Cronbach's ![]() (> 0.70) and composite reliability, while validity was assessed through exploratory factor analysis (KMO > 0.70; Bartlett's test p < 0.05) and confirmatory factor analysis (CFI/TLI > 0.90; RMSEA, SRMR < 0.08) following [20, 21, 22]. Convergent and discriminant validity were further confirmed using average variance extracted (AVE), the Fornell—Larcker criterion, and the HTMT ratio (Fornell & Larcker, 1981).

(> 0.70) and composite reliability, while validity was assessed through exploratory factor analysis (KMO > 0.70; Bartlett's test p < 0.05) and confirmatory factor analysis (CFI/TLI > 0.90; RMSEA, SRMR < 0.08) following [20, 21, 22]. Convergent and discriminant validity were further confirmed using average variance extracted (AVE), the Fornell—Larcker criterion, and the HTMT ratio (Fornell & Larcker, 1981).

The structural model was estimated with SEM, supplemented by multi-group analysis to compare FDI and domestic firms across industries [23]. To address potential common method bias, we employed both procedural remedies and ex-post diagnostics, including Harman's single-factor test, marker-variable analysis, and full collinearity variance inflation factor (VIF). Measurement invariance tests (configural, metric, and scalar) supported valid cross-group comparisons. Robustness was further ensured by bootstrapping with 5,000 resamples, providing bias-corrected confidence intervals for direct and indirect effects as well as effect size estimates.

|

Construct |

Code |

No. of Items |

Key Measurement Content |

Reference |

|

AI Adoption |

AI1–AI4 |

4 |

Extent of AI adoption in data analytics, ESG monitoring, risk forecasting, and sustainable planning |

Kim & Park (2022) |

|

Risk Management |

RM1–RM4 |

4 |

Role of AI in early warning, risk identification, crisis scenario building, and loss mitigation |

Liu et al. (2023) |

|

Data Transparency |

DT1–DT4 |

4 |

AI’s ability to improve accuracy, transparency, and standardization of ESG data, enhancing investor trust |

Liu et al. (2023) |

|

ESG Performance |

ESG1–ESG4 |

4 |

ESG implementation: emission reduction, social responsibility, governance transparency, and strategic integration |

Zhang & Li (2024) |

|

Firm Resilience (RES) |

RES1–RES4 |

4 |

Ability to recover after crises, sustain operations, adapt to disruptions, and leverage growth opportunities |

Zhang & Li (2024) |

|

Source: Author, adapted from prior studies. |

||||

Table 1: Summary of Research Measurement Scales

Research Results

Descriptive Statistics of the Sample

The survey data of 300 enterprises reflects a fairly representative distribution of industries and firm types within Vietnam's export sector. Among the total sample, domestic enterprises accounted for 57.3%, while foreign direct investment (FDI) enterprises represented 42.7%. By industry, textiles and footwear accounted for the largest share of firms (31.7%), followed by electronics and components (23.3%), seafood and agriculture (19.7%), wood and furniture (15.7%), and other sectors (9.6%) (See Table 2). This structure is consistent with the actual composition of Vietnam's key export industries and allows for reliable comparisons across sectors as well as between FDI and domestic firms.

|

Industry |

FDI |

Domestic |

Total |

|

Textiles/Footwear |

46 |

49 |

95 |

|

Electronics/Components |

28 |

42 |

70 |

|

Seafood/Agriculture |

26 |

33 |

59 |

|

Wood/Furniture |

19 |

28 |

47 |

|

Others |

9 |

20 |

29 |

|

Total |

128 |

172 |

300 |

|

Source: Author’s calculation, 2025. |

|||

Table 2: Distribution of Enterprises by Industry and Firm Type

Reliability and Validity of Measurement Scales

The reliability test results show that all measurement scales achieved Cronbach's Alpha values ranging from 0.842 to 0.892, exceeding the recommended threshold of 0.70 [21]. This indicates a high level of internal consistency among observed variables, ensuring the reliability of each construct. In addition, Composite Reliability (CR) values were all greater than 0.70, further confirming the stability and reliability of the measurement scales in the research model (Table 3).

|

Construct |

No. of Items |

Cronbach’s Alpha |

|

AI Adoption |

4 |

0.870 |

|

Risk Management |

4 |

0.842 |

|

Data Transparency |

4 |

0.857 |

|

ESG Performance |

4 |

0.880 |

|

Firm Resilience |

4 |

0.892 |

|

Source: Author’s calculation, 2025. |

||

Table 3: Cronbach’s Alpha and Reliability Test Results

Next, an Exploratory Factor Analysis (EFA) was conducted to examine the convergent and discriminant validity of the constructs. Results indicated a Kaiser–Meyer–Olkin (KMO) value of 0.912 and a statistically significant Bartlett's Test of Sphericity (p < 0.001), confirming the suitability of the dataset for factor analysis. Five factors were extracted, explaining a total variance of 71.4%, which is above the conventional 50% threshold, suggesting that the measurement scales adequately represent the underlying constructs (Table 4).

|

Indicator |

Value |

Standard |

Conclusion |

|

KMO |

0.912 |

> 0.60 |

Acceptable |

|

Bartlett’s Test (p) |

<0.001 |

<0.05 |

Significant |

|

No. of Extracted Factors |

5 |

≥ 1 |

Acceptable |

|

Explained Variance |

71.4% |

≥ 50% |

Acceptable |

|

Source: Author’s calculation, 2025. |

|||

Table 4: Exploratory Factor Analysis (EFA) Results

In Confirmatory Factor Analysis (CFA), the model fit indices indicated a good fit (CFI = 0.94; TLI = 0.93; RMSEA = 0.045; SRMR = 0.046). The standardized factor loadings of observed variables ranged from 0.72 to 0.84, satisfying the requirement for convergent validity. Moreover, the Average Variance Extracted (AVE) values were all above 0.50, and the Heterotrait–Monotrait (HTMT) ratios were below 0.85 across constructs, confirming both convergent and discriminant validity of the scales (Table 5).

|

Indicator |

Value |

Acceptable Threshold |

|

CFI |

0.94 |

> 0.90 |

|

TLI |

0.93 |

> 0.90 |

|

RMSEA |

0.045 |

< 0.08 |

|

SRMR |

0.046 |

< 0.08 |

|

Factor Loadings |

0.72 – 0.84 |

≥ 0.50 |

|

CR |

≥ 0.70 |

≥ 0.70 |

|

AVE |

≥ 0.50 |

≥ 0.50 |

|

HTMT |

< 0.85 |

< 0.85 |

|

Source: Author’s calculation, 2025. |

||

Table 5: Confirmatory Factor Analysis (CFA) Results

Thus, all measurement scales in the study satisfy the requirements of reliability, convergent validity, and discriminant validity, providing a robust foundation for subsequent Structural Equation Modeling (SEM) analysis.

Structural Equation Modeling (SEM) Results

The SEM analysis results indicate that the proposed research model demonstrates a high degree of fit with the survey data. The model fit indices (CFI = 0.94, TLI = 0.93, RMSEA = 0.045, and SRMR = 0.046) meet or exceed the thresholds recommended by Hu and Bentler (see Table 6) [22]. This confirms that the proposed theoretical framework is appropriate for testing the relationships among AI, risk management, data transparency, ESG, and firm resilience (RES).

|

Path |

Standardized β |

p-value |

Conclusion |

|

RM ← AI |

0.62 |

<0.001 |

Significant, supports H1 |

|

DT ← AI |

0.58 |

<0.001 |

Significant, supports H2 |

|

ESG ← RM |

0.44 |

<0.001 |

Significant, supports H3 |

|

ESG ← DT |

0.37 |

0.004 |

Significant, supports H4 |

|

ESG ← AI |

0.19 |

0.031 |

Significant but weak, supports H5 |

|

Source: Author’s calculation, 2025. |

|||

Table 6: SEM Estimation Results

The path analysis shows that AI adoption strongly influences risk management and data transparency, which in turn indirectly enhance ESG performance. ESG emerges as the central construct, exerting the strongest effect on RES. AI adoption does not directly increase resilience; rather, its influence is primarily mediated through ESG. The model explains 58% of the variance in ESG and 50% of the variance in RES, indicating a relatively good explanatory power.

In summary, the SEM results not only confirm the mediating roles of risk management and data transparency but also emphasize the critical importance of ESG as the key linkage connecting AI with firm resilience. The policy implication is clear: firms should not only invest in AI but must also simultaneously strengthen risk management, improve data transparency, and integrate ESG into their development strategies to achieve sustainable resilience.

Comparison of Results by Industry and Firm Type

The analysis reveals notable cross-industry differences in Artificial Intelligence (AI) adoption, ESG practices, and firm resilience (RES). The electronics and components sector recorded the highest average level of AI adoption (3.98), alongside relatively high values for ESG (3.71) and RES (3.55), reflecting its technology-intensive nature and deep international integration, largely driven by foreign direct investment (FDI) firms. In contrast, the "Other" industries group reported the lowest values across all three dimensions (AI = 3.34; ESG = 3.51; RES = 3.34), highlighting constraints in resources and governance standardization. The seafood and agriculture sector achieved a relatively high ESG score (3.65), consistent with stringent international requirements for safety and sustainability, although its AI adoption and RES levels remained moderate. The textiles and footwear, as well as wood and furniture industries, showed relatively balanced outcomes, with indices fluctuating around moderately high averages (Table 7).

|

Industry |

AI_mean |

ESG_mean |

RES_mean |

|

Textiles/Footwear |

3.65 |

3.61 |

3.55 |

|

Others |

3.34 |

3.51 |

3.34 |

|

Seafood/Agriculture |

3.47 |

3.65 |

3.43 |

|

Electronics/Components |

3.98 |

3.71 |

3.55 |

|

Wood/Furniture |

3.60 |

3.39 |

3.42 |

|

Source: Author’s calculation, 2025. |

|||

Table 7. Average AI, ESG, and RES Values by Industry

By ownership type, pronounced differences exist between FDI and domestic enterprises. FDI firms reported higher average levels of AI adoption (3.87) and ESG practices (3.73) compared to domestic firms (AI = 3.49; ESG = 3.49), reflecting their advantages in capital, technology, and compliance with international standards. However, in terms of RES, the gap between the two groups was relatively modest (FDI = 3.66; Domestic = 3.36). This suggests that although domestic firms lag behind in technology adoption and ESG governance, they retain a certain degree of adaptability in coping with global economic turbulence (Table 8).

|

Firm Type |

AI_mean |

ESG_mean |

RES_mean |

|

FDI |

3.87 |

3.73 |

3.66 |

|

Domestic |

3.49 |

3.49 |

3.36 |

|

Source: Author’s calculation, 2025. |

|||

Table 8: Average AI, ESG, and RES Values by Firm Type

Overall, the comparison across industries and ownership types shows two key patterns: (i) AI adoption and ESG practices are clearly differentiated, being concentrated in the electronics and components sector as well as among FDI firms; and (ii) RES does not differ significantly across groups, reflecting the broad adaptive capacity of Vietnamese enterprises. These findings carry important policy implications, underscoring the need to promote mechanisms for technology transfer and ESG standardization from FDI to domestic firms, while simultaneously supporting traditional industries such as textiles, agriculture, and wood processing in strengthening technological capabilities and governance to achieve sustainable resilience.

Discussion

The results indicate that all measurement scales satisfied the thresholds for reliability and validity (Cronbach's Alpha, CR, AVE, HTMT), confirming the robustness of the SEM model and its suitability for hypothesis testing.

The analysis confirms that Artificial Intelligence (AI) does not exert a significant direct effect on firm resilience (RES). Instead, the effect is indirect, operating through the mediating channels of risk management (RM) and data transparency (DT), which in turn strengthen Environmental—Social—Governance (ESG) performance. The indirect pathway in which AI influences RM and DT, which subsequently enhance ESG and ultimately strengthen RES, is statistically significant, with standardized coefficients ranging from 0.18 to 0.27 (95% CI: [0.09, 0.32]). These results highlight ESG as the central mechanism through which digital adoption enhances organizational resilience, consistent with recent international evidence (Li et al., 2025) [24].

Comparative analysis reveals clear heterogeneity across ownership and industry. Foreign direct investment (FDI) firms demonstrate significantly higher levels of AI adoption and ESG performance than domestic enterprises, while differences in RES are more modest (FDI mean = 3.66 vs. domestic mean = 3.36). Similarly, the electronics and components sector records the highest values of AI adoption and ESG, reflecting its technology-intensive nature, whereas traditional industries such as textiles and footwear show lower adoption but comparable resilience outcomes.

Overall, these findings emphasize the indirect and conditional role of AI: AI adoption enhances resilience only when embedded in RM and DT practices that elevate ESG standards. This aligns with emerging evidence from other economies, including China and Korea [7, 25]. By situating Vietnam's experience within these comparative debates, the study reinforces the argument that AI enabled governance and ESG capabilities constitute critical levers of sustainable competitiveness in emerging markets.

Policy Implications

The findings yield several important implications for strengthening the resilience (RES) of Vietnamese enterprises in the context of global integration and volatility.

First, accelerate AI technology transfer from FDI to domestic firms. FDI enterprises demonstrate significantly higher AI adoption, while domestic firms lag due to limited resources. Policies should promote technology diffusion through value-chain linkages, fiscal incentives, and innovation hubs to reduce this gap.

Second, elevate ESG as a strategic benchmark rather than mere export compliance. Given ESG's strong effect on RES, the government should issue locally tailored standards aligned with international norms and support SMEs with training, consulting, and green finance access.

Third, institutionalize risk management (RM) and data transparency (DT). As AI's impact is mediated through RM and DT, policies should mandate standardized risk systems and strengthen corporate data governance. Legal frameworks for ESG disclosure can enhance transparency and investor confidence.

Fourth, support traditional export industries in upgrading governance and technology. Textiles, wood, and agriculture remain central to Vietnam's exports but lag in AI and ESG implementation. Preferential credit schemes, innovation funds, and sector-specific training should be prioritized to reduce inter-sectoral disparities [26-38].

Conclusion

This article analyzed the interrelationships among AI adoption, RM, DT, ESG practices, and RES in Vietnamâ??s export oriented enterprises. The findings reveal that AI does not directly enhance resilience but exerts an indirect influence through RM and DT, which, in turn, strengthen ESG. ESG emerges as the most critical determinant of resilience, underscoring the role of governance and sustainability standards as strategic pillars for long-term competitiveness.

The study contributes to the literature by clarifying how AI driven capabilities translate into resilience through ESG in an emerging market context. For practice, the results suggest that enterprises should align AI investment with institutionalized RM and DT, while policymakers should support technology transfer from FDI firms to domestic enterprises and establish ESG benchmarks consistent with global standards. These measures would enable both advanced and traditional sectors to enhance resilience in the face of global uncertainty.

Several limitations should be acknowledged, including the focus on major export industries and the use of cross sectional data, which constrain the generalizability and the dynamic assessment of resilience. Future research could adopt longitudinal designs and expand to a wider spectrum of firms and sectors. Importantly, the framework can be extended beyond Vietnam to ASEAN and cross country contexts, enabling comparative analyses that capture institutional diversity, technological readiness, and ESG adoption. To operationalize this extension, scholars could harmonize ESG taxonomies, ensure measurement invariance, and employ panel or administrative data to examine policy shocks (e.g., carbon regulations, AI sandboxes). Such efforts would enhance external validity and position the study within broader debates on AI enabled sustainability and organizational resilience in emerging economies.

References

- Lee, S., & Kim, H. (2021). Corporate resilience and crisis management: Evidence from global industries. Journal of Business Research, 134, 425–437.

- Di Floristella, A. P., Jerdenius, A., Maasdorp, E., & Sahin,O. (2022). Comparative perspectives on EU and ASEAN approaches to supply chain resilience in times of crisis.Journal of Risk and Financial Management, 15(11), 481.

- Broadstock, D. C., Chan, K., Cheng, L. T., & Wang, X. (2021). The role of ESG performance during times of financial crisis: Evidence from COVID-19 in China. Finance research letters, 38, 101716.

- Wang, K., Yu, S., Mei, M., Yang, X., Peng, G., & Lv, B. (2023). ESG performance and corporate resilience: an empirical analysis based on the capital allocation efficiency perspective. Sustainability, 15(23), 16145.

- Xu, Y., Li, Z., & Chen, H. (2024). Digital transformation, green innovation, and corporate resilience: Evidence from Chinese manufacturing firms. Journal of Cleaner Production, 421, 138765.

- Alshareef, M. N. (2025). Artificial intelligence-enhanced environmental, social, and governance disclosure quality and financial performance nexus in Saudi listed companies under vision 2030. Sustainability, 17(16), 7421.

- Xiao, Y., & Xiao, L. (2025). The impact of artificial intelligence-driven ESG performance on sustainable development of central state-owned enterprises listed companies. Scientific Reports, 15(1), 8548.

- Pan, H., Zou, N., Wang, R., Ma, J., & Liu, D. (2025).Artificial intelligence usage and supply chain resilience: An organizational information processing theory perspective. Systems, 13(9), 724.

- OECD. (2025). The Adoption of Artificial Intelligence in Firms. Paris: OECD Publishing.

- Nguyen, T. T., & Kim, S. Y. (2021). ESG practices and firm resilience: Evidence from emerging markets. Asia Pacific Journal of Management, 38(4), 1153–1177.

- Zhang, H., & Liu, Q. (2025). How ESG performance promotes organizational resilience: Evidence from global manufacturing firms. Business Strategy and the Environment, 34(2), 512–528.

- Adebis, H. S., & John, B. (2025). Leveraging AI-enhanced ESG metrics for effective risk assessment in bank treasury operations.

- Kokina, J., Blanchette, S., Davenport, T. H., & Pachamanova,D. (2025). Challenges and opportunities for artificial intelligence in auditing: Evidence from the field. International Journal of Accounting Information Systems, 56, 100734.

- ESG Book. (2023, November 23). How generative AI enables corporate ESG reporting. ESG Book Research Insights.

- Klein, A., & Zhou, L. (2025). AI, ESG, and law: Potential, limitations, and strategies concerning AI in ESG reporting. SSRN.

- Rahman, M., Alam, N., & Khan, A. (2024). Dual crises resilience: Financial dynamics of ASEAN tourism firms under COVID-19 and global shocks. Tourism Economics. Advance online publication.

- Khodijah, A. S., Astuti, D. R., Muhammad, A., & Ihsan,Z. (2024, June). The Resilience of ASEAN 5 Company during Pandemics: Does ESG matter?. In Proceedings of the 8th Global Conference on Business, Management, and Entrepreneurship (GCBME 2023) (Vol. 288, p. 180). Springer Nature.

- Hokmabadi, H., Rezvani, S. M., & de Matos, C. A. (2024). Business resilience for small and medium enterprises and startups by digital transformation and the role of marketing capabilities—A systematic review. Systems, 12(6), 220.

- Kim, B., & Kim, B. G. (2023). An explorative study of resilience influence on business performance of Korean manufacturing venture enterprise. Sustainability, 15(9), 7218.

- Hair, J. F. (2009). Multivariate data analysis.

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychometric theory (3rd ed.). McGraw-Hill.

- Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural equation modeling: a multidisciplinary journal, 6(1), 1-55.

- Kline, R. B. (2016). Principles and practice of structural equation modeling (4th ed.). Guilford Press.(2026).

- Zhang, Y. (2024). Artificial intelligence adoption and ESG performance: Evidence from Chinese listed companies. Sustainability, 16(12), 8765.

- Li, J., Wu, T., Hu, B., Pan, D., & Zhou, Y. (2025). Artificial intelligence and corporate ESG performance. International Review of Financial Analysis, 102, 104036

- McAfee, A., & Brynjolfsson, E. (2017). Machine, platform, crowd: Harnessing our digital future. WW Norton & Company.

- Chen, S. (2024). The influence of artificial intelligence and digital technology on ESG reporting quality. International Journal of Global Economics and Management, 3(1), 301-310.

- Cui, J. (2025). Empirical Analysis of Digital Innovations Impact on Corporate ESG Performance: The Mediating Role of GAI Technology. arXiv preprint arXiv:2504.01041.

- Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organizational processes and performance. Management science, 60(11), 2835-2857.

- NURUL, H. R., & IMRAN, H. R. (2025). The role of data analytics in enhancing ESG transparency in the corporate sector of Bangladesh. GLOBAL JOURNAL OF ENGINEERING AND TECHNOLOGY ADVANCES УÑ?Ñ?едиÑ?ели: Global Scholarly Communication, 22(1), 081-093.

- Kline, R. B. (2023). Principles and practice of structural equation modeling. Guilford publications.

- Lee, K. (2019). The art of economic catch-up: Barriers, detours and leapfrogging in innovation systems. Cambridge University Press.

- Li, Y., Wang, M., & Zhao, L. (2022). Artificial intelligence adoption and sustainable firm performance: The mediating role of risk management. Journal of Cleaner Production, 351, 131569.

- Lin, Y., & Li, S. (2025). Supply chain resilience, ESG performance, and corporate growth. International Review of Economics & Finance, 97, 103763.

- Lu, Y., Wu, J., Peng, J., & Lu, L. (2020). The perceived impact of a public health emergency on SMEs: Evidence from China. Sustainability, 12(13), 5353.

- Tan, J. D., & Low, K. C. (2020). Corporate governance, transparency, and sustainability in Singapore. Corporate Governance, 20(1), 45–62.

- World Bank. (2020). Vietnam development report 2020: Connecting Vietnam for growth and shared prosperity. World Bank.(2026).

- Xu, J. (2024). AI in ESG for financial institutions: an industrial survey. arXiv preprint arXiv:2403.05541.