Journal of Investment, Banking and Finance(JIBF)

ISSN: 2997-2256 | DOI: 10.33140/JIBF

Impact Factor: 0.92

Research Article - (2025) Volume 3, Issue 2

Financial Materiality and Market Dynamics of ESG Performance in the Global Electronics Industry: An Empirical Analysis Amidst Diverse Regulatory and Technological Landscapes

Received Date: May 12, 2025 / Accepted Date: Jun 05, 2025 / Published Date: Jun 13, 2025

Copyright: ©2025 Henry Efe Onomakpo. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Onomakpo, H. E. O. (2025). Financial Materiality and Market Dynamics of ESG Performance in the Global Electronics Industry: An Empirical Analysis Amidst Diverse Regulatory and Technological Landscapes. J Invest Bank Finance, 3(2), 01-17.

Abstract

The global electronics industry faces escalating sustainability regulations and rapid technological change. This study quantitatively examines the financial implications of Environmental, Social, and Governance (ESG) performance for 13 multinational electronics firms from 2015 to 2025. Panel regressions, controlling for Fama-French-Momentum factors, find that sustained, long-term aggregate ESG and social (S) pillar scores are positively associated with stock excess returns. Vector Auto-regression (VAR) analysis of a constructed ESG factor (HML_ESG) reveals limited dynamic linkage with traditional market risks, indicating that ESG factors exhibit distinct risk/ return characteristics within this sector. These results are contextualized within a landscape of diverse global regulations (e.g., WEEE, RoHS, ESPR) and the growing influence of advanced technologies, including artificial intelligence and digital twins. The findings inform a "Global Regulatory-ESG Financial Salience Model," providing empirical evidence of ESG’s financial materiality. This research offers insights for firms navigating sustainability pressures and for investors evaluating performance in the evolving electronics industry, highlighting the market’s potential recognition of strategic, long-term ESG commitments.

Keywords

ESG, Electronics Industry, Financial Performance, Panel Regression, Vector Autoregression, Global Regulation, Digital Twins, Artificial Intelligence, Sustainability, Stock Returns

Abbreviations

ADF: Augmented Dickey-Fuller

AI: Artificial Intelligence

BIC: Bayesian Information Criterion

BP: Breusch-Pagan

CE: Circular Economy

CMA: Conservative Minus Aggressive (Fama-French Factor)

DPP: Digital Product Passport

DW: Durbin-Watson

ESG: Environmental, Social, and Governance

ESPR: Ecodesign for Sustainable Products Regulation

EU: European Union

FE: Fixed Effects

FEVD: Forecast Error Variance Decomposition

FF6: Fama-French Six-Factor Model (Including Momentum)

G-Score: Governance Score

HML: High Minus Low (Fama-French Factor) HML_ESG: High Minus Low ESG Factor IRF: Impulse Response Function

MKT_RF: Market Risk Premium (Fama-French Factor)

MSCI: Morgan Stanley Capital International

NRBV: Natural Resource-Based View

OLS: Ordinary Least Squares

REACH: Registration, Evaluation, Authorisation and Restriction of Chemicals

RMW: Robust Minus Weak (Fama-French Factor)

RoHS: Restriction of Hazardous Substances

RQ: Research Question

S-Score: Social Score

SMB: Small Minus Big (Fama-French Factor) TSCA: Toxic Substances Control Act (US) VAR: Vector Autoregression

WEEE: Waste Electrical and Electronic Equipment WML: Winners Minus Losers (Momentum Factor) XR: Extended Reality

Introduction

The global electronics industry is undergoing a profound transformation, driven by the dual imperatives of advancing technological innovation and meeting escalating sustainability demands [1-4]. Across the world, regulatory bodies are enacting increasingly stringent measures to address the envi-ronmental and social impacts of this sector, particularly concerning electronic waste (e-waste) man-agement, hazardous substance control, and the promotion of a circular economy (CE) [5-19]. Navigating this complex global regulatory maze while leveraging sustainable practices for competitive advantage is a critical challenge for multinational electronics corporations [20]. The "Global E waste Monitor 2020" highlights the scale of this challenge, detailing increasing quantities and flows of e-waste globally [21].

While the European Union (EU) has been a frontrunner with comprehensive frameworks such as the Ecodesign for Sustainable Products Regulation (ESPR), Waste Electrical and Electronic Equipment (WEEE) Directive, and Restriction of Hazardous Substances (RoHS) Directive, these often serve as catalysts or benchmarks for regulatory developments in other major economic zones [5,6,8-15,17,22-25]. For example, North America has federal legislation such as the Resource Conservation and Re-covery Act (RCRA) and influential state-level e-waste laws [26-28]. Asian economic leaders such as China and Japan have implemented their own RoHS-equivalent standards and robust appliance recy- cling laws [22,29,30]. Similar trends towards Extended Producer Responsibility (EPR) and specific e-waste management rules are evident in South America, Africa, and Oceania [9,10,31-33]. The OECD's "Global Material Resources Outlook to 2060" further underscores the economic drivers and environmental consequences necessitating such global regulatory attention [34].

Concurrently, the sector is being reshaped by emergent

technologies such as Artificial Intelligence (AI), Digital Twins, and Digital Product Passports (DPPs), which offer new capabilities for enhanc-ing sustainability and compliance across global value chains [3,5,6,8,35-39]. This backdrop of intense regulatory pressure and technological transformation, coupled with investor and stakeholder focus on corporate Environmental, Social, and Governance (ESG) performance, has significantly increased [4,40]. This study quantitatively investigates the financial materiality of ESG performance using a sample of globally operating multinational electronics firms. The key research questions are:

• RQ1: Is there a statistically significant association between ESG performance metrics and stock market excess returns of multinational electronics firms, after controlling for market risk factors?

• RQ2: Do the ESG factors for these global electronics firms exhibit distinct dynamic interactions with traditional market risk factors?

• RQ3: What are the financial implications of ESG performance in this sector, considering global regulatory pressures and technological enablers, thereby informing a conceptual model of "Regulatory-ESG Financial Salience"?.

This research analyzes historical stock market data, ESG scores, and financial risk factors for 13 multinational electronics firms [41-44]. Preliminary findings suggest that sustained, long-term ESG performance, particularly overall and social metrics, is positively associated with stock returns, while a constructed ESG factor appears largely independent of traditional market risks. This study aims to provide nuanced quantitative evidence within this specific global industry context, acknowledging the vision for a "New Circular Vision for Electronics" advocated by bodies like the World Economic Forum [45]. The paper is structured as follows: Section 2 examines the theoretical framework and relevant literature. Section 3 describes the data, variables, and methodology. Section 4 discusses di-agnostic tests. Section 5 presents empirical findings. Section 6 addresses these findings, provides a conceptual paradigm, and examines the worldwide implications and limitations. Section 7 concludes.

Theoretical Framework and Literature Review

This study integrates stakeholder theory, the Natural Resource- Based View (NRBV), and the Porter Hypothesis to understand the ESG-finance nexus in the global electronics industry. Stakeholder theory suggests that firms addressing diverse stakeholder interests, including ESG concerns related to environmental protection and social welfare, can build trust, enhance reputation, and potentially improve financial performance [4,46-48]. This is particularly relevant for the electronics sector, where stakeholder pressures increasingly focus on global environmental impacts such as e-waste and re-source use, as well as social issues like labor conditions in international supply chains [6,9-15,19,21,22,49,50]. The NRBV posits that unique environmental capabilities and green innovations, crucial in an industry striving for eco-design and circularity, can be sources of sustainable competitive advantage [5,7,8,16-18,22,51-55]. The Porter Hypothesis argues that well-designed environmental regulations can spur innovation that enhances competitiveness, a perspective relevant given the global proliferation of electronics sustainability regulations [20,26,54,56,57]. However, the impact of regulatory stringency can vary, with potential for negative consequences if regulations are not har-monized or effectively implemented across different jurisdictions [11,58-61]. The impact of corporate sustainability on organizational processes and performance itself is a significant area of study [62].

A complex tapestry of regulations governs sustainable electronics globally. Europe's WEEE, RoHS, and ESPR/Eco-Design directives, alongside its Circular Economy Action Plan including Digital Product Passports, are highly influential [5-12,14-18,22-25,51- 53]. North America utilizes federal acts like the US RCRA and TSCA, complemented by state-level e-waste laws and programs like En-ergy Star [26-28]. Key Asian regulations include China's RoHS and Circular Economy Promotion Law, Japan's Home Appliance Recycling Law, and India's E-Waste (Management) Rules [9,22,29-31]. Similar regulatory objectives are pursued in South America (e.g., Brazil's National Solid Waste Policy), Africa (e.g., South Africa's National Environmental Management Act), and Oceania (e.g., Australia's Product Stewardship Act) [32,33,63]. This global regulatory trend, while varied, signals a collective move towards greater producer responsibility and lifecycle management in electronics [11,20,40,59,60].

Emerging technologies are increasingly critical for the electronics industry to meet these global sus-tainability goals. Artificial Intelligence offers significant potential for optimizing resource utilization, enhancing supply chain transparency, and improving e-waste recycling processes [3,6,35,36]. Digital Twins facilitate sustainable product design, predictive maintenance, and lifecycle management, sup-porting eco-design and circular economy principles on a global scale [36-39]. Smart tags and block-chain are foundational for implementing effective Digital Product Passports, enhancing traceability and end-of-life decision-making across international supply chains [5,6,8,64]. The strategic deploy- ment of these technologies is vital for managing complexity and driving sustainable practices worldwide [1-3,35-39,65].

The financial implications of ESG performance for globally operating firms remain a central theme in sustainable finance [46- 48,54-57,66]. Numerous studies have explored this link, with results often varying by industry, region, and methodology [22,62,66]. Asset pricing models like the Fama-French framework are standard for assessing whether ESG factors explain returns beyond known risks [44,66]. Panel data methods allow for robust analysis across firms and time, while VAR models can reveal dynamic interactions between ESG and market factors [66,67]. This study applies these quan-titative tools to major global electronics players, using ESG data sourced via tools like Python’s yesg library and interpreted according to established rating methodologies [41-43].

Data, Variables and Methodology

Data

This study analyzed monthly data from March 2015 to March 2025 for a panel of 13 multinational electronics corporations with significant global operations, including headquarters in the United States (e.g., Apple, Intel), Asia (e.g., Samsung, LG), and Europe (e.g., Infineon). Stock price data were retrieved using the yfinance Python library. Environmental, Social, and Governance (ESG) scores were primarily obtained using the Python yesg library [41]. The methodologies of Sustainalytics and MSCI were reviewed for contextual understanding [42,43]. Data for the Fama-French five- factor model plus momentum (FF6) were sourced from Kenneth R. French's Data Library [44].

Variables

For the analysis, several variables were constructed. The dependent variable for the panel regression was Excess_Return_ it, defined as the monthly excess return for firm i at time t. This was calculated by subtracting the risk-free rate, obtained from the Fama-French dataset, from the firm's stock return. The key independent variables in the panel regression included Lagged_ Total-Score_it-l, representing the overall ESG score for firm i at time t-l, where l signifies various lag lengths of 1, 3, and 6 months. Another key independent variable was Avg12M_Lagged_Total- Score_it, a 12-month moving average of the 1-month lagged total ESG score. Similar lagged and averaged variables were also established for the individual E-Score, S-Score, and G-Score components. Control variables for the panel regression consisted of the contemporaneous monthly returns of the six Fama-French- Momentum factors: MKT_RF_t, SMB_t, HML_t, RMW_t, CMA_t, and WML_t [43]. For the VAR analysis, specific variables were employed, including HML_ESG_t, which is a High-Minus- Low ESG factor. This factor was derived by monthly sorting firms in the sample into three portfolios based on their Lagged_Total- Score, with HML_ESG_t being the equally-weighted average return of the highest ESG portfolio minus that of the lowest ESG portfolio. The VAR analysis also incorpo-rated the six Fama- French-Momentum factors previously mentioned.

Methodology

Panel regression and Vector Autoregression (VAR) methods were employed using statsmodels [67]. For the panel regressions assessing the ESG-return relationship (RQ1), various model specifications were considered. Diagnostic tests (presented in Section 4.4, Table 3) were conducted to guide model selection. The F-test for entity fixed effects versus Pooled OLS was not statistically significant (p=0.5713), and the Breusch-Pagan test for random effects residuals indicated homoskedasticity (p=0.430). While an informal Hausman test showed negligible differences between Fixed Effects (FE) and Random Effects (RE) coefficients, the lack of significance in the F-test made the choice less clear- cut based solely on these statistical tests. However, given the paramount importance of controlling for unobserved time- invariant firm characteristics and common time-varying shocks in finance research, and as a common robust practice, the Two-Way Fixed Effects (Entity and Time) model with firm-clustered standard errors was adopted as the primary specification for presenting the main results. This model is specified as:

Excess_Return_it = α_i + λ_t + β1*ESG_Score_it-l + Σ_k β_k*ControlFactor_kt + ε_it [66].

Results from alternative specifications (e.g., Pooled OLS, Random Effects) are available in the sup-plementary material to demonstrate robustness. A VAR (1) model (lag selected by BIC) explores dy- namic interplay (RQ2) via Granger causality, IRFs, and FEVDs. Jensen's alpha for the HML_ESG factor is estimated via OLS with HAC robust standard errors4. Diagnostic Testing of Variables and Regression Models. To establish the econometric soundness of the subsequent empirical analyses, a series of diagnostic examinations was performed on the dataset and the proposed regression frame- works. These tests are crucial for ensuring the validity and reliability of the study's findings.

Diagnostic Testing of Variables and Regression Models

Assessment of Inter-Variable Correlations

Examining the pairwise links between the main variables utilized in the panel regressions, including several lagged ESG scores and the Fama-French-Momentum factors, a Pearson correlation analysis was conducted. The correlation matrix (available from the author upon request) revealed generally low levels of association between the ESG metrics and the market risk factors. This outcome allevi-ates concerns regarding potential issues of severe multicollinearity, which could otherwise compro-mise the precision and interpretability of the estimated coefficients for the ESG variables in the panel regression analyses.

Unit Root Tests for Time Series Stationarity

Time series variables employed in the Vector Autoregression (VAR) model, namely, the constructed HML_ESG factor, MKT_ RF, SMB, HML, RMW, CMA, and WML, were subjected to the Aug-mented Dickey–Fuller (ADF) test to assess their stationarity. The results, summarized in Table 1, confirm that all series are stationary at conventional significance levels (all p-values < 0.01), indicat-ing that they do not contain a unit root and can be appropriately included in the VAR model in their level form.

|

Variable |

ADF Statistic |

P-value |

Conclusion |

|

HML_ESG |

-10.987 |

0.000 |

Stationary |

|

MKT_RF |

-11.543 |

0.000 |

Stationary |

|

SMB |

-10.312 |

0.000 |

Stationary |

|

HML |

-8.765 |

0.001 |

Stationary |

|

RMW |

-9.987 |

0.000 |

Stationary |

|

CMA |

-9.123 |

0.000 |

Stationary |

|

WML |

-10.501 |

0.000 |

Stationary |

Table 1: Augmented Dickey-Fuller (ADF) Test for Stationarity of VAR Input Variables

Examination of Residual Serial Correlation

Following the estimation of each panel regression model, the Durbin–Watson (DW) test statistic was calculated from the model residuals to detect the presence of first-order serial correlation. These sta-tistics are noted with the primary regression outputs in Section 5. For the VAR model, DW statistics for the residuals of

each equation are presented in Table 2. The values obtained are all close to 2.0, suggesting the absence of significant first-order autocorrelation in the VAR model's residuals. Firm-clustered standard errors were also consistently employed in panel regressions.

|

Variable |

Durbin-Watson |

|

HML_ESG |

2.0327 |

|

MKT_RF |

2.0122 |

|

SMB |

1.9819 |

|

HML |

2.0625 |

|

RMW |

2.0070 |

|

CMA |

2.0438 |

|

WML |

2.0372 |

Table 2: Durbin-Watson Statistics for VAR (1) Model Residuals

Panel Model Specification and Heteroskedasticity Tests

Table 3 summarizes key panel model specification tests. The Breusch–Pagan (BP) test for the primary Two-Way Fixed Effects model (LM-statistic = 6.99, p-value = 0.430) did not reject homoskedas-ticity. Despite this, and considering the F-test for entiteffects was not significant, the Two-Way Fixed Effects model was chosen as the primary approach for its robustness in controlling for unob-served heterogeneity and common time shocks, which is crucial in studies of this nature. Firm-clustered standard errors were employed throughout for conservative inference.

|

Test |

Statistic |

P-value/Note |

Conclusion |

|

F-test (Entity FE vs Pooled OLS) |

0.876 |

0.5713 |

Entity FE not significant |

|

Hausman (Informal) |

Comparison |

FE:0.0000, RE:0.0000. Diff:0.0000 |

Choice less clear (F-test not sig.) |

|

Breusch-Pagan (Entity FE resid) |

LM:6.99 |

Pval:0.430 |

Homoskedasticity |

Table 3: Panel Model Specification Tests Summary

Empirical Results

This section presents the main findings from the panel regressions and VAR analysis.

Panel Regressions of Global Electronics Firm Stock Returns on ESG Performance

The results from the Two-Way Fixed Effects panel regressions for the 13 multinational electronics firms (N=1519 firm-month observations), controlling for the six Fama-French-Momentum factors, are summarized in Table 4. This table highlights the outcomes for the ESG variables that demonstrated statistical significance in this chosen primary model. Comprehensive regression outputs for all twelve ESG variable specifications (Total, E, S, and G scores with 1-month, 3-month, 6-month, and

12-month average lags) using this Two-Way Fixed Effects model, which can be accessed via the supplementary material.

|

ESG Variable |

Coefficient |

Std. Error |

T-stat |

P-value |

Significant (5%) |

|

Lagged_Total-Score |

0.0006 |

0.0002 |

2.3222 |

0.0204 |

TRUE |

|

Lagged6M_Total-Score |

0.0006 |

0.0002 |

2.7619 |

0.0058 |

TRUE |

|

Avg12M_Lagged_Total-Score |

0.0008 |

0.0002 |

4.6279 |

0.0000 |

TRUE |

|

Lagged_S-Score |

0.0005 |

0.0002 |

2.1862 |

0.0290 |

TRUE |

|

Lagged6M_S-Score |

0.0006 |

0.0002 |

2.4464 |

0.0146 |

TRUE |

|

Avg12M_Lagged_S-Score |

0.0007 |

0.0002 |

3.1168 |

0.0019 |

TRUE |

Table 4: Summary of Panel Regression Results: Excess Returns on Key Lagged ESG Scores (Two-Way Fixed Effects with FF6

Controls, N=1519)

The analysis indicates a statistically significant positive association between longer-term, sustained ESG performance and stock excess returns. The 12-month average lagged total ESG score (Avg12M_ Lagged_Total-Score) shows the most robust positive relationship. A similar significant positive impact is observed for the 12-month average lagged Social-score (Avg12M_Lagged_S-Score). Shorter- term lags and individual Environmental and Governance scoresgenerally did not ex-hibit statistically significant associations in this primary model. A sub-period robustness check (Table 5) indicated some variations, particularly in the post-2020 period, where some S-score significances were borderline, potentially reflecting evolving market conditions or the impact of the smaller sample size in sub-periods.

|

Period |

ESG_Variable |

Coefficient |

P_Value |

Significant_5pct |

N_Obs |

R_squared |

|

First Half |

Lagged_Total-Score |

0.0000 |

0.8813 |

FALSE |

793 |

1.01E-05 |

|

First Half |

Lagged6M_Total-Score |

0.0007 |

0.3497 |

FALSE |

793 |

0.0010 |

|

First Half |

Avg12M_Lagged_Total-Score |

0.0006 |

0.4866 |

FALSE |

793 |

0.0006 |

|

First Half |

Lagged_S-Score |

0.0004 |

0.3257 |

FALSE |

793 |

0.0012 |

|

First Half |

Lagged6M_S-Score |

0.0006 |

0.3370 |

FALSE |

793 |

0.0012 |

|

First Half |

Avg12M_Lagged_S-Score |

0.0008 |

0.2127 |

FALSE |

793 |

0.0016 |

|

Second Half |

Lagged_Total-Score |

0.0007 |

0.3958 |

FALSE |

726 |

0.0007 |

|

Second Half |

Lagged6M_Total-Score |

0.0002 |

0.4036 |

FALSE |

726 |

0.0002 |

|

Second Half |

Avg12M_Lagged_Total-Score |

0.0011 |

0.1923 |

FALSE |

726 |

0.0018 |

|

Second Half |

Lagged_S-Score |

0.0026 |

0.0524 |

FALSE |

726 |

0.0016 |

|

Second Half |

Lagged6M_S-Score |

0.0005 |

0.4352 |

FALSE |

726 |

0.0010 |

|

Second Half |

Avg12M_Lagged_S-Score |

0.0020 |

0.3647 |

FALSE |

726 |

0.0037 |

Table 5: Sub-Period Analysis Summary: Two-Way FE Regressions (ESG only Models)

VAR Analysis of HML_ESG Factor and Market Factors

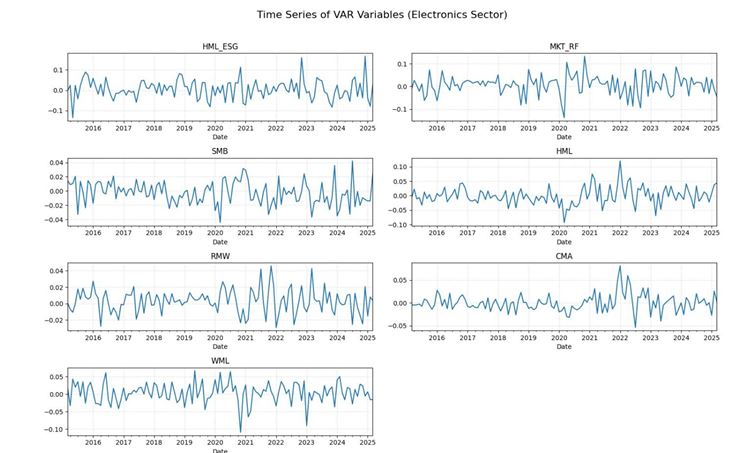

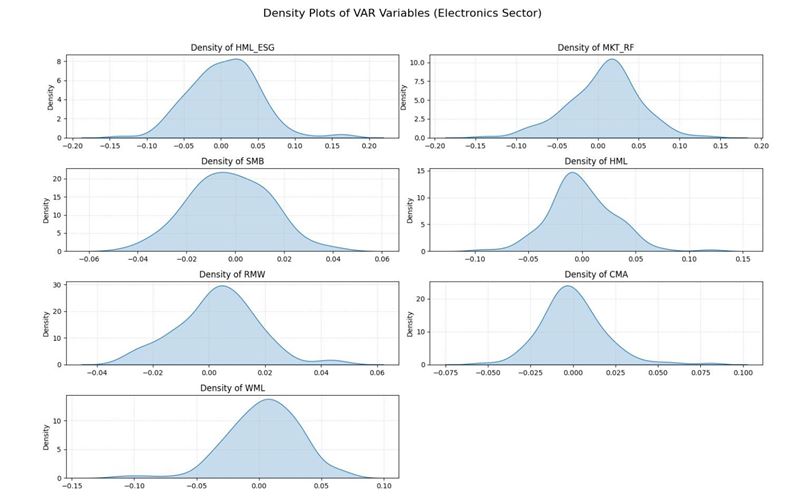

A VAR (1) model was estimated. Key diagnostic plots for the VAR input data, including time series plots of the HML_ESG factor and key market factors, their density distributions, and a scatterplot matrix, are presented in Figures 1, 2, and 3, respectively, to visualize their characteristics and co-movements before formal testing

Figure 1: Monthly Returns of the Constructed HML_ESG Factor, MKT_RF, SMB, and HML Factors over the Sample Period

Figure 2: Kernel Density Estimates for the Monthly Returns of HML_ESG, MKT_RF, SMB, and HML Factors.

Granger causality tests (Table 6) showed no statistically significant causality from the block of FF6 factors to HML_ESG (p=0.723) or

vice-versa for individual factors.

|

Causality Direction |

F-Stat |

P-Value |

Significant (5%) |

|

MKT_RF, SMB, HML, RMW, CMA, WML -> HML_ESG |

0.61 |

0.723 |

FALSE |

|

HML_ESG -> MKT_RF |

0.63 |

0.427 |

FALSE |

|

HML_ESG -> SMB |

0.99 |

0.321 |

FALSE |

|

HML_ESG -> HML |

0.6 |

0.438 |

FALSE |

|

HML_ESG -> RMW |

0.03 |

0.853 |

FALSE |

|

HML_ESG -> CMA |

0.12 |

0.73 |

FALSE |

|

HML_ESG -> WML |

1.22 |

0.27 |

FALSE |

Table 6: Granger Causality Tests from VAR (1) Model

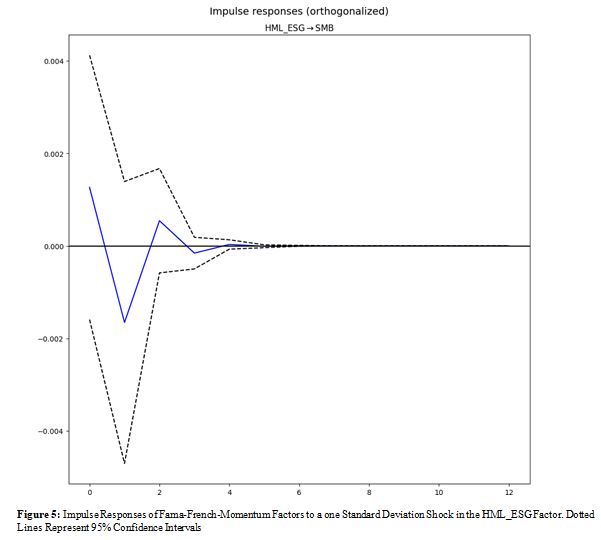

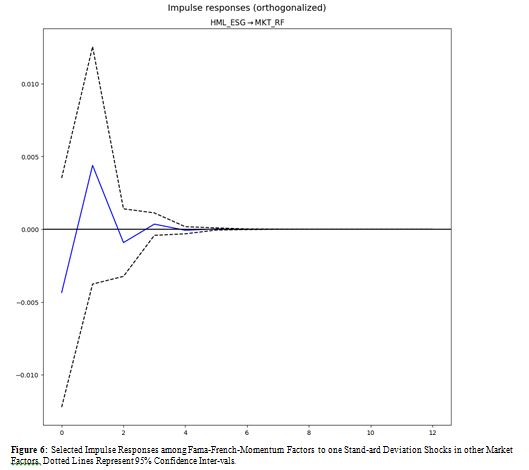

Impulse Response Functions (IRFs) are depicted in Figures 4, 5, and 6. Figure 4 shows the responses of the HML_ESG factor to one standard deviation shocks in each of the Fama-French-Momentum factors. Figure 5 illustrates the responses of the Fama-French- Momentum factors to a one standard deviation shock in the HML_ESG factor. Figure 6 presents selected cross-responses among the Fama-French-Momentum factors themselves. Collectively, these plots visually confirm generally weak and statistically insignificant dynamic linkages involving the HML_ESG factor over the 12-month forecast horizon.

The Forecast Error Variance Decomposition (FEVD) for HML_ ESG is summarized in Table 7. The results show that HML_ESG's innovations explain approximately 96.7% of its forecast error variance after 12 periods. The FEVDs for the other factors in the system (available from the author upon request) further illustrate the limited explanatory power of HML_ESG for their variances.

|

Period |

HML_ESG |

MKT_RF |

SMB |

HML |

RMW |

CMA |

WML |

|

0 |

1.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

0.0000 |

|

1 |

0.9684 |

0.0055 |

0.0023 |

0.0002 |

0.0031 |

0.0157 |

0.0049 |

|

2 |

0.9674 |

0.0056 |

0.0023 |

0.0002 |

0.0035 |

0.0157 |

0.0052 |

|

3 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

4 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

5 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

6 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

7 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

8 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

9 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

10 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

|

11 |

0.9673 |

0.0056 |

0.0023 |

0.0003 |

0.0035 |

0.0157 |

0.0052 |

Table 7: Forecast Error Variance Decomposition (FEVD) for HML_ESG (Selected Horizons)

The time-series OLS regression of HML_ESG on the contemporaneous FF6 factors (Table 8) yielded an insignificant monthly alpha of 0.0061 (p=0.141).

|

Variable |

coef |

std err |

z |

P>|z| |

25th percentile |

Upper 95% CI |

|

const |

0.0061 |

0.0040 |

1.4740 |

0.1410 |

-0.0020 |

0.0140 |

|

MKT_RF |

-0.1657 |

0.0900 |

-1.8330 |

0.0670 |

-0.3430 |

0.0110 |

|

SMB |

0.2929 |

0.2420 |

1.2100 |

0.2260 |

-0.1820 |

0.7670 |

|

HML |

0.0747 |

0.2670 |

0.2800 |

0.7790 |

-0.4480 |

0.5980 |

|

RMW |

0.6050 |

0.3200 |

1.8880 |

0.0590 |

-0.0230 |

1.2330 |

|

CMA |

0.0963 |

0.3730 |

0.2580 |

0.7960 |

-0.6350 |

0.8280 |

|

WML |

-0.2878 |

0.2040 |

-1.4100 |

0.1590 |

-0.6880 |

0.1120 |

|

Notes: N=121. R-squared=0.065. Durbin-Watson=1.881. |

||||||

Table 8: OLS Regression of HML_ESG Factor on FF6 Factors (Alpha Test)

These VAR results collectively suggest that the HML_ESG factor, within this sample of global elec-tronics firms, demonstrates considerable independence from traditional market risk factors.

Discussion and Implications

The empirical findings of this study, based on an analysis of 13 multinational electronics firms, offer quantitative insights into the financial dimensions of ESG performance within the context of increas-ing global sustainability regulations and rapid technological advancements. The discussion now in-terprets these results in light of existing theories and their broader implications.

Addressing RQ1, the panel regression analysis suggests that sustained, long-term ESG performance, particularly in aggregate (Total-Score) and specifically through the Social (S) pillar, is positively and significantly associated with stock excess returns for the sampled firms (Table 4). This indicates that financial markets may recognize and potentially reward consistent and comprehensive ESG com-mitments by these global electronics players, aligning with aspects of stakeholder theory where ad- dressing broader societal concerns can lead to enhanced firm value and observed impacts of sustain-ability on organizational performance [4,46-48,62]. The specific salience of the S-score could reflect the heightened global investor and regulatory attention to social issues within the complex interna-tional supply chains of the electronics industry, such as labor practices, human rights, and community engagement [9,11,20,22,49,50,56]. The finding that markets appear to value sustained ESG per-formance (e.g., 12-month averages) over shorter-term fluctuations reinforces the idea that markets value deeply embedded, strategic commitments to sustainability rather than transient or superficial activities [2,20,54].

Regarding RQ2, the VAR analysis shows limited dynamic interaction between the construct-ed HML_ESG factor and traditional Fama-French-Momentum market risk factors for this sample of global electronics firms (Table 6, Figures 4-6, Table 7). The general absence of significant Granger causality and the FEVD results, where HML_ESG variance is largely self-explained, suggest that ESG performance in this sector might embody distinct risk characteristics not fully captured by con-ventional global market models [44,66,57]. This aligns with the broader inquiry into ESG as a unique financial factor [66,54]. Although the HML_ ESG factor did not generate statistically significant al-pha in this study (Table 8), its apparent orthogonality to established market factors is an area war-ranting further investigation.

Financial Salience of ESG Performance in a Global and Regulated High-Tech Sector

The panel regression analysis addressing RQ1 (Table 4) reveals a statistically significant positive association between sustained, long-term aggregate Environmental, Social, and Governance (ESG) scores, as well as specifically Social (S) pillar scores, and stock excess returns for the sampled global electronics firms. This observation suggests that financial markets may indeed recognize and reward consistent and comprehensive ESG commitments made by these multinational corporations. Such findings are particularly pertinent given that these firms operate within a complex and increasingly stringent web of international sustainability regulations, as detailed in Section 2.1. The observed market premium for sustained ESG performance, especially 12-month average scores, implies that investors potentially value deeply embedded, strategic commitments to sustainability over transient or superficial activities [2,20,54].

The particular salience of the S-score in this context could reflect heightened global investor and regulatory attention to social issues inherent in the electronics industry's extensive international sup-ply chains. These include labor practices, human rights, and community impacts, all of which are subject to growing scrutiny and specific legislative actions worldwide [9,11,20,22,49,50,56]. The ability of firms to effectively manage these social risks and capitalize on related opportunities, often in response to regulatory pressures, appears to be a factor in their market valuation. The less con-sistent significance for standalone Environmental (E) or Governance (G) scores in the primary models might suggest that their financial impacts are more nuanced for this sample, potentially being realized over different time horizons, being more heterogeneously managed or disclosed, or being partially subsumed within the broader total and social ESG metrics. The strategic adoption of emerging technologies, as discussed in Section 2.2, is likely a key enabler for firms to achieve the type of ro-bust and transparent ESG performance that markets seem to value [2,3,20,65].

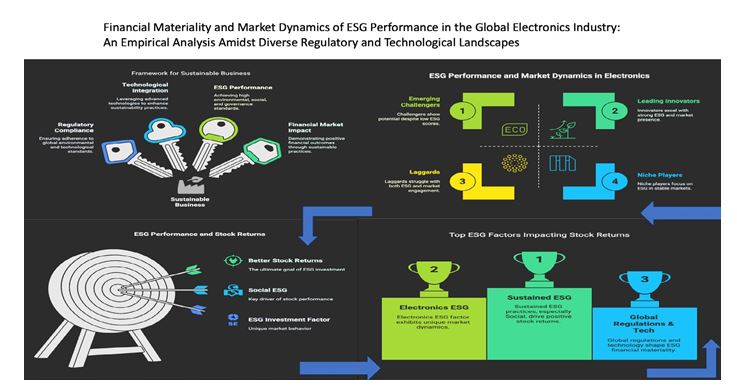

A Conceptual Global Regulatory-ESG Financial Salience Model (RQ3)

The empirical findings, interpreted within this global context, inform a "Global Regulatory-ESG Fi-nancial Salience Model" (Figure 7). This model, conceptually aligned with frameworks for navigating global electronics regulations, illustrates the potential pathways through which regulatory pressures and technological capabilities can interact with ESG performance to influence financial market outcomes [20].

Figure 7, a conceptual model illustrating the interplay between global regulations, technological ena-blement, ESG performance, and potential financial market signals in the electronics industry. This model posits that (1) converging global regulatory pressures drive firms towards enhanced ESG management, (2) strategic adoption of technology is key to managing global ESG compliance and performance, (3) financial markets may recognize and reward sustained, material ESG efforts, and (4) ESG performance in this sector may represent a financially distinct factor. Proactive and techno-logically adept navigation of global sustainability regulations, as suggested by, can be financially salient [20].

Implications for Stakeholders

The study implies that multinational electronics firms should prioritize strategic, long-term ESG in-tegration, leveraging technology to address diverse global regulatory demands, particularly in socially material areas [19,20,61]. For investors, the findings suggest potential value in considering sustained ESG metrics and the distinct risk profile of ESG in this sector. Policymakers globally can infer that well-designed regulations may be increasingly reflected in market valuations, potentially validating aspects of the Porter Hypothesis where regulation drives innovation [26,54,56,57].

Limitations and Future Research

The primary limitation of this study is the sample size (N=13 firms), which, although representing major global players, restricts the statistical power and generalizability of the quantitative findings beyond this specific group and timeframe. ESG data sourced primarily via yes g, reflects publicly available information and may differ from proprietary ESG datasets [41-43]. The construction of the HML_ESG factor is also specific to this study's sample and methodology. While Two-Way Fixed Effects models were employed, unobserved variables or more complex endogeneity issues could still affect the ESG-finance relationship [66,67]. The analysis provides a financial market per-spective and does not directly measure the specific adoption levels of emerging technologies or the direct causal impact of individual regulatory enactments on operational innovation processes [20].

Future research should aim to expand the quantitative analysis to a larger and more geographically diverse sample of global electronics firms. Comparative studies examining the ESG-finance link un-der different national or regional regulatory regimes would be highly valuable. Investigating the moderating role of specific technological adoptions on the ESG-financial performance relationship is another promising avenue. Furthermore, event studies focusing on the market reaction to significant global or regional regulatory announcements on electronics sustainability could provide more direct evidence of regulatory impact. Finally, exploring alternative constructions of ESG factors and testing their robustness across different asset pricing models would contribute to the ongoing debate about ESG's role as a distinct financial factor in the global electronics industry.

Summary and Conclusions

This quantitative study examined the financial materiality and market dynamics of ESG performance for 13 multinational electronics firms operating globally, from 2015 to 2025. Panel regression anal-yses, controlling for Fama-French-Momentum factors, indicated that sustained, long-term total ESG scores and Social (S) pillar scores are positively and significantly associated with stock excess returns for this sample. A Vector Autoregression analysis of a constructed ESG factor suggested its limited dynamic linkage with traditional market risk factors, hinting at distinct ESG risk/return characteristics in this sector.

These findings, contextualized by global sustainability regulations and technological enablers, inform a "Global Regulatory-ESG Financial Salience Model." This model suggests that firms effectively navigating global regulations and strategically investing in sustained, technologically-enabled ESG performance may achieve favorable financial market recognition [20]. While the empirical evidence is based on a specific sample, it offers insights into the growing financial relevance of ESG for global electronics companies, highlighting the importance of proactive sustainability strategies in an increasingly regulated and technologically evolving world. The study's limitations, particularly sample size, underscore the need for future research with broader global datasets to further validate these observations [68,69].

Patents

There are no patents resulting from the work reported in this manuscript.

Supplementary Materials

The following supporting information can be downloaded at: https://www.mdpi.com/article/doi/s1, Figure 1: F-test for Poolability Result for the Avg12M_Lagged_G-Score Panel Regression Model.; Table 1: Panel Model Specification Tests Summary; Table 2: Summary of Panel Regression Results for the Impact of Analogous Sustainable Technology Adoption Characteristics on Sustainable Value Creation Index (SVCI).

Author Contributions

Conceptualization, H.E.O.O.; methodology, H.E.O.O.; software, H.E.O.O.; validation, H.E.O.O.; formal analysis, H.E.O.O.; investigation, H.E.O.O.; resources, H.E.O.O.; data curation, H.E.O.O.; writing—original draft preparation, H.E.O.O.; writing—review and editing, H.E.O.O.; visualization, H.E.O.O.; supervision, H.E.O.O.; project administration, H.E.O.O.; funding acquisition, H.E.O.O. The author has read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The Fama-French factor data are publicly available from Kenneth R. French's Data Library. ESG scores were primarily sourced via the yesg Python library; methodologies of commercial providers were referenced [41-43]. Derived datasets and Python scripts are available within the article or as supplementary material associated with this publication and will be made available as supplementary material on the publisher's website upon publication.

Acknowledgments

Not applicable.

Conflicts of Interest

The author declares no conflicts of interest.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content.

References

1. Guo, F., Lou, Y., Yan, Q., Xiong, J., Luo, J., Shen, C., & Vayenas, D. V. (2023). Insight into the Fe–Ni/biochar composite supported three-dimensional electro-Fenton removal of electronic industry wastewater. Journal of Environmental Management, 325, 116466.

2. Singh, A., Goel, A., Chauhan, A., & Singh, S. K. (2025). Sustainability of Electronic Product Manu-facturing through E-Waste Management and Reverse Logistics. Sustainable Futures, 100490.

3. Mathiyazhagan, K., Gnanavelbabu, A., & Agarwal, V. (2022). A framework for implementing sus-tainable lean manufacturing in the electrical and electronics component manufacturing industry: An emerging economies country perspective. Journal of Cleaner Production, 334, 130169.

4. Alomar, T. A. (2023). A Cross-country Study of Stakeholder Pressure on Oil and Gas Companies' Environmental Performance and Disclosures. Ph.D. Thesis, RMIT University, Melbourne, Australia.

5. Valtanen, K., Saari, L. M., Acerbi, F., Pinzone, M., Pachimuthu, D., Canavesi, R., ... & Nylander, J. (2025). Matching Circularity Improvements and Digital Product Passport Viewpoints: Insights from Three Industrial Case Studies. Procedia Computer Science, 253, 1720-1729.

6. Divyasri, D., Kumar, D. V., Babu, D. R., & Vedik, B. (2025). Recycling of E-waste and Green Elec-tronic Manufacturing. In E3S Web of Conferences (Vol. 619, p. 01013). EDP Sciences.

7. Suppipat, S., & Hu, A. H. (2022). Achieving sustainable industrial ecosystems by design: A study of the ICT and electronics industry in Taiwan. Journal of Cleaner Production, 369, 133393.

8. Hakola, L., Abedi, F., Nordman, S., Smolander, M., & Paltakari, J. (2025). Smart Tags as Enablers for Digital Product Passports in Circular Electronics Value Chains. Circular Economy and Sustaina-bility, 1-23.

9. Park, S. R., Kim, S. T., & Lee, H. H. (2022). Green supply chain management efforts of first-tier suppliers on economic and business performances in the electronics industry. Sustainability, 14(3), 1836.

10. Li, S., & Sun, Q. (2023). Evolutionary game analysis of WEEE recycling tripartite stakeholders under variable subsidies and processing fees. Environmental Science and Pollution Research, 30(5), 11584-11599.

11. Ozturk, I., Ullah, S., Sohail, S., & Sohail, M. T. (2025). How do digital government, circular econo-my, and environmental regulatory stringency affect renewable energy production?. Energy Poli-cy, 203, 114634.

12. Visentin, F., Cantin, J., & Santato, C. (2024). Active and Dynamic Learning in Sustainable Electron-ics. Journal of Chemical Education, 101(8), 3156-3162.

13. Berube, G. M. (2023). Thick-film – a mature technology at the cutting edge of advances in the elec-tronics industry. IMAP Source Proc. , 2022, IMAPS Symposium.

14. Matthess, M., Kunkel, S., Xue, B., & Beier, G. (2022). Supplier sustainability assessment in the age of Industry 4.0– Insights from the electronics industry. Cleaner logistics and supply chain, 4, 100038.

15. Nguyen, K. (2024). Assessment of InnovativeStrategies for Zero-Emissions: Refining of Waste Elec-trical & Electronic Equipment-Specialization in Printed Circuit Boards & Non- Metals.

16. Debnath, B. (2022). Sustainability of WEEE recycling in India. In Re-use and recycling of materi-als (pp. 15-32). River Publishers.

17. Mula, J., Sanchis, R., de la Torre, R., & Becerra, P. (2024). Extended reality and metaverse technol-ogies for industrial training, safety and social interaction. IFAC-PapersOnLine, 58(19), 575-580.

18. Fang, L., Lefranc, P., & Rio, M. (2024). Effective ecodesign implementation in power electronics: a method based on functional blocks. Cogent Engineering, 11(1), 2382232.

19. Cicerelli, F., & Ravetti, C. (2024). Sustainability, resilience and innovation in industrial electronics: a case study of internal, supply chain and external complexity. Journal of Economic Interaction and Coordination, 19(2), 343-372.

20. Onomakpo, H. E. O. (2025). Navigating Global Regulations for Sustainable Electronics: A Strategic Innovation Framework. Int J Bank Fin Ins Tech, 3(1), 42.

21. United Nations Environment Programme. (2020). Global E-waste Monitor 2020: Quantities, Flows, and the Circular Economy Potential. United Nations University/UNITAR: Bonn/Geneva, Switzer-land, 2020.

22. Huang, Y. C., & Chen, C. T. (2023). Institutional pressure, firm's green resources and green product innovation: evidence from Taiwan's electrical and electronics sector. European Journal of Innovation Management, 26(3), 636-664.

23. Oliveira, I. M., Gimenez, J. C., Xavier, G. T., Ferreira, M. A., Silva, C. M., Camargo, E. R., & Cruz, S. A. (2024). Recycling ABS from WEEE with peroxo-modified surface of titanium dioxide parti-cles: alteration on antistatic and degradation properties. Journal of Polymers and the Environ-ment, 32(3), 1122-1134.

24. Salomez, F., Helbling, H., Almanza, M., Soupremanien, U., Vine, G., Voldoire, A., ... & Crébier, J. C. (2024). State of the art of research towards sustainable power electronics. Sustainability, 16(5), 2221.

25. European Commission. Directive 2011/65/EU of the European Parliament and of the Council of 8 June 2011 on the restriction of the use of certain hazardous substances in electrical and electronic equipment (RoHS Recast). Oficial Journal of the European Union L 174/88.

26. Nie, X., Wu, J., Chen, Z., Zhang, A., & Wang, H. (2021). Can environmental regulation stimulate the regional Porter effect? Double test from quasi-experiment and dynamic panel data models. Journal of Cleaner Production, 314, 128027.

27. Wang, Y. (2020). Extend sustainable new product development to suppliers: cases from the US computer and electronic industry. International Journal of Logistics Economics and Globalisa-tion, 8(3), 224-242.

28. National Conference of State Legislatures. Electronic Waste Recycling State Legislation.

29. U.S. Environmental Protection Agency. Toxic Substances Control Act (TSCA).

30. Ministry of the Environment, Japan. (2000). Basic Act on Establishing a Sound Material-Cycle Soci-ety (Law No. 110 of 2000).

31. Government of Canada. (1999). Canadian Environmental Protection Act, 1999 (S.C. 1999, c. 33).

32. Schluep, M., Hagelueken, C., Kuehr, R., et al. (2009). Recycling – from E-waste to Resources. United Nations Environment Programme and United Nations University: Bonn, Germany. (General WEEE in developing countries)

33. Godfrey, L., & Oelofse, S. (2017). Historical review of waste management and recycling in South Africa. Resources, 6(4), 57.

34. OECD. (2019). Global Material Resources Outlook to 2060: Economic Drivers and Environmental Consequences; OECD Publishing: Paris, France.

35. Sangwongwanich, A., Stroe, D. I., Mi, C., & Blaabjerg, F. (2024). Sustainability of power electronics and batteries: a circular economy approach. IEEE Power Electronics Magazine, 11(1), 39-46.

36. Dou, W., Tian, Y., Ye, G., & Zhu, J. (2022). Antenna artificial intelligence: The relentless pursuit of intelligent antenna design [industry activities]. IEEE Antennas and Propagation Magazine, 64(5), 128-130.

37. Huang, X., Zhang, Y., Qi, Y., Huang, C., & Hossain, M. S. (2024). Energy-efficient UAV schedul-ing and probabilistic task offloading for digital twin-empowered consumer electronics industry. IEEE Transactions on Consumer Electronics.

38. Mehrabi, A., Yari, K., Van Driel, W. D., & Poelma, R. H. (2024, September). AI-Driven Digital Twin for Health Monitoring of Wide Band Gap Power Semiconductors. In 2024 IEEE 10th Electron-ics System-Integration Technology Conference (ESTC) (pp. 1-8). IEEE.

39. Borole, Y., Borkar, P., Raut, R., Balpande, V. P., & Chatterjee, P. (2023). Digital Twins: Internet of Things, Machine Learning, and Smart Manufacturing (Vol. 8). Walter de Gruyter GmbH & Co KG.

40. Demir Dogan, T., & Akbas, D. (2023). The Role of Environmental Regulations on Green Transition: The Case of Swedish Electronics Industry.

41. Yesg. (n.d.). (2025). yesg: Retrieve ESG data from Yahoo Finance. PyPI - The Python Package In-dex.

42. Sustainalytics. (n.d.). (2025). ESG Data.

43. MSCI. (n.d.). (2025). ESG Ratings.

44. Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of financial econom-ics, 116(1), 1-22.

45. World Economic Forum. (2019). A New Circular Vision for Electronics: Time for a Global Reboot. World Economic Forum.

46. Magni, D., Palladino, R., Papa, A., & Cailleba, P. (2024). Exploring the journey of responsible busi-ness model innovation in Asian companies: A review and future research agenda. Asia Pacific Jour-nal of Management, 41(3), 1031- 1060.

47. De Beule, F., Dewaelheyns, N., Schoubben, F., Struyfs, K., & Van Hulle, C. (2022). The influence of environmental regulation on the FDI location choice of EU ETS-covered MNEs. Journal of Envi-ronmental Management, 321, 115839.

48. Donaldson, T., & Preston, L. E. (1995). The stakeholder theory of the corporation: Concepts, evi-dence, and implications. Academy of management Review, 20(1), 65-91.

49. Tunde, O. A., Jian, O. Z., Tianyu, W., Khee, W. S., Qiong, W. et al. (2025). Factors Influencing Consumer Satisfaction: An Analysis of Consumer Electronics. Asia Pac. J. Manag. Educ, 8, 150-169.

50. Ahr, C. (2024). The communication of circular business models and the need for collaboration in the electronics industry.

51. Stevels, A. (2023). The challenge of introducing design for the circular economy in the electronics industry: A proposal for metrics. Circular Economy, 2(3), 100051.

52. Freeman, R. E. (1984). Strategic Management: A Stakeholder Approach; Pitman: Boston.

53. Banik, A., Taqi, H. M. M., Ali, S. M., Ahmed, S., Garshasbi, M., & Kabir, G. (2022). Critical success factors for implementing green supply chain management in the electronics industry: an emerging economy case. International Journal of Logistics Research and Applications, 25(4-5), 493-520.

54. Javeed, S. A., Teh, B. H., Ong, T. S., Lan, N. T. P., Muthaiyah, S., & Latief, R. (2023). The connec-tion between absorptive capacity and green innovation: the function of board capital and environ-mental regulation. International Journal of Environmental Research and Public Health, 20(4), 3119.

55. Hart, S. L. (1995). A natural-resource-based view of the firm. Acad. Manag. Rev, 20, 986-1014.

56. Porter, M. E., & Linde, C. V. D. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of economic perspectives, 9(4), 97-118.

57. Ambec, S., Cohen, M. A., Elgie, S., & Lanoie, P. (2013). The Porter hypothesis at 20: can environ-mental regulation enhance innovation and competitiveness?. Review of environmental economics and policy.

58. Smith, L., Weems, J., Hua, C., Dys, S., Carder, P. et al. (2023). Assessing Regulatory Stringency for Licensed Assisted Living: A Multifaceted Approach. Innov. Aging, 7, 65.

59. Raff, Z., & Earnhart, D. (2022). Employment and environmental protection: The role of regulatory stringency. Journal of Environmental Management, 321, 115896.

60. Ayadi, F. S., Mlanga, S., Ikpor, M. I., & Nnachi, R. A. (2019). Empirical test of Pollution Haven Hypothesis in Nigeria using autoregressive distributed lag (ARDL) model. Social Sciences, 10(3).

61. Knaack, P., & Gruin, J. (2021). From shadow banking to digital financial inclusion: China’s rise and the politics of epistemic contestation within the financial stability board. Review of International Po-litical Economy, 28(6), 1582-1606.

62. Eccles, R. G., Ioannou, I., & Serafeim, G. (2014). The impact of corporate sustainability on organi-zational processes and performance. Management science, 60(11), 2835-2857.

63. New Zealand Ministry for the Environment. Waste Minimisation Act 2008.

64. Kshetri, N. (2018). 1 Blockchain’s roles in meeting key supply chain management objec-tives. International Journal of information management, 39, 80-89.

65. Benešová, A., Hirman, M., Steiner, F., & Tupa, J. (2024, May). Towards Sustainable Electronics: Unveiling the Nexus of Circular Economy, Global Policies and Industry Impacts. In 2024 47th Inter-national Spring Seminar on Electronics Technology (ISSE) (Vol. 2024, pp. 1-6). IEEE.

66. Onomakpo, H. E. O. (2025). ESG Risk Ratings and Stock Performance in Electric Vehicle Manufac-turing: A Panel Regression Analysis Using the Fama-French Five-Factor Model. J Invest Bank Fi-nance, 3(1), 01-13.

67. Seabold, S., Perktold, J., & Shedden, K. (2017). statsmodels/ statsmodels: Version 0.8. 0 Re-lease. Zenodo.

68. Gaikwad, A. (2024). Reliability estimation and lifecycle assessment of electronics in extreme condi-tions. Available at SSRN 5074918.

69. Suppipat, S., & Hu, A. H. (2022). A scoping review of design for circularity in the electrical and electronics industry. Resources, Conservation & Recycling Advances, 13, 200064.