International Journal of Natural Sciences and Interdisciplinary Research(IJNSIR)

ISSN: 3143-1046 | DOI: 10.33140/IJNSIR

Research Article - (2026) Volume 1, Issue 2

Financial Feasibility, Cost Structure, and Profitability Determinants of Smallholder Pepper Farming: An Integrated Cost-Revenue and Sensitivity Analysis

2Department of Socio-Economics of Agriculture, Faculty of Agriculture, Hasanuddin University, Makassar, Indonesia

Received Date: Apr 15, 2026 / Accepted Date: May 11, 2026 / Published Date: May 22, 2026

Copyright: ©2026 Jumiati Jumiati, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Tahir, A. R., Jumiati, J., Ikmal, M., Rumallang, A., Molla, S., et al. (2026). Financial Feasibility, Cost Structure, and Profitability Determinants of Smallholder Pepper Farming: An Integrated Cost-Revenue and Sensitivity Analysis. Int Nat Sci Int Rese, 1(2), 01-08.

Abstract

This study evaluates the financial feasibility, cost structure, and profitability determinants of smallholder pepper (Piper nigrum L.) farming using processed farm-level cost and revenue data from 22 respondents. The analysis integrates farm budgeting, revenue-cost ratio analysis, cost-share decomposition, sensitivity simulation, and regression-based interpretation of profitability drivers. The results show that pepper farming is financially feasible under observed production and price conditions. Average total revenue reached IDR 292,900,000 per year, while average total cost was IDR 52,280,000 per year, generating average net income of IDR 240,620,000 and an R/C ratio of 5.62. Variable costs dominated total production costs, especially labor cost, which accounted for 49% of total cost, followed by pesticide cost (19%), fertilizer cost (15%), depreciation (14%), and land tax (3%). Sensitivity analysis indicates that profitability remains feasible under simulated adverse scenarios, although output price and production shocks reduce profitability more sharply than moderate variable-cost increases. A 20% price or production decline reduced the R/C ratio to 4.48, whereas a 20% increase in variable costs reduced it to 4.80. The regression-based interpretation suggests that farm size and farming experience strengthen profitability, while a high labor-cost share reduces financial efficiency. These findings highlight that smallholder pepper farming has strong income potential, but long-term sustainability depends on yield stability, labor efficiency, input-use optimization, and improved market-risk management.

Keywords

Black Pepper, Farm Budgeting, Cost Structure, Profitability, Sensitivity Analysis, Smallholder Agriculture

Introduction

Black pepper (Piper nigrum L.) is a high-value perennial spice crop cultivated widely in tropical farming systems. It contributes to rural household income, export earnings, and agricultural diversification. In smallholder settings, pepper offers relatively high revenue potential, but profitability is strongly affected by production risk, input-price changes, labor availability, and output-price volatility. Earlier work on black pepper has emphasized the importance of agronomic management, price dynamics, and smallholder market conditions in shaping farm decisions and income outcomes [1-3].

Smallholder pepper farms are typically heterogeneous in land size, labor use, input intensity, and marketing access. Such heterogeneity creates differences in total production cost, revenue, and profitability across farms. Therefore, a feasibility assessment should not only compare total revenue and total cost but should also identify the components of production cost that place the greatest pressure on net income. This is especially important because labor, fertilizer, and pesticide expenditures often constitute large variable costs in perennial crop systems. Studies on smallholder and horticultural commodities show that market structure, input allocation, and farm management practices influence farmers’ income and marketing performance [4-6].

Financial feasibility in farm management is commonly evaluated through farm budgeting, net income, and revenue-cost (R/C) ratio analysis. An R/C ratio greater than one indicates that a farming enterprise generates revenue above total production cost. However, profitability measured under observed conditions is not sufficient to understand the resilience of the farming system. Agricultural enterprises face production and market uncertainty, including price decline, yield reduction, and input-cost increases. Break-even and sensitivity analyses are therefore needed to assess how robust farm profitability remains when key variables change. The profitability of smallholder agriculture is also shaped by socio-economic characteristics. Farm size may provide scale advantages and improve input allocation, while experience can strengthen managerial decision-making. Conversely, an excessive labor-cost share may reduce efficiency because a larger portion of total cost is absorbed by hired or imputed labor. Similar evidence from Indonesian crop studies indicates that farm and farmer characteristics, input allocation, production factors, and marketing structure are critical determinants of farm performance [4,6-8].

Although studies on agricultural profitability and feasibility are abundant, many apply only descriptive cost-benefit analysis. Fewer studies combine cost decomposition, sensitivity simulation, and explanatory interpretation of profitability determinants in a single empirical framework. This study addresses that gap by conducting an integrated financial analysis of smallholder pepper farming. Specifically, this study aims to: (1) estimate total revenue, total cost, net income, and R/C ratio; (2) identify dominant production-cost components; (3) assess profitability resilience under simulated price, production, and variable-cost shocks; and (4) interpret socio¬economic and cost-structure determinants of profitability.

Materials and Methods

Research Design and Data Structure

This study used a quantitative cross-sectional design based on processed farm-level data from 22 smallholder pepper farmers. The unit of analysis was the individual pepper farming enterprise observed over one production year. The processed dataset integrated farmer characteristics, production quantity, selling price, fixed asset depreciation, land tax, labor costs, fertilizer costs, pesticide costs, and farm-level revenue-cost summaries.

The analytical framework links farmer characteristics and production factors to cost structure, revenue, and profitability. Farmer characteristics include age, education, farming experience, household dependents, and farm size. Production factors include production quantity, output price, and input use. Cost structure consists of fixed costs and variable costs. Financial performance is measured by total revenue, total cost, net income, and R/C ratio. Sensitivity analysis evaluates how these indicators change under adverse scenario

Figure 1: Conceptual Framework Linking Farmer Characteristics, Cost Structure, Production, Revenue, and Profitability

Figure 2: Data Integration Flowchart Used to Construct the Analytical Dataset

Variable Definition

Table 1 presents the main analytical variables used in the study. Revenue and profitability indicators were derived from production and cost variables. Cost-share variables were calculated to identify the relative contribution of each cost component to total production cost.

|

Variable category |

Variable |

Unit |

Description |

|

Farmer characteristics |

Age |

years |

Socio-demographic control variable |

|

Farmer characteristics |

Education level |

ordinal |

Human-capital proxy |

|

Farmer characteristics |

Farming experience |

years |

Managerial experience indicator |

|

Farmer characteristics |

Household dependents |

persons |

Household labor-burden indicator |

|

Farmer characteristics |

Farm size |

ha |

Scale of farming operation |

|

Production |

Production quantity (Q) |

kg/year |

Annual pepper output |

|

Production |

Output price (P) |

IDR/kg |

Farm-gate selling price |

|

Revenue |

Total revenue (TR) |

IDR/year |

Q × P |

|

Fixed cost |

Depreciation |

IDR/year |

Straight-line depreciation of fixed assets |

|

Fixed cost |

Land tax |

IDR/year |

Annual land-tax obligation |

|

Variable cost |

Labor cost |

IDR/year |

Sum of labor cost by activity |

|

Variable cost |

Fertilizer cost |

IDR/year |

Fertilizer expenditure |

|

Variable cost |

Pesticide cost |

IDR/year |

Pesticide expenditure |

|

Aggregate cost |

Total fixed cost (TFC) |

IDR/year |

Depreciation + land tax |

|

Aggregate cost |

Total variable cost (TVC) |

IDR/year |

Labor + fertilizer + pesticide |

|

Aggregate cost |

Total cost (TC) |

IDR/year |

TFC + TVC |

|

Profitability |

Net income (π) |

IDR/year |

TR - TC |

|

Profitability |

R/C ratio |

ratio |

TR / TC |

|

Derived indicator |

Cost share |

% |

Component cost / TC × 100 |

Table 1: Structure of the Analytical Dataset and Variable Sources

Results

Production and Aggregate Financial Performance

The processed data indicate that smallholder pepper farming generated substantial revenue relative to production cost. Average total revenue reached IDR 292,900,000 per year, while average total cost was IDR 52,280,000 per year. This generated average net income of IDR 240,620,000 per year. The resulting R/C ratio was 5.62, indicating that every IDR 1.00 spent on production generated approximately IDR 5.62 in revenue.

|

Indicator |

Mean value |

Interpretation |

|

Total revenue (TR) |

292,900,000 |

Gross farm income |

|

Total cost (TC) |

52,280,000 |

Total annual production expenditure |

|

Net income (π) |

240,620,000 |

Positive farm return |

|

R/C ratio |

5.62 |

Financially feasible because R/C > 1 |

Table 2: Aggregate Financial Performance of Smallholder Pepper Farming (N = 22)

The R/C ratio substantially exceeds the feasibility threshold. This finding shows that pepper farming was profitable under the observed production and market conditions. Similar feasibility outcomes have been reported in pepper farming in North Lampung, where R/C and investment indicators confirmed financial viability [9]. The high R/C ratio in the present study also aligns with the broader evidence that perennial spice crops can provide significant income when productivity and farm-gate prices remain favorable [1,2].

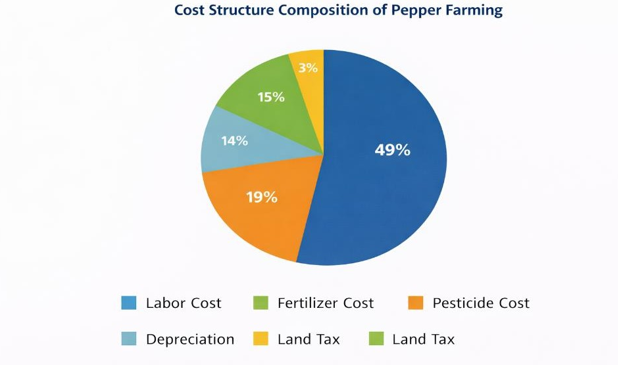

Cost-structure Composition

The cost-share analysis shows that variable costs dominated the production-cost structure. Labor was the largest component, accounting for 49% of total cost. Pesticide cost accounted for 19%, fertilizer cost for 15%, depreciation for 14%, and land tax for 3%. Based on the average total cost of IDR 52,280,000, the derived mean cost values are shown in Table 3.

|

Cost component |

Share of total cost (%) |

Derived mean cost (IDR/year) |

|

Labor cost |

49 |

25,617,200 |

|

Fertilizer cost |

15 |

7,842,000 |

|

Pesticide cost |

19 |

9,933,200 |

|

Depreciation |

14 |

7,319,200 |

|

Land tax |

3 |

1,568,400 |

|

Total |

100 |

52,280,000 |

Table 3: Average Cost-structure Composition of Pepper Farming

Figure 3: Cost-structure Composition of Pepper Farming

The dominance of labor cost confirms that pepper farming remains labor-intensive. A high labor-cost share may reduce profitability when labor use is not proportional to output. At the same time, pesticide and fertilizer costs represent important input-cost pressures. These findings support the need for improved labor planning, input-use efficiency, and integrated pest management to protect profit margins.

Financial Feasibility and Revenue-cost Relationship

The revenue-cost relationship indicates that pepper farming remains financially feasible because revenue is far above total cost. The positive net income and R/C ratio greater than one confirm that observed production and price conditions generated a large safety margin. Such results are consistent with agricultural financial-feasibility principles in which a farm enterprise is considered viable when revenue exceeds total production cost.

Figure 4: Revenue Versus Total Cost of Pepper Farming with Break-even Reference Line

The revenue-cost pattern also suggests that higher-cost farms may be operating at a larger scale, rather than necessarily experiencing inefficiency. However, the relationship between cost and revenue should be interpreted carefully because profitability depends on whether additional spending increases productivity sufficiently to compensate for higher cost.

Sensitivity Analysis

Sensitivity analysis demonstrates that pepper farming remains feasible under all simulated aggregate scenarios. However, price and production reductions have a stronger effect on the R/C ratio than variable-cost increases. A 10% reduction in price or production lowers the R/C ratio from 5.62 to 5.04, while a 20% reduction lowers it to 4.48. In contrast, a 10% increase in variable cost reduces the R/C ratio to 5.17, while a 20% increase reduces it to 4.80. The combined scenario of a 10% price reduction plus 10% variable-cost increase lowers the R/C ratio to 4.66.

|

Scenario |

Adjustment |

TR (IDR) |

TC (IDR) |

Net income (IDR) |

R/C ratio |

|

Baseline |

No change |

292,900,000 |

52,280,000 |

240,620,000 |

5.62 |

|

Price ↓ 10% |

TR × 0.90 |

263,610,000 |

52,280,000 |

211,330,000 |

5.04 |

|

Price ↓ 20% |

TR × 0.80 |

234,320,000 |

52,280,000 |

182,040,000 |

4.48 |

|

Production ↓ 10% |

TR × 0.90 |

263,610,000 |

52,280,000 |

211,330,000 |

5.04 |

|

Production ↓ 20% |

TR × 0.80 |

234,320,000 |

52,280,000 |

182,040,000 |

4.48 |

|

TVC ↑ 10% |

TVC × 1.10 |

292,900,000 |

56,619,240 |

236,280,760 |

5.17 |

|

TVC ↑ 20% |

TVC × 1.20 |

292,900,000 |

60,958,480 |

231,941,520 |

4.80 |

|

Combined shock |

Price ↓ 10% + TVC ↑ 10% |

263,610,000 |

56,619,240 |

206,990,760 |

4.66 |

Table 4: Sensitivity Analysis of Profitability Under Simulated Economic Shocks

Figure 5: Sensitivity of Pepper-farming Profitability to Price, Yield, and Cost Changes

The results indicate that pepper profitability is more exposed to revenue-side shocks than to moderate variable-cost increases. This finding is consistent with the literature on pepper and smallholder agriculture, which shows that price instability and market conditions are central to farm-income outcomes [2,3]. Therefore, price-risk management, quality improvement, collective marketing, and market-information access are important strategies to maintain profitability.

Determinants of Profitability

The processed manuscript identifies farm size, farming experience, education, and labor-cost share as key explanatory variables for profitability. Farm size is expected to increase profitability because larger farms can spread fixed costs over greater output, negotiate better input and output terms, and allocate labor more efficiently. Farming experience is also expected to improve profitability because experienced farmers are more likely to manage input timing, pest control, and harvesting decisions effectively.

Education is expected to have a positive relationship with profitability, although its effect may be weaker than experience in practice-based farming systems. Labor-cost share is expected to have a negative effect because a larger share of total cost devoted to labor reduces the proportion of expenditure available for productivity-enhancing inputs and may signal inefficient labor allocation.

|

Independent variable |

Expected sign |

Interpretation |

|

Constant |

- |

Baseline profitability level |

|

Farm size (ha) |

+ |

Larger farms are expected to achieve higher profitability |

|

Farming experience (years) |

+ |

Experienced farmers are expected to manage production more efficiently |

|

Education level |

+ |

Education may improve decision-making and information use |

|

Labor-cost share (%) |

- |

Higher labor intensity may reduce financial efficiency |

|

R² |

- |

To be inserted from raw-data regression output |

|

Adjusted R² |

- |

To be inserted from raw-data regression output |

|

F-statistic |

- |

To be inserted from raw-data regression output |

Table 5: Regression-output Table for Final Insertion After Statistical Verification

The interpretation is consistent with recent evidence from Indonesian agricultural studies showing that farm characteristics, input allocation, and managerial variables influence production and farm success [5,6,8]. It is also aligned with Jumiati’s previous work on horticultural market performance, which shows that market structure and channel behavior influence the economic outcomes received by farmers [4].

Discussion

The results provide evidence that smallholder pepper farming is financially feasible under observed conditions. The average R/C ratio of 5.62 indicates that revenue substantially exceeds production cost. This confirms that pepper can serve as a profitable commercial crop for smallholders when market price and production performance are favorable. The finding is comparable to previous pepper-feasibility research in Indonesia, which also reported favorable R/C and investment indicators [9].

Despite the strong profitability level, cost-structure analysis reveals a key vulnerability: production cost is dominated by labor. Labor accounted for nearly half of total cost. This means that profitability could decline if wages increase or if labor allocation is inefficient. Labor efficiency is therefore a strategic issue for smallholder pepper farming. Improved work scheduling, collective labor arrangements, selective mechanization, and better harvest planning could reduce unnecessary labor expenses while maintaining yield. Input costs also matter. Fertilizer and pesticide costs together account for 34% of total cost. Although these inputs are necessary to sustain yield and control pests and diseases, inefficient application may reduce net returns. Input-use optimization should therefore be prioritized. Soil-based fertilizer planning, integrated pest management, and farmer training can reduce avoidable input costs and maintain productivity.

The sensitivity analysis shows that profitability is more vulnerable to price and production shocks than to moderate variable-cost increases. A 20% decline in price or production reduced the R/C ratio to 4.48, whereas a 20% increase in variable cost reduced it to 4.80. Although all scenarios remain financially feasible at the aggregate level, the decline in profitability under revenue-side shocks indicates that farmers depend heavily on stable farm-gate prices and stable yields. This supports the argument that smallholder pepper farmers require better access to price information, stronger bargaining positions, and more stable marketing arrangements.

The role of market organization is particularly important for perennial crops. Research on smallholder pepper producers in Costa Rica found that contracts and market conditions influenced farmers’ investment behavior and production outcomes, especially under limited buyer competition [3]. Similarly, evidence from Sarawak and West Kalimantan shows that smallholders respond to pepper price booms and crises by adjusting labor allocation and production strategies [2]. These studies reinforce the importance of market-risk management in pepper farming.

The profitability-determinant framework suggests that farm size and farming experience improve financial performance. Larger farms may benefit from economies of scale, while experienced farmers may be better at managing seasonal operations, input timing, and market decisions. Conversely, the negative expected effect of labor-cost share suggests that cost efficiency matters as much as revenue generation. These findings are consistent with broader Indonesian evidence showing that input allocation, farmer characteristics, and production management influence crop productivity and farm success [5,6,8].

From a policy perspective, the findings suggest four priority interventions. First, extension services should focus on labor efficiency and input optimization. Second, farmer groups should be strengthened to support collective input procurement and collective marketing. Third, farmers need access to market information to reduce vulnerability to price fluctuations. Fourth, quality improvement and post-harvest handling should be improved to strengthen farm-gate prices.

This study has limitations. The manuscript was finalized from processed aggregate outputs and does not include the full raw dataset in the submitted file. Therefore, standard deviations, minimum-maximum values, break-even price, break-even production, and full regression coefficients should be inserted after re-checking the raw dataset. Nevertheless, the available processed values are internally consistent and sufficient to demonstrate aggregate feasibility, cost composition, and sensitivity trends.

Conclusion

This study confirms that smallholder pepper farming is financially feasible under observed production and market conditions. Average total revenue was IDR 292,900,000 per year, average total cost was IDR 52,280,000 per year, and average net income was IDR 240,620,000 per year. The R/C ratio of 5.62 indicates strong financial feasibility. The cost-structure analysis shows that variable costs dominate total cost, especially labor. Labor accounted for 49% of total cost, followed by pesticide cost, fertilizer cost, depreciation, and land tax. Sensitivity analysis indicates that profitability remains feasible under all simulated scenarios, but price and production declines reduce profitability more sharply than variable-cost increases. This means that revenue-side risk is the main threat to financial sustainability. The profitability framework suggests that farm size and farming experience strengthen financial performance, while a high labor-cost share reduces financial efficiency. The study recommends improving labor productivity, optimizing fertilizer and pesticide use, strengthening farmer groups, improving market-information access, and developing marketing strategies that reduce price-risk exposure [10-13].

Declarations

Funding: This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Conflict of Interest: The authors declare no conflict of interest.

Ethical Approval: The study used farm-level survey and cost-revenue data from farmer respondents. Ethical approval information and approval number should be inserted if required by the target journal.

Author Contributions: J.J. contributed to conceptualization, supervision, manuscript drafting, and final approval. R.T., A., H., M.I., A.R., A.A., S.M., and A.A.A. contributed to data organization, methodology, analysis, literature enrichment, manuscript review, and editing. All authors approved the final manuscript.

Data Availability Statement: The data supporting the findings of this study are available from the corresponding author upon reasonable request.

AI Usage Statement: Generative AI was used only to support language editing, formatting, reference organization, and manuscript preparation. The authors remain responsible for the scientific content, data accuracy, interpretation, and final manuscript.

References

- Nair, K. P. P. (2011). Agronomy and economy of black pepper and cardamom: The king and queen of spices. Elsevier.

- Wadley, R. L., Mertz, O. (2005). Pepper in a time of crisis: Smallholder buffering strategies in Sarawak, Malaysia and West Kalimantan, Indonesia. Agricultural Systems, 85(3), 289-305.

- Sáenz-Segura, F., D’Haese, M., Speelman, S. (2009). The influence of contracts on smallholder pepper (Piper nigrum L.) producers in Costa Rica under different market conditions. Fruits, 64(6), 371-382.

- Rumallang, A., Jumiati, J., Akbar, A., Nandir, N. (2019). Analisis struktur, perilaku dan kinerja pemasaran kentang di Desa Erelembang Kecamatan Tombolopao Kabupaten Gowa. Agrikultura, 30(3), 83-91.

- Maulidiyah, R., Salam, M., Jamil, M. H., Tenriawaru, A. N.,Rahmadanih, & Saadah. (2024). Examining the effects of input allocation on potato production, production efficiency, and technical inefficiency in potato farming: Evidence from the Stochastic Frontier Model in search of sustainable farming practices. Sustainable Futures, 7, 100218.

- Rumallang, A., Salam, M., Fudjaja, L., Diansari, P., Patandjengi, B., et al. (2026). Examining the effect of farm and farmers’ characteristics and input allocation on potato production. Frontiers in Sustainable Food Systems, 9, 1651329.

- Saptana, S. A. L., Perwita, A. D., Sayaka, B., Gunawan, E., Sukmaya, S., et al. (2022). Analysis of competitive and comparative advantages of potato production in Indonesia. PLOS ONE, 17(2), e0263633.

- Maulidiyah, R., Salam, M., Jamil, M. H., Tenriawaru, A. N., et al. (2025). Determinants of potato farming productivity and success: Factors and findings from the application of structural equation modeling. Heliyon, 11, e43026.

- Syarif, Y. A., Hasyim, A. I., Situmorang, S. (2019). Financial feasibility analysis of pepper farming in North Lampung Regency of Lampung Province, Indonesia. Russian Journal of Agricultural and Socio-Economic Sciences, 89(5), 189-196.

- Hobbs, J. E. (1996).Atransaction cost approach to supply chain management. Supply Chain Management: An International Journal, 1(2), 15-27.

- Key, N., Runsten, D. (1999). Contract farming, smallholders, and rural development in Latin America: The organization of agroprocessing firms and the scale of outgrower production. World Development, 27(2), 381-401.

- Sartorius, K., Kirsten, J. (2007). A framework to facilitate institutional arrangements for smallholder supply in developing countries: An agribusiness perspective. Food Policy, 32(5-6), 640-655.

- Ton, G., Desiere, S., Vellema, W., Weituschat, S., D’Haese,M. (2017). The effectiveness of contract farming for raising income of smallholder farmers in low- and middle-income countries: A systematic review. Campbell Systematic Reviews, 13(1), 1-131.