Journal of Economic Research & Reviews(JERR)

ISSN: 2771-7763 | DOI: 10.33140/JERR

Impact Factor: 1.3

Review Article - (2025) Volume 5, Issue 3

Does Debt Hamper Economic Growth? A Time Series Analysis for Tanzania (1990 – 2023)

22Senior Lecturer in Economics and Head of Department of Economics at St Augustine, University of Tanzania, Tanzania

Received Date: Aug 27, 2025 / Accepted Date: Sep 25, 2025 / Published Date: Oct 21, 2025

Copyright: ©©2025 Mariam Baus Abubakar, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Citation: Abubakar, M. B., Warioba, F. D. (2025). Does Debt Hamper Economic Growth? A Time Series Analysis for Tanzania (1990

Abstract

This study investigated relationship between debt and economic growth in Tanzania, with a specific focus on whether debt hampers the country’s long run economic growth. Using annual time series data from 1992 to 2023. Analysis employs Johansen Cointergration test and Vector Error Correction Model (VECM) to explore both short run and long run dynamics between GDP and macroeconomic variables including debt, (FDI), inflation, exchange rate and institutional quality. Empirical results reveal existence of long run equilibrium relationship among variables. Specifically, debt is found to have a statistically significant negative effect on GDP in long run, supporting debt overhang theory, which suggests that excessive debt discourages investment and impedes growth. In short run, however, effect of external debt on economic growth is statistically insignificant likely due to implementation lags and inefficiencies in public investment. Other variables such as exchange rate volatility, poor institutional quality and unproductive FDI flows also show negative long run impacts on growth, while moderate inflation appears to support growth mildly. Based on these findings, the study recommends improved debt management policies, stronger public investment efficiency and institutional reforms to ensure that borrowing contributes effectively to sustainable economic growth in Tanzania.

Keywords

Foreign Debt, VECM, GDP, FDI, Inflation & Exchange Rate

Introduction

Foreign debt has become a defining feature of modern economic development, particularly for both Less Developed Countries (LDCs), including Tanzania. Governments often resort to external borrowing to finance infrastructure, stabilize currency, manage fiscal deficits, or stimulate economic growth. While foreign debt can serve as a strategic tool for development, its long-term impact on economic growth remains a subject of intense debate in academic and policy circles. Globally, the total external debt stock reached $97 trillion in 2023, according to the International Monetary Fund, with developing countries accounting for over $11.4 trillion of this amount [1]. Many LDCs especially in Sub- Saharan Africa, South Asia, and parts of Latin America are facing unsustainable debt burdens. For example, Tanzania defaulted on its sovereign debt in 2020, while Ghana, Sri Lanka, and Ethiopia have entered debt restructuring negotiations due to unsustainable debt-to-GDP ratios exceeding 70%.

In contrast, MDCs like the United States (with a debt-to-GDP ra¬tio exceeding 120%) and Japan (over 260%) continue to borrow extensively, often at low interest rates, without triggering simi¬lar crises raising questions about debt sustainability, institutional strength, and policy effectiveness across different income groups. Over the past three decades, Tanzania has increasingly relied on external debt to finance its development agenda including infra-structure, education and health. While debt can play a vital role in bridging the resource gap in developing economies, its accu-mulation beyond sustained levels raises serious concerns about its impact on long term economic growth. Despite periodic debt relief initiatives such as High Indebted Poor Countries (HIPC) Initia¬tives and Multilateral Debt Relief Initiative (MDRI), Tanzania’s external debt stock has been rising steadily in recent years. For’ example, from 2022 to 2023 the country’s debt rose from 40.485% to 44.611% respectively (World Bank 2024). This trend raises questions about whether external borrowing is being effectively utilized to generate economic growth or whether it is creating a debt overhang that discourages investment, distorts fiscal policy and undermines macroeconomic stability.

Moreover, existing empirical studies on the debt growth nexus in Tanzania such as Rut Sitara (2002) & Said et al (2010) have yielded mixed and inconclusive results with limited attention to the dynamic effects of debt in both the short and long run. This gap creates a need for updated, country specific research using robust econometric methods to assess whether external debt truly sup-port or hinders Tanzania’s economic growth. This study therefore, seeks to fill this gap by examining the short run and long run effects of external debt on economic growth in Tanzania, using time series data and the Vector Error Correction Model (VECM). The findings also provide evidence on how inflation, exchange rate, FDI, and institutional quality influences on economic growth. Public debt is a central concern for many developing economies, including Tan¬zania. While debt can finance productive investment, excessive debt levels may constrain economic growth through high interest payments and reduced fiscal space. This study seeks to answer a critical question: Does public debt hamper economic growth in Tanzania? The paper uses time series data and econometric meth¬ods to empirically test the relationship between debt accumulation and economic performance.

Literature Review

Theoretical Literature Review

There were numerous theoretical arguments on public debt, including debt overhang, crowding- out, and flexible accelerator theories. A debt overhang is one in which a country is unable to take on additional debt to fund future projects due to a large amount of debt. By creating a debt overhang, current public investment is dissuaded, since all earnings from new projects will go to existing debt holders, leaving the entity with very limited resources for it to recover from. propose that the debt overhang theory argues public debts are negatively correlated with economic growth in the long run [2].

The fear of high future taxes and/or debt crises reduces the incentive for private investment [3]. This implies that increased public debt negatively impacts economic growth through a decrease in investment. Furthermore, the crowding out theory holds that debt could be so burdensome that government revenue may not be sufficient to provide public services that stimulate private investment and boost private sector engagement. argue that public debt is sub- ject to crowding-out effects, especially when government securities are substituted for capital stock in portfolios containing public assets [4]. According to the traditional Keynesian IS-LM model, an increase in government expenditures would lead to an increase in public debt that would have an expansionary effect on the economy because of an increase in income and transaction demand.

In this study we used Debt overhang theory developed, they argue that when a country’s debt is very large the expected future debt repayment discourages both public and private investment [5]. Investors anticipate that much of the return from new investment will be used to repay existing debt and therefore they hold back negatively impact the economic growth. In LDCs there is a problem of debt overhang because of limited revenue base, low savings and dependence on aids and commodity export and they are more exposed to external shocks which amplify the debt growth trade off. Supporting theories of debt overhang are Solow growth Model (1956) which explains debt affects capital accumulation hence steady state growth, Endogenous growth theory by Romer which explains public debt may reduce long run growth if it crowds out productivity enhancing spending like infrastructure and education.

Empirical Literature Review

Examined the impact of fiscal policy variables on private investment in Nigeria with the ARDL technique panning the period 1980-2017 and found that public external debt had a deleterious effect on private investment both in the long and short run [6]. examined the Dynamic Impact of Public External Debt on Capital Formation in Sub-Saharan Africa from 2000 to 2008 using the PMG estimation approach and found that increasing external debt stock and interest payment on it only have a marginal impact on capital formation in the short run but a more serious negative effect in the long run [2]. Examined the role external debt and foreign direct investment played in influencing financial development in Africa from 2002 to 2015 with dynamic panel and GMM estimation technique and found that external debt and foreign direct investment have a significant positive relationship with financial development in African economies [7].

Examined the impact of public debt on investment: Evidence from Nigeria both in the short-run and the long-run using the ARDL framework over the period, 1981-2016, and found that domestic debt improves or crowds in both private and public investments, and external debt crowds-in private investment both in the short-run and the long-run. Moreover, the impact of external debts on all forms of investment in Nigeria is greater than domestic debts [8]. Assesses the impact of debt overhang and crowding out effect’s hypotheses on investment in Nigeria from 1981 to 2018 [9]. With the Vector Error Correction Model, the study found that Debt- Export Ratio confirms its expansionary effect on investment. Examine the long run relationship and interconnections between public debt and domestic investment in 13 West African countries from 1986 to 2018 with Panel Dynamic Least Squares (DOLS) and Panel Fully Modified Least Squares (FMOLS), and found debts (% of GDP) have an insignificant effect on investment in the long run [10].

Investigated the impact of the components of public debts on the various forms of investment in Nigeria with the ARDL framework over the period, 1981-2016, and found that domestic debt crowds in both private and public investment, and also that external debt crowds-in private investment both in the short-run and the long-run; crowds-out public investment [8]. However, the impact of external debts on all forms of investment in Nigeria is greater than domestic debts. Considered the consequences of external loans on capital investment in Nigeria from 1996 to 2018 with the ordinary least squares multiple regression method and found that external debt has a significant negative impact on capital investment while debt servicing cost has a strong and significant positive effect on capital investment [11]. Exploited a panel dataset for 26 EU countries, between 1995 and 2015, to examine the extent to which increased levels of public debt have led to reduced public investment, based on the ‘debt overhang’ hypothesis [12].

The study found evidence that:

(i) The results are mainly driven by high-debt countries

(ii) The negative impact of debt on investment is slightly smaller in the Eurozone than in the entire EU

(iii) Both the stock and flow of public debt play a role in reducing public investment with the impact of the later that is found to be more profound. Explored the effect of public debt on private investment in Tanzania from 1970 to 2016 with the ARDL technique and found that the combined effect of domestic and external debt on private investment is statistically significant both in the long run and short run [13]. Investigated the effects of fiscal policy on private investment and economic growth in Kenya from 1973 to 2009 with a two-stage instrumental variable estimation method and found that fiscal policy impacts on investment and investment play a major role in the determination of economic growth in Kenya [14]. Motivated by the modified version of the Flexible Accelerator Model of investment behavior. Empirically investigated the determinants of Private Investment in Ethiopia with a multivariate single equation ECM estimation method for data from 1950 to 2003 in two sub-periods [15]. The study found private investment in Ethiopia is influenced positively by the domestic market, return to capital, trade openness and liberalization measures, infrastructural facilities and FDI; but, negatively by government activities, macroeconomic uncertainty and political instability.

Research Gap

From the array of empirical works, it can be observed that there exists a methodological gap for this study in an attempt to bring a new literature on How Foreign debt impact Economic growth in Tanzania. The study fills the gaps in the literature by investigating how external debts affects economic growth in a long run and short run as well as the interaction between economic growth, inflation, exchange rate, Institutional quality and Foreign Direct Investment using VECM Model. Basing on the number of observations which is 33 years (1990 to 2023) in Tanzania is a gap among many literatures. Lastly the gap is seen in showing the pattern of debt accumulation in Tanzania and describing the characteristics of such pattern.

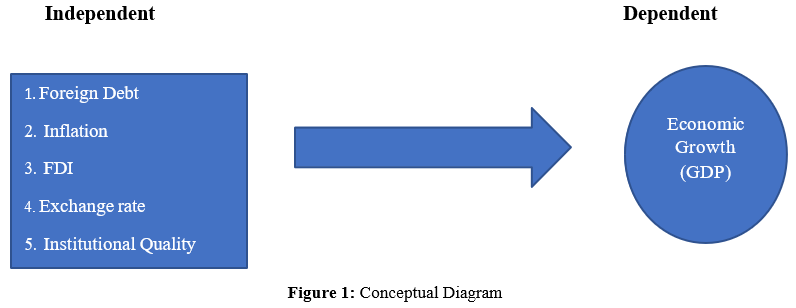

Conceptual Relationship

Economic Growth = f (Foreign Debt, Inflation, FDI, Exchange Rate, Institutional Quality) The conceptual framework assumes that economic growth in Tanzania is influenced by the level of foreign debt, the inflation rate, capital inflows such as FDI, exchange rate fluctuations, and the strength of institutional quality. A negative relationship is hypothesized between debt and growth, while FDI and strong institutions are expected to promote growth.

Methodology

Research Design and Sources of Data

This study adopted a quantitative research design, combining both descriptive and time series data econometric analysis to examine the how does foreign debt hamper economic growth in Tanzania over a 30-year period (1990 – 2023). Secondary Sources such as World Bank World Development Indicators (WDI), International Monetary Fund (IMF) and policy reports are used. The dependent variable used is GDP measured as annual growth in %, independent variables are foreign debt measured as external debt stocks percentage in GNI, Foreign Direct Investment measured as net inflows percent of GDP, inflation measured as Consumer prices. Exchange rate measured real effective exchange rate and Institutional quality measured as government effectiveness were used in the study.

Model Specification

Recommended Econometric Model is VECM Model (Vector Error Correction Model), this is because all variable was non-stationary at different lags and became stationary at first differencing. The variables were cointegrated after using Johansen test for cointegration and thus work best for vector error correction model since time series data have a tendency of influencing each other at short run and long run. VECM Model is suitable for small sample sizes (like 1990–2023 = 34 years). VECM estimates both short-run and long-run relationships, it also accounts for the dynamic nature of economic relationships and speed for adjustment. Stationarity Check using Use ADF (Augmented Dickey-Fuller) was applied, Johansen test for Cointegration to check for long-run relationship among the variables was used.

The General VECM Model is

GDP = α+β1DEBT+β2FDI+β3INF+β4EXR+β5IQ + εt

Let:

• GDP = Real Gross Domestic Product

• DEBT= External Debt

• FDI= Foreign Direct Investment

• INF= Inflation Rate

• EXR= Exchange Rate

• IQ = Institutional Quality

• Et = Error term

• α ,β= Coefficients

Results and Discussion

Unit Root Test Results for all Variables

|

Variable |

Test Statistics |

1% Critical Value |

5% Critical Value |

10% Critical Value |

P- value Z(t)= |

|

GDP |

-1.830 |

-4.380 |

-3.600 |

-3.240 |

0.6900 |

|

External debt |

-1.292 |

-4.380 |

-3.600 |

3.240 |

0.8898 |

|

FDI |

-0.279 |

-4.380 |

-3.600 |

3.240 |

0.9962 |

|

Inflation |

-0.256 |

-4.380 |

-3.600 |

3.240 |

0.1828 |

|

Exchange rate |

-0.233 |

-4.380 |

-3.600 |

3.240 |

0.9909 |

|

Institutional Quality |

-1.809 |

-4.380 |

-3.600 |

3.240 |

0.7002 |

Table1: Unit Root Test from lag0 to 10 for all Variables

Augmented Dickey Fuller Test was used to test for stationarity. From lag 0 to Lag 10 among all variables include GDP, External debt, FDI, Inflation, Exchange rate and Institution Quality failed to reject null hypothesis stating that it is non-stationary or there is unit root problem because the values of t statistics are less than the critical values at 1%, 5% and 10% and the value of P value is greater than 0.05 as illustrated in the table above.

|

Variable |

Test Statistics |

1% Critical Value |

5% Critical Value |

10% Critical Value |

P-value= Z(t) |

|

D2. GDP |

-7.534 |

-4.316 |

-3.572 |

-3.223 |

0.0000 |

|

D2. External Debt |

-4.241 |

-4.316 |

-3.572 |

-3.223 |

0.0039 |

|

D2. FDI |

-9.452 |

-4.316 |

-3.572 |

-3.223 |

0.0000 |

|

D2. Inflation |

-5.104 |

-4.316 |

-3.572 |

-3.223 |

0.0001 |

|

D2. Exchange rate |

-4.196 |

-4.316 |

-3.572 |

-3.223 |

0.0045 |

|

D2. Institutional Quality |

-5.111 |

-4.316 |

-3.572 |

-3.223 |

0.0001 |

Table 2: First Order of Difference Unit Root test results for all Variables

All variables where then difference at order of integration one so that to solve the problem of unit root, then all variables became stationary at first difference and hence reject the null hypothesis which states the variable is non-stationary. The test statistics is greater than critical values at 1% for variables GDP, FDI, Inflation and Institutional quality while External debt and Exchange rate t statistics was greater than critical value at 5%. Furthermore, all variables were significant since the p value after first difference was less than 0.05 as indicated in the table 2 above.

Cointegration

To understand long run relationships between two or more non-stationary variables we perform Cointegration test using Johansen Test for Cointegration. Standard regression on non-stationary series may give spurious results, cointegration allows us to find meaningful long-term relationships among the variables.

|

Vecrank GDP External Debt FDI Inflation EXR IQE Johansen tests for Cointegration |

|||||

|

Trend: Constant Number of OBS: 32

Sample: 1992-2023 Lags: 2 |

|||||

|

Maximum Rank |

Parms |

LL |

Eigenvalue |

Trace Statistic |

5% Critical Value |

|

0 |

42 |

-410.50166 |

- |

109.1801 |

94.15 |

|

1 |

53 |

-393.3633 |

0.65738 |

74.9034 |

68.52 |

|

2 |

62 |

-378.34258 |

0.65738 |

74.9034 |

68.52 |

|

3 |

69 |

-365.67602 |

0.54691 |

19.5289 |

29.68 |

|

4 |

74 |

-360.90141 |

0.25800 |

9.9796 |

15.41 |

|

5 |

77 |

-356.90557 |

0.22100 |

1.9880 |

3.76 |

|

6 |

78 |

-355.91159 |

0.06023 |

- |

- |

Table 3: Cointegration Results

Test statistics is greater than the critical we reject null hypothesis which states no cointegration. The maximum rank indicates the number of cointegrating relationship, according to the results of table number 3 above there are 2 cointegrating equations among the variables.

Vector Error Correction Model

There are 3 (three) Cointegrating vector exist since trace statistics is greater than critical value at first time at maximum rank 3, where by 19.5289 < 29.68 as indicated in table number 3 above. Table number 4 below indicates the long run equilibrium relationship among the variables.

|

Cointegrating Equations |

||||||

|

Equation |

Parms |

Chi2 |

P>chi2 |

|||

|

Cel |

5 |

52.12199 |

0.0000 |

|||

|

Identification: Beta is Exactly Identified Johansen Normalization Restriction Imposed |

||||||

|

Beta |

Coef |

Std. Err |

Z |

P>|z| |

[95% Conf. Interval] |

|

|

Cel GDP |

1 |

. |

. |

. |

. |

|

|

External Debt |

-.7491565 |

.1393665 |

-5.33 |

0.000 |

-1.01631 |

-.4700031 |

|

FDI |

-9.959513 |

1.482789 |

-6.72 |

0.000 |

-12.86571 |

-7.053311 |

|

Inflation |

-.4801144 |

1.482783 |

-2.05 |

0.041 |

-.940006 |

-.0202227 |

|

EXR |

-.0221543 |

.0040887 |

-5.42 |

0.000 |

-.0301679 |

-.0141406 |

|

IQE |

-65.3201 |

17.122449 |

-3.81 |

0.000 |

-98.87956 |

-31.76063 |

|

Cons |

25.62683 |

. |

. |

. |

. |

. |

Table 4: Cointegration Equation of Long Run Relationship

GDP 1(normalized) is the dependent variable, external debt (-0.7431565) at 0.000 significant negative long run effect on GDP. FDI (-9.959513) at 0.000 significant negative long run effect on GDP. Inflation (-0.4801144) at 0.041 significant negative long run effect on GDP. Exchange rate (-0.221543) at 0.000 significant negative long run effect on GDP. Institutional quality (-65.3201) at 0.000 significant negative long run effect on GDP. Constant (25.62683) at 0.000 significant intercept of the long run equation. The estimated long run equilibrium relationship is

GDPt = 0.743. External Debtt + 9.959. FDIt + 0.48. Inflationt + 0.221 EXRt + 65.3201. IQEt – 25.63.

But since GDP is Normalized to 1, the Equation Really Means GDPt - 0.743. External Debtt - 9.959. FDIt - 0.48. Inflationt - 0.221 EXRt - 65.3201. IQE = Constant.

The Economic Interpretation of the above model is as follows; External Debt (-0.743): A 1-unit increase in external debt is associated with long run decrease in GDP by 0.743 units or 74.3%. Surprisingly FDI (-9.959) also shows a negative long run effect on GDP, this might suggest FDI is not well directed or is extractive in nature. Inflation (- 0.48) is associated with a negative long run effect on GDP perhaps it is a cost push inflation. Exchange rate (-0.221) indicates a higher exchange rate like depreciation affects negatively the GDP in the long run. Institutional Quality (- 65.321) indicates poor institutional quality reduces GDP and this is very consistent with Institutional theory. All the variables are statistically significant at 5% level where the p- value < 0.05 indicating that the cointegration relationship is strong and reliable.

Short Run Dynamic and Speed of Adjustment

Short Run Dynamic and Speed of Adjustment for GDP Equation

The Error Correction term Ce1 L1 variable with coefficient (-0.0957) is significant at 0.021. The coefficient represents the speed of adjustment of GDP to restore long run equilibrium after a shock. The coefficient confirms that if GDP deviates from its long run path it corrects about 9.6% of the disequilibrium in the next period. This is a moderate adjustment speed suggesting it takes several periods to return to equilibrium. In the short run dynamics, it shows how the first changes variables affect a certain variable in a short run, the results show that the past GDP changes reduces current growth by -0.4207. External debt, FDI, Inflation, Exchange rate and Institutional Quality has no effect to GDP in the short run

Short Run Dynamic and Speed of Adjustment for External Debt Equation

There is positive and insignificant error correction term meaning that external debt does not adjust back to the long run equilibrium in the short run. Since it is not significant (P value = 0.165>0.05) shocks to the long run relationship do not significantly affect external debt in the short run. LD GDP (-1.1846) is negative but not significant. LD External debt (0.4975) is positive and significant meaning that past changes in debt increases current debt. FDI, Inflation, Exchange rate and Institutional Quality are not significant meaning that they do not affect external debt in the short run.

Short Run Dynamic and Speed of Adjustment for FDI Equation

The error correction term for FDI is positive (0.0679) suggesting that FDI may not correct deviations from long run equilibrium, with p value 0.061 just above 5% significance so it indicates weak short run adjustment of FDI. Furthermore, none of the variables including GDP, External debt, inflation, exchange rate and Institutional quality have significant short run effect on FDI.

Short Run Dynamics and Speed of Adjustment for Inflation

The Coefficient (-0.2287) implies that approximately 22.87% of the disequilibrium is corrected each period and is significant at 5% level since the p value is 0.045. So, inflation will return to equilibrium over time about 4 to 5 periods to close the gap fully. Coefficient (-0.9550467) significant at level 5% indicates a short run increase in GDP leads to a reduction in inflation. External debt has coefficient (0.1649314) at p value= 0.075 which is marginally significant indicating there is a slightly positive impact on inflation in the short run. Institutional Quality with coefficient (21.04932) is significant at 5% level since the p value = 0.036 suggesting that Institutional quality has a positive impact on inflation in the short run. FDI, Exchange rate and are positive but not significant indicating they have no any short run impact on inflation.

Short Run Dynamics and Speed of Adjustment for Exchange Rate

There is no strong evidence of short run exchange rate adjustment towards the long run path in the model of exchange rate since the p value at ce1 = 0.368 which means exchange rate does not respond significantly to deviations from the long run equilibrium. None of the variables are statistically significant since all p-values > 0.05. GDP, FDI, Inflation, Exchange rate (its own lag) and Institutional quality show no significant short run impact on exchange rate.

Short Run Dynamics and Speed of Adjustment for Institutional Quality

There is no evidence that institutional quality adjusts back to long run equilibrium in the short run. The system does not correct disequilibrium suggesting that institutional quality is not dynamic responsive to shocks in the short term because its p value at ce1 is = 0.760. Furthermore, none of the lagged independent variables have a significant short run effect on Institutional Quality since all the p value > 0.05.

Discussion of the Findings

Trend of Tanzania Debt Accumulation

Figure 2: Debt Accumulation in Tanzania from 1990 T0 2023

In Early 1990s to 1995 there was high and volatile debt levels starting around 100% or more with noticeable fluctuations, this period reflects Tanzania’s post structural adjustment era which was characterized by high levels of external debt and limited fiscal capacity. There was a sharp decline in debt accumulation from 1995 to 2000 attributing to debt relief programs such as heavily indebted poor countries (HIPC) initiative, structural reforms in public finance and improved fiscal discipline. In the early 2000s debt reached at its lowest point coincides with Multilateral debt relief initiative (MDRI) and stronger donor partnership. Tanzania also received significant debt cancelation especially from multilateral lenders like IMF and World Bank at this era.

In 2007 to 2015 debt levels remained relatively low and stable during this period, the government managed to balance develop-ment financing with debt sustainability [16]. In 2016 to 2023 a gradual rise in debt accumulation begins which reflects increased government borrowing to fund infrastructure megaprojects exam¬ple SGR railway, Stiegler’s Gorge dam and growing social and eco¬nomic investment needs. Although the rise in this phase appears to be modest but the upward trend suggests growing fiscal pressures.

Does Foreign Debt Hamper Economic Growth?

Results show there is a significant negative long run effect of external debt on GDP and a non-significant short run effect of external debt on GDP supporting the idea that debt only becomes a burden over time through reduced investment and fiscal pressure. The long run negative effect proves the debt overhang theory suggested by Krugman in 1989 true, that when a country accumulates excessive external debt, the expected future tax burden rises and this discourages private investment as investors fear future earnings will be taxed to repay the debt and as a result economic growth slows down. In Tanzania high debt service obligations can crowd out public investment in sectors like infrastructure, education and health. Furthermore, the significant long run effect of external debt on GDP proves the crowding out effect theory since high debt may require increased interest payments which lead to reduced government spending on productive activities and negatively affect GDP in the long run. If debt is used for non-productive or corruption prone projects, it adds to the burden without stimulating growth.

Short run neutral effect can be proved in Keynesian Stimulus Effect which states in the short run, borrowing may be used to stimulate demand example financing recurrent expenditures or subsidies. However, the macroeconomic impact of such spending may be limited unless directed toward productive investment. Development projects financed by debt like roads, power plants take years to complete, thus their positive or negative effects are not immediately visible in short run GDP dynamics. Studies like Rutasitara (2002) and Said et al (2010) found that high external debt burdens reduced economic growth in Tanzania especially during the 1990s despite debt relief under HIPC and MDRI. Pattillo et al (2002) found that external debt above 35 to 40% of GDP has a negative effect on growth in low income countries, confirmed similar effects in sub Saharan Africa [3]. Generally negative long run effect of external debt on GDP in Tanzania aligns with debt overhang and crowding out theories and the short run neutrality arises because debt financed investments take time to affect the economy and of¬ten face absorption and execution constraints.

What is the Influence of Inflation, Exchange Rate, FDI, and Institutional Quality on Economic Growth?

Results shows that a positive long run coefficient of inflation on GDP suggesting that moderate inflation may be growth friendly in Tanzania possibly due to demand side effects or pride flexibility. Found that moderate inflation in Tanzania may support growth but excessive inflation usually above 10% harms it [17]. VECM results showed a significant negative long run effect of exchange rate on GDP implying that exchange rate depreciation increases cost of imported capital goods and thus undermine growth. found that exchange rate volatility in Tanzania harms investment and growth especially when driven by external shocks [18]. In addition, VECM results shows a significant negative long run impact of FDI on GDP which may reflect FDI flowing into nonproductive or enclave sectors, it also indicates profit repatriation exceeding local benefits and weak backward linkages with the local economy. World bank (2020) noted that FDI in Tanzania is concentrated in mining and extractives with limited job creation. Lastly, Institutional quality had a significant negative long run effect on GDP likely due to government weakness, ineffective regulatory and legal systems and public sector inefficiency. Afrobarameter and Transparency international have documented persistent governance and corruption challenges in Tanzania. Found that weak institutions in East Africa including Tanzania limit the effectiveness of public investment and macroeconomic reforms [19].

Conclusion and Recommendations

This study set out to examine the impact of external debt on economic growth in Tanzania using time series and employing the Johansen Cointegration test and Vector Error Correction Model (VECM). The findings provide both theoretical and empirical confirmation that external debt has a significant negative effect on GDP in long run while its short run impact is statistically insignificant. The long run negative relationship supports the Debt Overhang Theory which states that large external debt burdens create uncertainty and discourage private investment due to the anticipation of future tax increase and fiscal tightening. Additionally, high debt service obligations crowds out public investment in productive sectors like infrastructure, health and education. The short run analysis reveals that external debt does not immediately influence economic growth possibly due to time lags in the implantation and returns of debt financed projects. Moreover, the study found that other macroeconomic variables such as exchange rate, FDI inflows, institutional quality and Inflation also plays a significant role in determining long term economic growth, though many showed no immediate short run effect on economic growth [20,21].

Policy Recommendation for Tanzania

1. 1.Improved External Debt Management: Tanzania should strengthen its debt management framework by ensuring that new borrowing is aligned with productive investment and economic priorities. The country should also adopt debt sustainability thresholds avoiding excessive borrowing especially for recurrent expenditure.

2. Enhance Public Investment Efficiency: Tanzania should ensure external borrowing is allocated to high return development projects such as infrastructure, manufacturing and export-oriented sectors. There should also be introduction to transparent projects selection criteria and regular cost benefit analysis.

3. Strengthen Institutional Quality: The country should improve its governance, public sector accountability and anti-corruption measures to ensure debt is used effectively. There should be strengthening of legal and regulatory frameworks to foster a conducive environment for private sector growth.

4. The Bank of Tanzania should Ensure Exchange rate stability by implementing macroeconomic policies that reduce exchange rate volatility which undermines investor confidence and raises debt service cost especially in foreign currency.

5. The Ministry of Industry, trade and Investment should maximize FDI benefits by creating policies that link FDI inflows with local content requirements, technology transfer and employment generation. The ministry responsible should also encourage FDI into value adding sectors beyond mining and raw materials.

6. The country should maintain low and stable inflation example 5 to 7% since a moderate inflation can support growth, however excessive inflation should be curbed through coordinated fiscal and monetary policies.

7. Last but not the list the country should boost domestic resources mobilization by improving tax collection, reduced tax evasion and broadening the tax base to reduce reliance on external borrowing and encourage domestic borrowing. To sustain long term growth, Tanzania must adopt a balanced strategy that ensures external debt is a tool for development, not a burden. Without sound fiscal discipline, strong institutions and targeted investments, debt accumulation will continue to constrain the country’s growth potential.

Funding

This research received no external funding.

References

- International Monetary Fund (2023), International Debt report, IMF, USA.

- Kocha, C. N., Iwedi, M., & Sarakiri, J. (2021). The dynamic impact of public external debt on capital formation in Sub-Saharan Africa: The Pooled Mean Group Approach. Journal of Contemporary Research in Business, Economics and Finance, 3(4), 144-157.

- Chowdhury, A. (2001). External debt and growth in developing countries: a sensitivity and causal analysis. WIDER-Discussion Papers.

- De Leeuw, F., & Holloway, T. M. (1983). Cyclical adjustment of the federal budget and federal debt. Survey of Current Business, 63(12), 25-40.

- Abdulkarim, Y., & Saidatulakmal, M. (2021). The impact of fiscal policy variables on private investment in Nigeria. African Finance Journal, 23(1), 41-55.

- Agyapong, D., & Bedjabeng, K. A. (2020). External debt stock, foreign direct investment and financial development: Evidence from African economies. Journal of Asian Business and Economic Studies, 27(1), 81-98.

- Ogunjimi, J. (2019). The impact of public debt on investment: Evidence from Nigeria. DBN Journal of Economics & Sustainable Growth.

- Ebhotemhen, W. (2020). The effects of external debt and other selected macroeconomic variables on investment in Nigeria. Journal of Economics and Allied Research, 5(1), 91-105.

- Fagbemi, F., & Adeosun, O. A. (2021). Public debt-investment nexus: the significance of investment-generation policy in West Africa. Journal of Economic and Administrative Sciences, 37(4), 438-455.

- Omodero, C. O. (2019). External debt financing and public capital investment in Nigeria: A critical evaluation. Economics and Business, 33, 111-126.

- Picarelli, M. O., Vanlaer, W., & Marneffe, W. (2019). Does public debt produce a crowding out effect for public investment in the EU?.

- Mabula, S., & Mutasa, F. (2019). The effect of public debt on private investment in Tanzania. African Journal of Economic Review, 7(1), 109-135.

- Isaac, M. K., & Samwel, K. C. (2012). Effects of fiscal policy on private investment and economic growth in Kenya. Journal of Economics and Sustainable Development, 3(7), 8-16.

- Sisay, A. M. (2010). Determinants of private investment in Ethiopia: A time series study. Ethiopian Journal of Economics, 19(1), 75-124.

- International Monetary Fund (2013), Staff report, IMF, USA.

- Ndanshau, M. O. (2010). Money and other determinants of inflation: the case of Tanzania. Indian journal of economics and business, 9(3), 503-545.

- Adam, C. S., & Bevan, D. L. (2006). Aid and the supply side: Public investment, export performance, and Dutch disease in low-income countries. The World Bank Economic Review, 20(2), 261-290.

- Ndulu, B. J., O'Connell, S. A., Bates, R. H., Collier, P., & Soludo, C. C. (2008). The political economy of economic growth in Africa, 1960-2000. Cambridge University Press,.

- Krugman, P. (1988). Financing vs. forgiving a debt overhang. Journal of development Economics, 29(3), 253-268.

- Sachs, J. (1989). The debt overhang of developing countries. In Debt, Stabilization and Development: Essays in Memory of Carlos DíazAlejandro, Oxford: Basil Blackwell, 80–102.

- Kasidi, F., & Said, A. M. (2013). Impact of external debt on economic growth: A case study of Tanzania. Advances in Management and Applied economics, 3(4), 59.